CPI fuel and the smoldering inflation fire

For all the CPI hoopla, remember that this is a monthly figure – all data tend to fluctuate, especially those heavily massaged ones (substitution, hedonistic adjustments, owners‘equivalent rent coupled with exclusion of certain essentials for their prices are deemed too volatile).

The Fed keeps walking a very fine line, and it‘s a success that the market isn‘t revolting – given the infrastructure bill passing Senate, calls on OPEC+ to increase production, it‘s clear to me that whatever today‘s figure, inflation will keep being a thorn in its side for a long time – as simple as putting 2 + 2 together.

Again, today’s report will be shorter than usual, and focus on select charts so as to drive position details of all the five publications.

Let‘s move right into the charts.

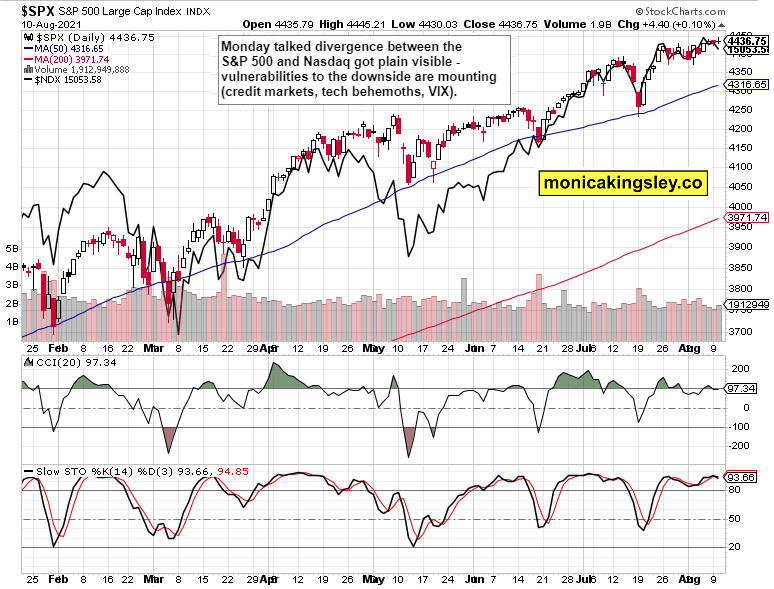

S&P 500 and Nasdaq Outlook

S&P 500 keeps holding up but Nasdaq not very much so – quoting from yesterday‘s analysis:

(…) Yes, Nasdaq is in as precarious short-term position as the 500-strong index – about to fall steeply just as gold did? Probably not, but vulnerable to a corrective move that could easily reach a few percent. The infrastructure bill is rather factored into the expectations, and similarly to Fed taper looming, any surprise could serve as a selling catalyst. The drying up volume may not be a sign of no more sellers here, but rather of combination of timid sellers and drying up pool of buyers. With the strong CPI data likely to be announced tomorrow, the bears would likely try their luck.

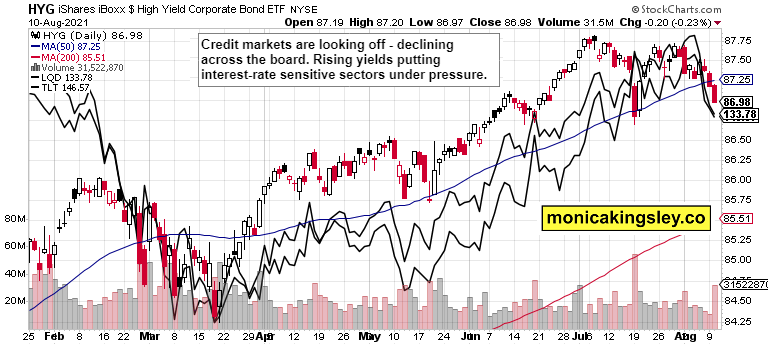

Credit markets

Credit market weakness is catching up ever more with high yield corporate bonds as they are getting under the same kind of pressure as quality debt instruments. Credit spreads are likely to start widening again as we‘re still in an economic expansion, and that would lift stock market spreads such as financials to utilities. Anyway, with rising yields look for the ride in equities to get rockier, and for tech to be diverging – yesterday was a preview of things to come.

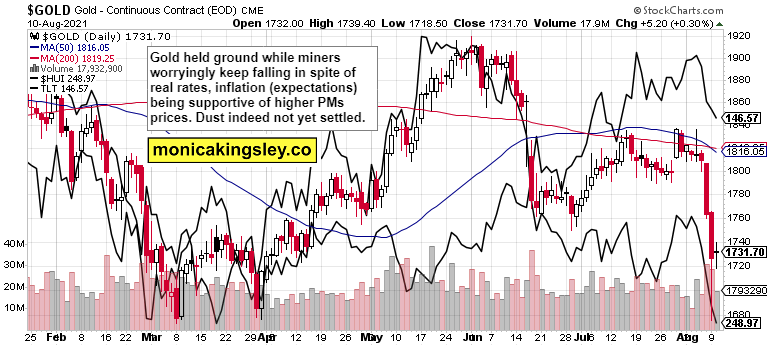

Gold, silver and miners

Yesterday, I made a case for why we‘re at an interesting valuation point in gold and silver. The daily chart view though still looks as bleak as ever – merely price stabilization while miners continue leading lower. The dust hasn‘t indeed settled and the success of Fed‘s June actions is still with us as inflation expectations and TIPS are being ignored:

(...) Does the market seriously believe that the Fed would turn into an inflation fighter? That they wouldn‘t lag behind both the incoming forward looking and lagging inflation metrics? Make no mistake, the June ISM services PMIs were the highest ever – there is plenty of inflation in the pipeline, and you‘re in essence making a bet whether the central bank will duly mop up the excesses, or not. I‘m in the latter camp, and that means the current gold and silver values are highly interesting to the medium-term investor and trader.

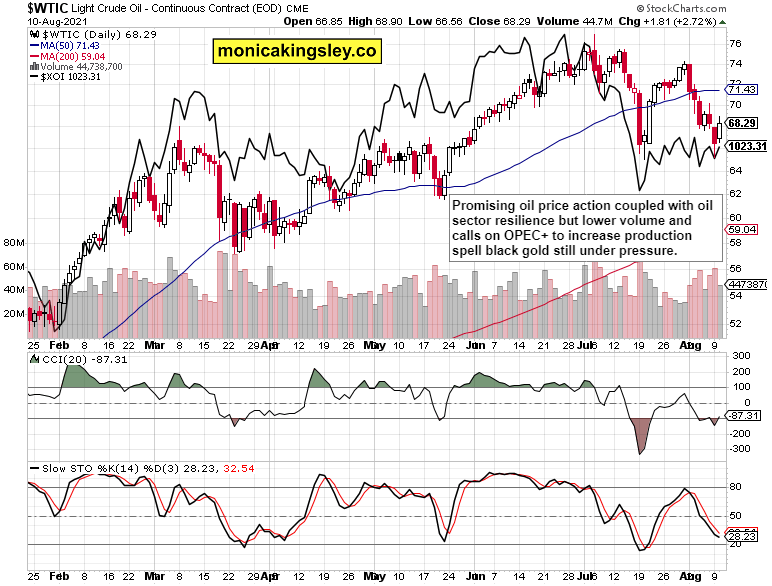

Crude oil

Oil has rebounded off Monday‘s premarket lows, but has met selling pressure even before today‘s message to OPEC+ was announced. I‘m counting on the oil sector continued resilience, but am not looking for similarly smooth sailing in black gold all that fast. Not at all.

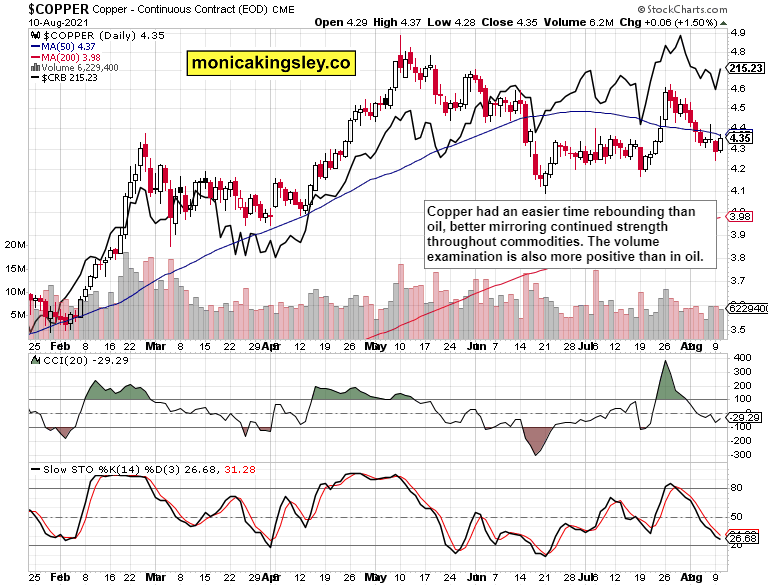

Copper

Copper paints a brighter picture by quite a few hues, and the commodity index has likewise sprang to life vigorously. The 4.20s support zone is likely to hold unless a game changer strikes, which has gotten a little more unlikely compared to yesterday (watching the news tape). The inflation data are more than likely to support real assets, even if they enable the Fed to declare improving economy conditions in Jackson Hole, and announce (watered down) taper (with strings attached) in September. Look for commodities to recover then fast, faster than precious metals.

Bitcoin and Ethereum

The slow motion crypto upswing goes on, without respite – consolidating and likely to continue. More fighting is expected around $48-50K in Bitcoin, but shouldn‘t affect Ethereum all that much.

Summary

In place of summary today, please see the above chart descriptions for my take.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.