Cuts aren‘t bullish

S&P 500 reversed, but the upswing teemed with non-confirmations and oddities, the common denominator being strong market pressure on Powell to give up further tightening and actually cut rates soon, perhaps strengthened by the Yellen behind closed doors banking meeting, which didn‘t bring about any deposits game changer. The reality of almost $400bn fresh liquidity thrown at the issues over the last two weeks, remains.

Deposits are still leaving smaller banks for bigger banks and money market funds – the KRE and XLF charts reflect the stress. This is a time of great uncertainty – financials can either stabilize through all the Fed actions and foreign swap lines (the same goes for Russell 2000), or decline considerably more. Either way, the dust hasn‘t settled yet.

The consumer continues burning through excess savings, the savings rate is at historically low levels, credit card usage is up, and bank lending standards are tightening. Mortgages, car loans, credit card balances… meanwhile LEIs continue declining, and it‘s also exactly one year since the Fed started the steep rate raising cycle, meaning that the real economy still has to feel most of the rate hikes already in (steepest rate raising cycle since mid 1990s, by the way).

Yet thanks to the banking troubles ushered in through the risk-free rate of return changes, markets have decided that it‘s time for Powell to officially pivot. Yes, they were thrown off whack by the 25bp hike, and chose to disregard the promise to hike once again (the bets on May being the pause month are 80%), and keep them restrictive. Likewise, it didn‘t listen to the remark that any tightening done through the lending standards of commercial banks, is actually equivalent to a hike.

The market is looking forward for a pivot soon, without appreciating what such a pivot actually means (as in heralds)– a recognition of troubles ahead. And these would arrive either through more banking news, through job market weakness, or through earnings disappointments. The Q1 earnings estimates would have to be yet downgraded I‘m afraid, and the same goes for Q2 as a minimum.

Stocks don‘t get that yet, and are focusing on easing already in Jun, without asking whether we have signs of proper market bottom such as rising LEIs, accomodative Fed and loose commercial banking standards. None of these apply.

That‘s why for all the Friday move higher, I continue being medium-term bearish as there isn‘t a rush out of dollars, precious metals rising on more than fits banking jitters, services inflation and nominal wage growth still hot (factors making the Fed restrictive), and market breadth limping along.

Keep enjoying the lively Twitter feed via keeping my tab open at all times – on top of getting the key daily analytics right into your mailbox. Combine with Telegram that never misses sending you notification whenever I tweet anything substantial, but the analyses (whether short or long format, depending on market action) over email are the bedrock.

So, make sure you‘re signed up for the free newsletter and that you have my Twitter profile open in a separate tab with notifications on so as to benefit from extra intraday calls.

Let‘s move right into the charts

S&P 500 and Nasdaq outlook

Instead of keeping price action below 3,945 - 3,958 „point of control“ zone, overcoming 4,015 on a closing basis again looms (bullish very short-term). Tech, semis and communications continue acting strong, but unless financials, value and Russell 2000 turn, this respite is only temporary even if it breaks 4,045, and even if it goes for 4,115. The internals are quite weak and VIX appears jsut resting.

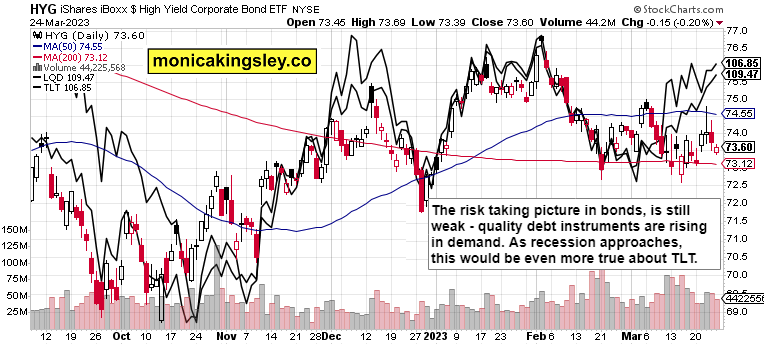

Credit markets

Bonds are still highly selective of risk. The fundamentals continue favoring LQD, TLT and TLH as opposed to HYG, JNK and the like – this isn‘t a hallmark of broad risk-on rally in stocks. Expect also the 10-y yield to continue retreating.

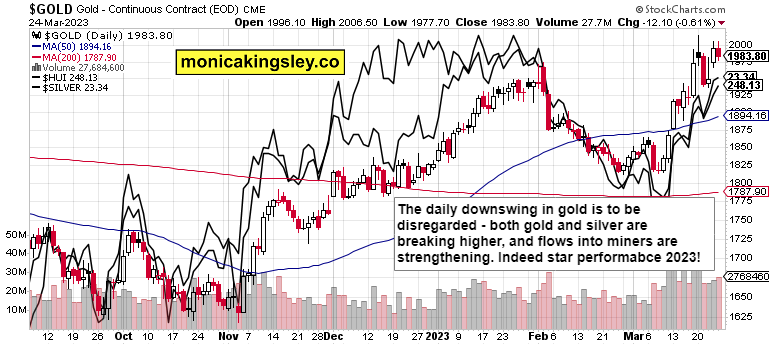

Gold, Silver and Miners

Precious metals are the stars – banking question marks, bets on Fed easing, stubborn inflation, nominal wage growth – all of these point to increasing appeal of gold and silver down the road (no matter any temporary hits).

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.