CPI–NFP double punch poised to set Q4 market tone

Key takeaways

-

CPI & NFP Take the Spotlight – US inflation (Wed) and the delayed jobs report (Fri) will recalibrate Fed expectations and drive USD direction.

-

Trade Tariffs in Play – Trump’s softer tone with China lifted sentiment, but headlines could swiftly reverse market mood.

-

Policy Guidance – A dense line-up of Fed speakers, including Chair Powell, will clarify the easing path amid strong growth and mixed labor signals.

-

Eurozone CPI as a Catalyst – Friday’s print will test the ECB’s dovish bias, with clear implications for EUR.

-

Commodities Diverge – Gold remains supported by lower real yields; oil faces pressure from supply dynamics despite geopolitical noise.

Market overview

Global markets enter the new week navigating a rare mix of inflation uncertainty, delayed labor data, shifting tariff rhetoric, and AI-driven equity momentum. US indices remain at record highs, underpinned by resilient growth and strong technology investment. Yet the temporary data blackout caused by the US government shutdown has clouded the Fed’s visibility, giving extra weight to this week’s CPI and NFP releases.

September’s CPI (Wednesday) and the rescheduled NFP (Friday) are set to be decisive for rate expectations heading into year-end. A softer inflation print combined with weak job creation would bolster expectations for further easing in October and December, weakening the dollar and supporting risk assets. Conversely, upside surprises could re-anchor the market toward a slower or shallower easing path, lifting yields and firming USD.

Trade policy adds another variable. Trump’s recent willingness to negotiate with China has supported risk sentiment, but the history of on-off tariff rhetoric suggests headline volatility is never far away. A stable tone favors cyclical FX and equities, while renewed escalation would likely trigger USD strength and weigh on commodities.

In Europe, Friday’s Eurozone CPI release will be a key test of the ECB’s dovish tilt. A downside surprise would reinforce expectations of prolonged accommodation and weigh on EUR/USD. UK monthly GDP (Thursday) will provide a snapshot of domestic resilience but will likely be overshadowed by USD moves and global sentiment.

Key macro themes

1. CPI → Rates → USD & Risk Assets

-

Baseline: Core CPI at 0.3% m/m would keep the disinflation path intact, supporting expectations for a 25 bp Fed cut before year-end. This would typically pressure the USD, support gold, and underpin equities via lower real yields.

-

Hot CPI (≥0.4% m/m): Reprices the easing path, pushes Treasury yields higher, strengthens the dollar, and could trigger an equity pullback.

-

Cool CPI (≤0.2% m/m): Reinforces the easing narrative, softens the USD, steepens bull flattening in Treasuries, and boosts EM and high-beta FX.

2. Delayed NFP → Labor Narrative Reset

The September jobs report carries outsized significance after weeks of patchy labor data.

-

Sub-trend jobs (50–100k) with 0.3% wages: Confirms cooling demand, softens USD, supports gold and Nasdaq.

-

Upside surprise (>150k or hotter wages): Challenges the easing narrative, lifts front-end yields, supports USD, and weighs on equities.

3. Tariffs & Sentiment

Markets have rebounded on Trump’s softer tone, reducing tail risks. However, volatility remains headline-driven.

-

Cooperative tone: Supports EUR, GBP, NZD and cyclical equities.

-

Renewed escalation: Favors USD/JPY and typically pressures commodities and EM FX.

Asset class implications

-

Equities: Momentum is intact, but CPI and NFP are credible catalysts for a volatility spike. Dips may be bought if CPI cools; hot data could trigger a tactical pullback.

-

USD: Direction will be determined by CPI first, NFP second. A 0.3% CPI plus soft NFP combination leans mildly bearish for the greenback.

-

EUR/GBP: Vulnerable to USD moves and domestic data—Eurozone CPI downside caps EUR; UK GDP offers short-term GBP impulses.

-

Gold: Bullish trend remains; lower real yields and any USD softness support further upside.

-

Oil: Pressured by OPEC+ supply expectations and US inventories. Macro risk-off on hot data could weigh further, while tariff détente offers only fleeting support.

Technical outlook

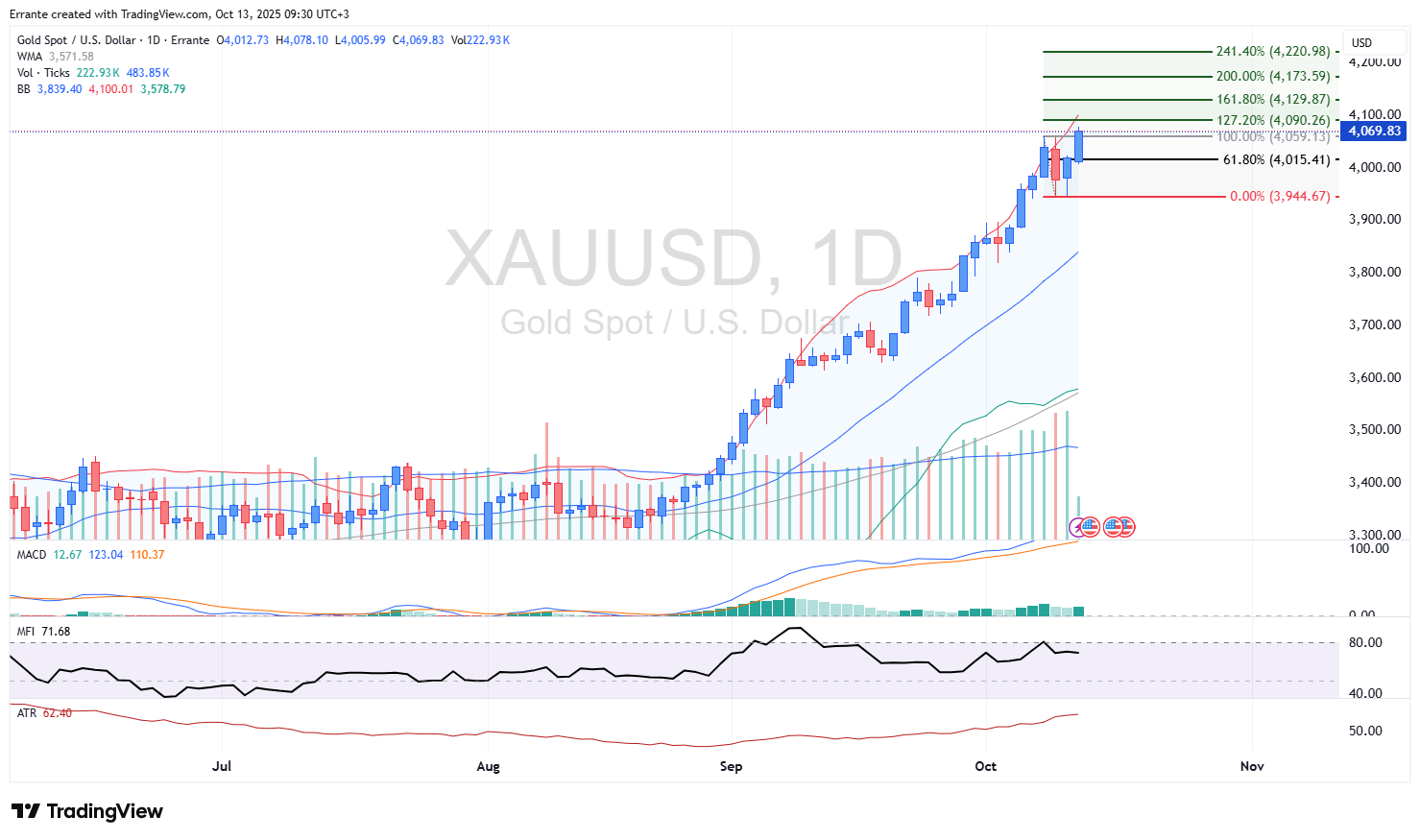

XAU/USD – Gold (Daily)

Gold remains in a strong primary uptrend, consolidating below record highs. Price is holding between $4,015 (Fib 61.8%) and $4,078 (recent swing high), with MACD positive and MFI around 72. Elevated ATR signals breakout conditions.

-

Main scenario: Sustained trade above $4,015–4,059 keeps the upside bias intact. A daily close above $4,078/4,090 would target $4,130 (Fib 161.8%), $4,174 (200%), and $4,221 (241.4%).

-

Key levels:

-

Resistance: $4,078, $4,090, $4,130, $4,174, $4,221

-

Support: $4,059, $4,015, $3,945

-

-

Alternative scenario: A hot CPI or strong NFP lifting real yields could trigger a shake-out. A daily close below $4,015 exposes $3,945; a break there opens a deeper correction toward mid-$3,800s.

NZD/USD – Kiwi (Daily)

NZD/USD trades in a descending channel around 0.5740, below 0.5754 resistance. MACD remains negative; MFI near 46 signals weak demand. The trend remains lower unless the pair reclaims 0.5789 (Fib 61.8%).

-

Main scenario: Prefer selling rallies below 0.5754/0.5789. Failure here keeps pressure toward 0.5729, 0.5698 (161.8%), and 0.5663 (200%).

-

Key levels:

-

Resistance: 0.5754, 0.5789, 0.5845.

-

Support: 0.5729, 0.5698, 0.5663, 0.5625.

-

-

Alternative scenario: A soft US data mix could weaken USD, triggering a daily close above 0.5789 and a run toward 0.5845 and the channel top around 0.5900–0.5950

Key events calendar (GMT+3)

Monday, October 13

• All Day – Canada – Thanksgiving Day.

• All Day – Israel – Simchat Torah Eve.

Tuesday, October 14

• 09:00 – EUR – German CPI (Sep).

• 19:20 – USD – Fed Chair Powell Speaks.

Wednesday, October 15

• 15:30 – USD – Core CPI, CPI (Sep).

Thursday, October 16

• 09:00 – GBP – GDP (Aug).

• 15:30 – USD – Retail Sales, PPI, Jobless Claims, Philly Fed.

• 19:00 – USD – Crude Oil Inventories.

Friday, October 17

• 12:00 – EUR – CPI (Sep).

• 15:30 – USD – NFP, Average Hourly Earnings, Unemployment Rate.

Bottom line

This week’s CPI and NFP releases will act as dual catalysts, potentially breaking the current “Goldilocks” narrative of cooling inflation and stable growth. Traders should be prepared for outsized moves in USD pairs, gold, and US indices. A soft inflation-labor mix supports the risk rally and weakens the dollar; hot data could trigger a sharp repricing of rates and volatility across markets. The interaction between US data, Eurozone CPI, and evolving trade rhetoric will shape the macro tone for the rest of Q4.

Author

Ali Mortazavi

Errante

BEc, CMSA, Member of IFTA - International Federation of Technical Analysis, Associate Member of STA - Society of Technical Analysis (UK).