Chinese PMI rebounds as Iran impacts start trickling through

China’s official manufacturing purchasing manager’s index reached a 12-month high of 50.4 in March as sub-indices rebounded across the board, and the non-manufacturing PMI also returned to expansionary territory. We’re starting to see the impact of higher energy prices, which could drag on activity if prices stay higher for longer.

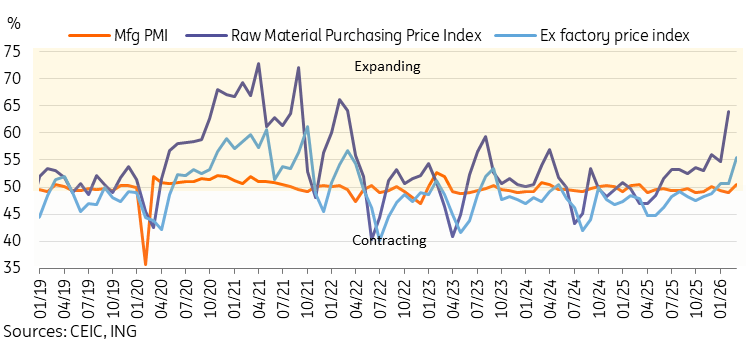

Manufacturing PMI returns to expansion despite Iran War

China's manufacturing PMI rebounded to 50.4 in March, up sharply from 49.0 in February. This came in stronger than market expectations and reached a 12-month high. Although the official PMI and industrial production trends have generally shown looser-than-normal correlation over the past year, they nonetheless suggest a solid start to the year for China's industrial activity.

The recovery was broad-based. Production (51.4), new orders (51.6), new export orders (49.1), and employment (48.6) all increased on the month. The new export orders subindex, in particular, reached its highest level since April 2024, as external demand continues to buoy growth in China.

We’re starting to see some of the impact of the Iran war and higher energy prices in the subindices. First, the purchase price of raw materials subindex surged to 63.9, up from 54.8. This is the highest monthly read since April 2022. Second, ex-factory prices also rose to 55.4, up from 50.6, hitting a 48-month high. This suggests that inflationary pressure is set to pick up in the months ahead. Persistently higher prices could begin to weigh more substantively on activity in the coming months.

Price subindices starting to show impact from Iran war

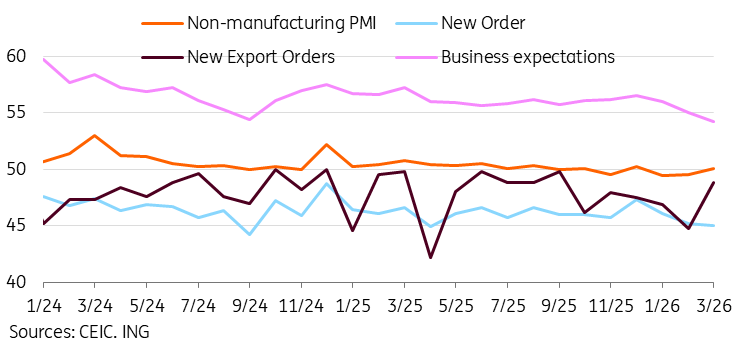

Non-manufacturing PMI also returned to expansion

China's non-manufacturing PMI also beat expectations, rebounding to 50.1 in March. This snapped a two-month contraction streak.

The uptick appears to be primarily due to a smaller contraction in new export orders, which rose to a 6-month high of 48.8 from 44.7. We also saw upticks in input prices in the non-manufacturing PMI index. This is another data point supporting China's reflationary theme. Generally, the other subcategories remained quite soft, indicating that the services sector remains under pressure.

Business expectations, which have consistently been an outperformer in the non-manufacturing PMI subindices, fell to 54.2, the lowest level since 2022.

Overall, PMI data has held up quite well in the first full month since the Iran war broke out. China remains relatively well-positioned to endure short-term disruptions. But if higher energy prices and shipping disruptions persist or worsen, we could see pressure build in the months ahead.

Non-manufacturing PMI barely returns to expansion but subindices still look weak

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.