Corporate America's Debt Binge: An Issue When Rates Rise?

Corporate debt has risen to 45 percent of GDP, equal to the peak of the previous expansion. Low interest rates and longer payment periods have kept corporate debt cheap, but these trends are beginning to reverse.

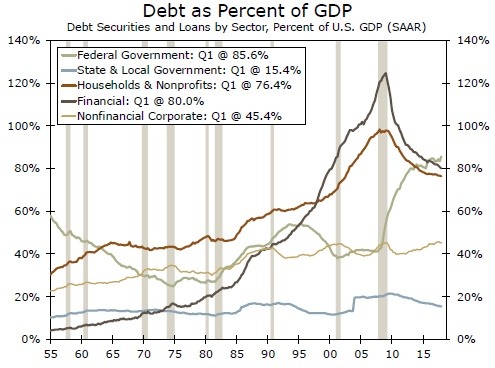

Nonfinancial Corporations Load on Debt

The overall U.S. economy has become less indebted since the Great Recession, with domestic debt outstanding as a percent of gross domestic product (GDP) falling to 330 percent in Q1 from more than 370 percent at the start of 2009. Shrinking debt relative to GDP is mainly due to deleveraging in the household and financial sectors, while debt has grown faster than GDP for government and nonfinancial business (top chart).

Aside from government, the largest debt gains have occurred in the nonfinancial corporate business sector. Corporate debt growth turned positive in 2011 and has averaged 5.8 percent a year since, propelled higher by low interest rates and robust investor appetite for fixed income securities. As a percent of GDP, corporate debt is currently sitting at its highest level of the cycle (45 percent) and is equal to the peak of the previous expansion.

Lower Interest Rates and Longer Payment Periods

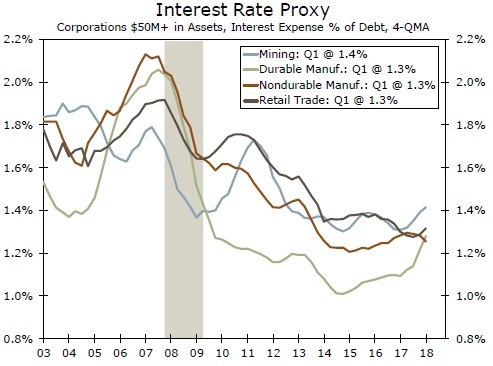

The interest rates corporations are paying on their debt remain far below historical levels, which has helped to keep debt servicing costs low relative to the amount of debt corporations are holding on their balance sheets. We look at interest expense as a share of total short-term and long-term debt as a proxy for the average interest rate paid by corporations (middle chart). This measure fell substantially after 2009 as the Federal Reserve cut the benchmark rate, and remains below the lows of the 2001-2007 cycle for retail trade and all major manufacturing industry categories.

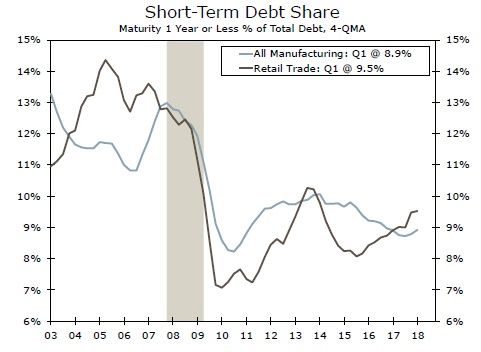

Also limiting the corporate debt burden is a shift toward more long-term debt, which means lower principal payments due in each period (bottom chart). Short-term debt (due in less than one year) represented 9.4 percent of debt held by manufacturing and retail corporations in Q1. This compares to over 13 percent at the end of the previous expansion.

In Q1, manufacturing corporations owed $505 billion on their debt in the coming year (short-term debt plus installments due on long-term debt), while large retail corporations owed $73 billion. These obligations amount to 19.1 percent and 12.6 percent of current assets, respectively. Even though interest rates and the short-term share of debt are lower than during the 2001-2007 expansion, high debt loads mean that debt payments coming due relative to current assets have far surpassed levels of the previous expansion.

But... Debt is Becoming More Expensive

In the past year, the short-term share of debt and the interest rate proxy have risen for corporations, reversing previous trends. Therefore, debt is set to become more expensive. Given strong economic growth and profits, leverage is not overly concerning at present. However, should investor appetite for debt wane or benchmark interest rates go up quickly, funding new debt could fast become more onerous for U.S. corporations.

Author

Wells Fargo Research Team

Wells Fargo