Consolidation continues but a risk positive bias is developing [Video]

![Consolidation continues but a risk positive bias is developing [Video]](https://editorial.fxstreet.com/images/TechnicalAnalysis/Sentiment/businessman-on-arms-outstretched-over-sunset-with-sunbeam-44874496_XtraLarge.jpg)

Market Overview

A couple of weeks ago, markets were all giddy with anticipation of deals. A prospective trade deal between US and China, in addition to a prospective Brexit deal. The reality of politics delivering on what seems to be two very difficult agreements has taken the steam out of major market moves. However, despite the volatility seeping away, there is still a sense that something has changed in both the trade dispute and the Brexit process. On trade, the noises coming from both camps are still positive. Larry Kudlow added to this by noting that the potential for the December trade tariffs to be cancelled if the trade talks go well. This is helping to lend a more positive bias once more to market moves. On the Brexit side, there is a frustration with the progress in the UK Parliament, but one thing has emerged in that the prospects of a “no deal” hardest of Brexits, has reduced. Delay would be tedious and is increasingly likely, but a reduced threat of the nuclear option has helped to sustain a significant sterling rebound. It is interesting to see improved risk appetite and traders leaning away from safer haven options. Treasury yields ticking higher, whilst gold and the Japanese yen have edged lower. A positive bias is also supportive for equities which also have the ramping up of earnings season to contend with. Although definitive direction is still hard to come by, there are signs of positive risk taking hold.

Wall Street closed with solid gains last night with the S&P 500 +0.7% and closing above 3000 for the first time in over a month (at 3007). US futures are showing a continued move higher with +0.2% today. Asian markets have been mildly positive with the Shanghai Composite +0.2% (Japan was closed for public holiday). European markets are trading cautiously higher, with the DAX futures +0.1% and FTSE futures all but flat. In forex, there is a very uncertain look today with little real direction on USD, with mild gains on GBP whilst NZD is the main outperformer. In commodities, gold and silver are fluctuating around the flat line, whilst oil is a shade lighter.

It is a relatively quiet day for the economic calendar today. The UK Public Sector Net Borrowing for September is at 0930BST which is expected to show a deficit of £8.8bn (deficit of £2.0bn in the equivalent month of 2018). Into the US session, the Existing Home Sales at 1500BST is expected to show a decline of -0.7% in September to 5.45m (from 5.49m in August). The Richmond Fed Comp index is at 1500BST and is expected to improve slightly to -7 in October (from -9 in September).

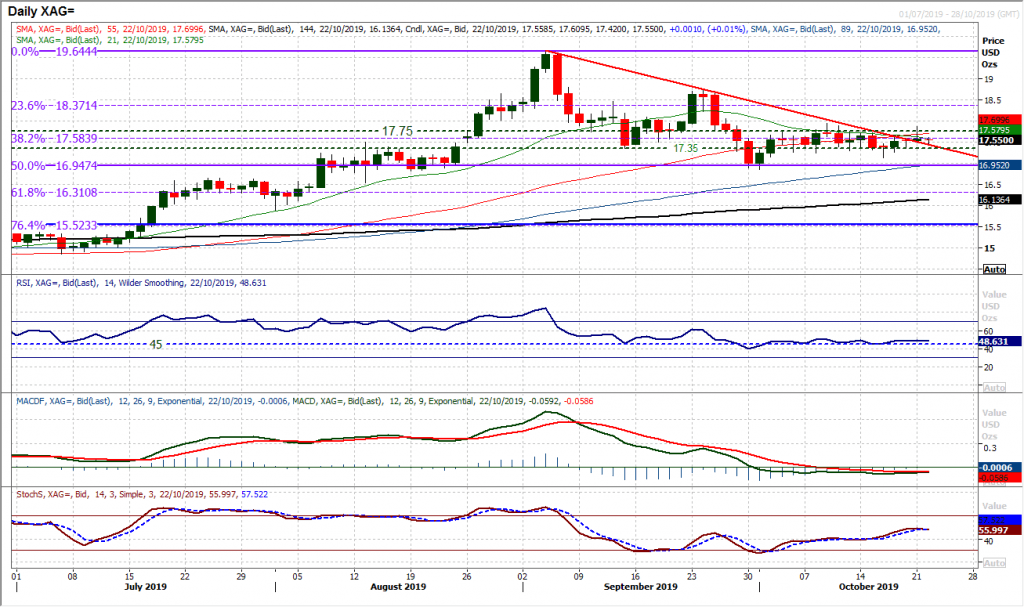

Chart of the Day – Silver

Both silver and gold have been stuck in a rut in recent weeks with precious little sign of any decisive direction. However, are we starting to see silver lead the way higher? A consolidation has driven the market sideways for more than two weeks, but has now broke a downtrend in place since September. This also comes with positive traction beginning to develop on the Stochastics (rising above 50 and at a six week high). However, it is still very early to call recovery. Yesterday’s candlestick would have been mildly disappointing as the bulls gave up a strengthening position as a mini breakout above $17.75 failed. With RSI stuck around 50 and MACD lines flat, this may have been a bit of a false dawn. However, it is important that the market holds above $17.35 support now. It also looks as though intraday corrections are being bought into. The hourly chart shows MACD consistently positioning above neutral for the past three sessions whilst the hourly RSI is consistently above 40. A basis of support is forming $17.35/$17.50. Too early to call a rally, but early signs are developing.

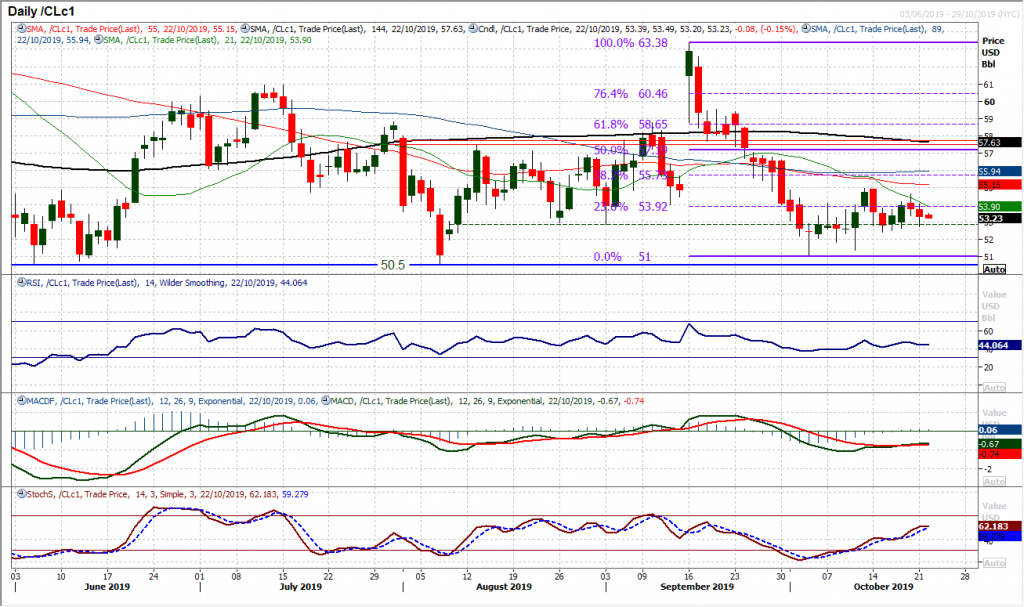

WTI Oil

We discussed previously about the attraction that WTI has to the old support at $52.85 and once more a consolidation has taken over a threatened sense of direction. A couple of mild negative candles have pulled the reins on the positivity from the middle of last week. The market currently sits back in its consolidation area $52.85/$53.90 (the latter being the 23.6% Fibonacci retracement of $63.40/$51.00). With a subdued nature to the momentum indicators (RSI between 40/50 for the past 8 sessions, MACD lines flat), the search for direction and conviction continues. This is a range play, with support at $51.00 and initially at last week’s low at $52.40, whilst resistance is now key around $54.90 and last week’s high of $54.60.

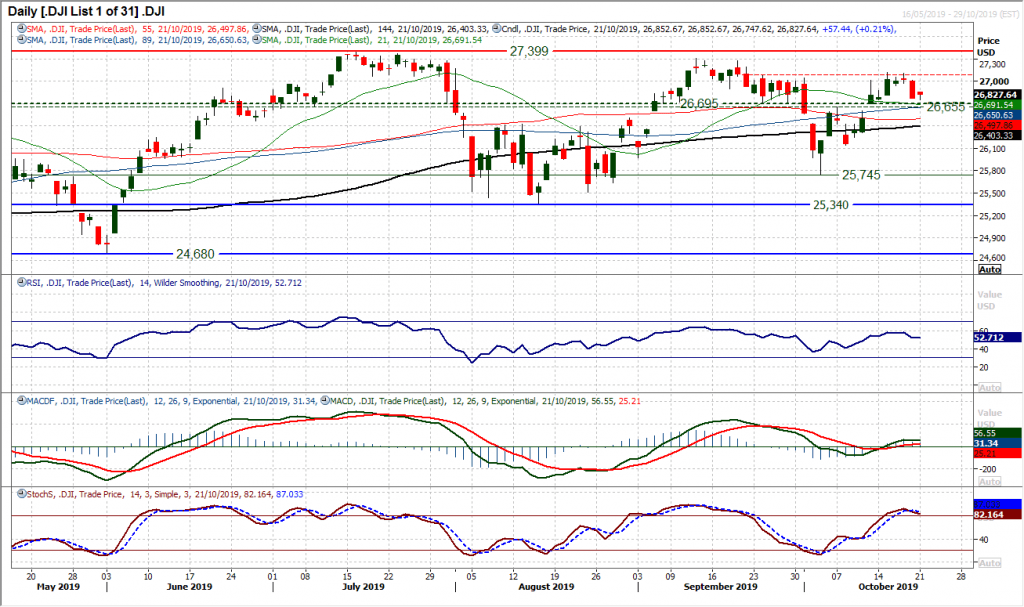

Dow Jones Industrial Average

There has been a degree of support coming in for the Dow again as the pivot around 26,655/26,695 helps to settle the nerves for the bulls. However, it was a far from convincing candlestick in yesterday’s session. Despite closing higher on the day, the bulls never managed to get any traction in a rebound. Given the failing recovery on momentum indicators, there is a sense that the market is finding conditions far from plain sailing. There is a risk that the outlook could turn sour if there were to be any further negative sessions. For now though, trading above the 26,655/26,695 support area and moving averages will lend a marginal positive bias to the outlook, but the bulls are lacking conviction. Resistance overhead between 27,045/27,120 will be the big near term test.

Author

Richard Perry

Independent Analyst