China’s Slowdown, Australia’s Stimulus, Laffer’s Legacy

China’s economy is slowing by any measure, while Australia’s central bank takes rates to record lows.

Vaibhav Tandon reports on China’s economic performance.

After a gap of three years, my work calendar finally permitted me to celebrate the festival of Diwali with my parents and relatives. We have a pretty big family, with a few younger members. Among them is my six-year-old nephew, who loves to read story books. He was reading the book “The Dragon Who Lost His Fire” by Teresa J. Reasor, a story about a grumpy dragon who struggles to overcome the angry attitude that has stopped him from breathing fire.

The dragon in the children’s tale isn’t the only one working through a difficult transition. The Chinese economy is also struggling to get its fire back. After three decades of incredible growth, the Chinese economy has spent the better part of the past decade gradually losing heat. But the latest run of weak economic data has caused some to wonder whether China has lost its spark.

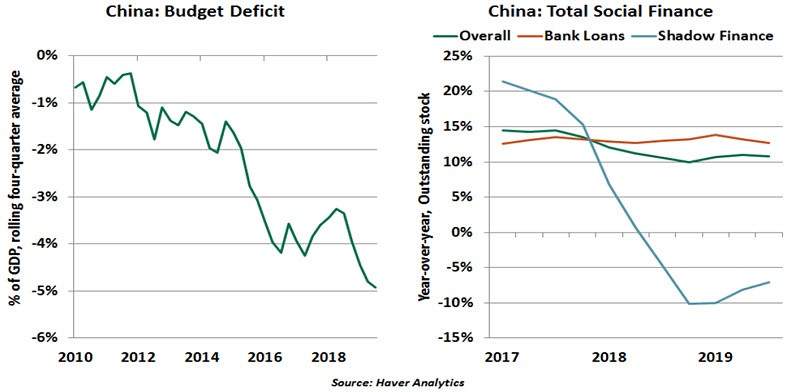

The official Chinese data, the veracity of which is debatable, has painted an increasingly cloudy outlook. China’s real gross domestic product (GDP) growth fell to a 6.0% year-over-year rate in the third quarter, a multi-decade low. Incoming data shows a further loss of momentum: Industrial activity, in particular, remains weak. Auto sales have been contracting since July 2018. Fixed asset investments by businesses have been trending lower.

As illustrated by the purchasing managers index (PMI), China’s tariff-battered manufacturing sector is in retreat. The protracted trade war with the U.S. has caused overall Chinese exports to contract by 1.3% over the past year. Exports to the United States are down a whopping 16% over the same period. Exports to Asian economies like Japan and South Korea have also dropped, implying a shift in global demand and trade flows. The trade war has also prompted several multinational corporations to reassess their supply chains. The broad slowdown and deflation in producer prices have squeezed companies’ profits.

“Underneath official statistics are clear signs that China’s economy is slowing.”

Diverse indicators ranging from freight shipments to factory power generation to expenditures on entertainment are all slowing. China’s office market reached its highest vacancy rate in a decade. Regional banks are failing at an increasing rate. In the first ten months of 2019, 831 local governments entered default, compared to just 100 in all of 2018. Even large cities like Nanchang, the capital of Jiangxi Province, are being sued for defaults. Forcing governments to pay their contractor bills is challenging as there is no formal regulation allowing seizure of government assets to settle dues. Taken together, this bad news suggests official GDP statistics understate the extent of the slowdown. A study by the Brookings Institution revealed that China over-reported its GDP growth by around two percentage points (on average) between 2008 and 2016.

While the country’s formal unemployment rate has remained steady, signs have emerged that sluggish domestic demand and trade frictions with the U.S. have led to increased layoffs in the manufacturing sector. The employment component of the manufacturing PMI has fallen close to levels last seen during the global financial crisis.

The slowdown is spreading to the consumer sector. Consumption is still resilient, but advancing much more slowly. Retail sales consistently grew at a double digit pace between 2008 and 2017, but have now weakened, despite $300 billion in personal income tax cuts. Household spending won’t be enough to prevent the deceleration of headline growth to record lows. Reduced growth in Chinese consumption has hit a few multinational corporations, including U.S. electronics makers and designer fashion brands.

And trade isn’t the only problem plaguing the Chinese economy. The effects of the broader global slowdown and China's deep indebtedness have also played their part. Weak economic activity raises the expectation of additional easing measures, but Beijing’s hands may be tied. Turning away from reforms and returning to large-scale stimulus will likely reduce the risk of defaults, but will also amplify long-term structural problems in the economy.

Such measures might also lead to a downgrade of the country’s credit rating. China’s total debt burden is immense, and requires careful monitoring.

To this point, policymakers have relied instead on more modest measures to underpin the economy, such as cuts to reserve requirement ratios, increased lending to small firms and additional infrastructure projects. However, these targeted measures have not yielded the desired results. Credit growth has also decelerated in spite of notably accommodative financial conditions.

Should the world’s second largest economy and biggest trader succeed in stabilizing its economy without a hard landing, global markets will breathe a sigh of relief. Weaker demand for Chinese imports is not only depressing regional demand for industrial components, but is also putting a lid on commodity prices, including oil. This unsettles commodity exporters like Brazil and Australia.

“Targeted easing measures aren’t working, but policymakers cannot afford to go all out.”

The possibility of a “Phase One” deal with the U.S. is a welcome development, but agreement is not assured and won’t solve all of China’s problems. Any near-term deal would likely be limited in scope, leaving most tariffs in place and several important issues unsettled. Such an agreement would improve sentiment only marginally and leave heavy industry in a difficult position.

The current economic pain could compel China to soften its stance on certain issues, but the country is unlikely to concede on all fronts. China still has sufficient resources to counter a slowdown, should it choose to abandon its reform efforts. Some are suggesting that China will benefit from playing a waiting game and taking its chances with a new U.S. administration. But it is unlikely that any new administration would treat Beijing differently, at least on trade.

The Chinese dragon will have to adapt to a new set of circumstances. China must accept that its economy won’t match its past intensity, and that old ways of managing commerce may be in need of review. Slower but sustainable growth would be China’s best outcome; as my nephew learned, losing some fire is no reason for the dragon to be grumpy.

Curve Ball

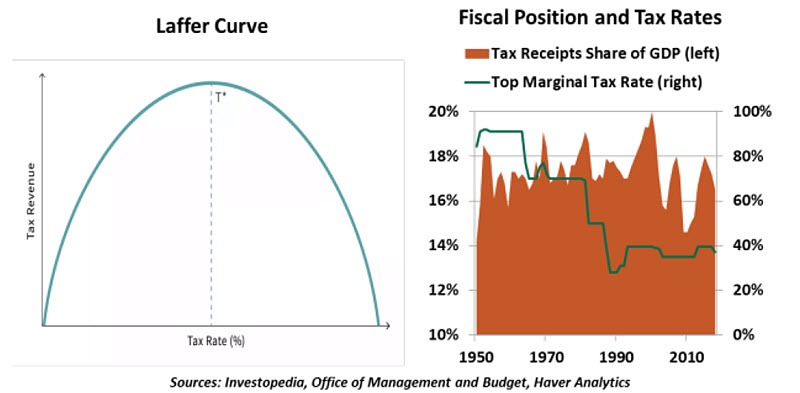

The U.S. government’s right to levy taxes was written into country’s Constitution. And from the moment of ratification, debates have raged over the appropriate structure and level of taxes. In modern discussions, the Laffer Curve is often used to argue that lower tax rates will increase economic activity and put the country into a better fiscal position. While this has been true at times in the past, we do not think it is true today.

The intuition behind the Laffer Curve is clear. A government that sets a 0% tax rate will collect $0 in taxes. On the other end of the spectrum, a 100% tax rate gives no incentive for an economic actor to undertake any productive activity, and results in tax revenues of zero. Reducing the tax rate below 100% will generate some motivation to work, and government revenues will increase. Somewhere between those two extremes, the trends must converge, producing a tax rate that maximizes government revenue.

Art Laffer wasn’t the first to realize this relationship, but the idea gained traction during Laffer’s time as an adviser to U.S. President Gerald Ford. Laffer argued against the notion that a tax increase would lead to an equivalent increase in government revenues, and, as the story goes, sketched the curve on a dinner napkin to illustrate. (The napkin in the Smithsonian Institution collection is a replica.) Laffer’s name was tied to the concept in press coverage at the time.

Laffer’s argument has some basis in historical experience. In 1964, the top marginal statutory individual tax rate in the United States was reduced from over 90% to 70%, with no impairment to the federal budget balance. Though deductions kept many payers below that high rate, we can be confident that a 90% tax rate is on the right-hand side of the Laffer Curve.

Rate reductions since that time have been less supportive, however. Tax reform in the 1980s that brought the top rate down from 70% to 50%, and then as low as 28%, did not lead to a notable increase in government revenues. Subsequent tax rate changes have been relatively smaller but still instructive. A top tax rate increase to 39.6% 1993 was followed by greater revenues and a balanced budget later in the 1990s, suggesting the country was on the left side of the curve. But in every case, many more factors than tax rates combine to paint the full fiscal picture.

“You have to know where you are on the Laffer Curve to understand how tax rates affect tax revenue.”

These experiences suggest that putting the Laffer Curve concept to use is difficult. We can only guess the peak point of the curve, the angle of the slopes on either side and where current or proposed tax rates fall on the distribution. The curve is often used politically to justify tax cuts and argue against tax increases. When politicians or analysts posit that tax cuts pay for themselves, the Laffer Curve is often used as evidence.

The Tax Cuts and Jobs Act (TCJA) of 2017 was, by the Congressional Budget Office’s estimation, poised to reduce tax receipts and increase the deficit over a ten-year horizon. Its supporters used the argument that the tax cut would pay for itself, increasing tax receipts by unlocking more economic activity. Closing the books on fiscal year 2019, we observe that tax revenues did increase. However, many of TCJA’s benefits were front-loaded; as its provisions start to sunset, the federal fiscal position may deteriorate.

The Laffer Curve’s advocates remind their audiences that the fiscal position is a function of both revenues and expenses; greater revenues are moot if spending also increases. The U.S. deficit’s climb to just shy of $1 trillion in 2019, during an interval of peace and economic growth, seems out of place. In the event of a downturn, the government will have less fiscal space for stimulative reforms. From our current position on the Laffer Curve, increasing taxes may be a necessary and effective way of keeping debt and deficits from spiraling out of control.

Wonder Down Under

To an outsider, Australia is in an enviable position. Its economy continues its record expansion: 28 years and counting. The country has excellent balance between services and commodities. Australia has been hindered by global trade frictions, but has done a decent job of maintaining good relations with both China and the United States. Thanks to enlightened immigration and retirement policies, the country is positioned to withstand upcoming demographic challenges better than almost any other developed country.

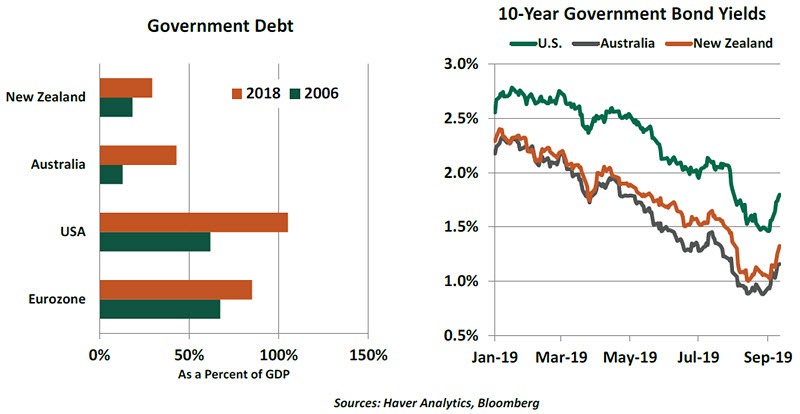

Yet my recent visit to the Antipodes revealed considerable anxiety among the population and policy makers. Growth is proceeding, but its pace has diminished. Flagging Chinese demand has led the price of iron ore, a key Australian export, to fall by one-third since midsummer. Australian property prices remain elevated relative to incomes, and household debt in the country is exceptionally high. Local economists are assigning a 25% probability of recession in Australia next year.

In response, the Reserve Bank of Australia (RBA) has brought short-term interest rates down to a record low. International investors have had a strong appetite for Australian government bonds, which has brought long-term yields in Australia to a record low as well. Easy financial conditions should help put a floor under economic growth, but monetary officials fret over the dwindling supply of “dry powder” that could be used should a recession come about.

The RBA has consequently been exploring alternative forms of monetary policy, like quantitative easing. But there is a much better solution. Australia is running a budget surplus at the moment, which seems at odds with what the economy needs. The country also has a low level of national debt, which leaves plenty of room for fiscal expansion.

The Australian Treasury has traditionally hewn to a very conservative budget policy, and deficits have historically been damaging to political fortunes. But like other countries, Australia must recognize that monetary policy has its limits. And when those limits are approached, fiscal policy must step forward.

Author

Northern Trust Economic Research Department

Northern Trust