China: Exports to lift Q2 growth, container rates stay high for now

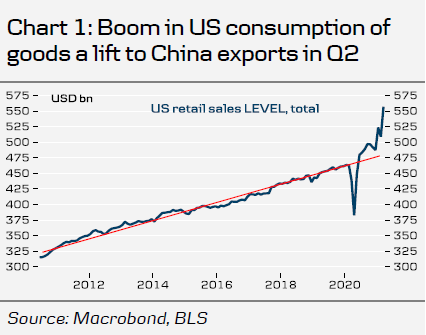

Exports to see lift in Q2: While US consumption of services has been weak, American households have spent a lot of money on goods after receiving new stimulus checks in March (chart 1). This is giving a short-term boost to Chinese exports and manufacturing in Q2 as US inventories are drawn down and US retail sales is likely stay elevated in the short term. China is still to a large extent the ‘factory of the world’. PMI export orders from NBS rebounded in March to a high level and our model points to more upside in the coming months. In H2, we expect the slowdown in China manufacturing to resume due to weaker growth in housing and infrastructure and a transition in the US and euro area consumer spending back towards services from goods.

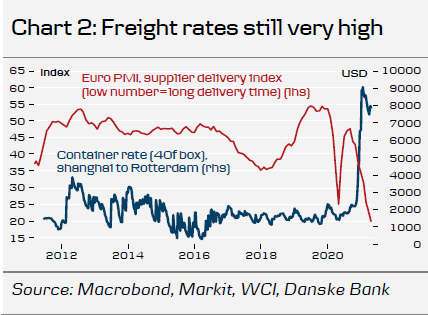

Freight rates and delivery times stay elevated for now: With the strong demand for goods there is little respite for container freight rates or delivery times, which stay elevated (chart 2). The blockage of the Suez Canal did not help. However, we look for a gradual decline in rates and delivery times during Q3, as 1) goods spending moderates again, 2) more shipping supply enters the market and 3) vaccinations reduce port congestion as port workers will again run at full time.

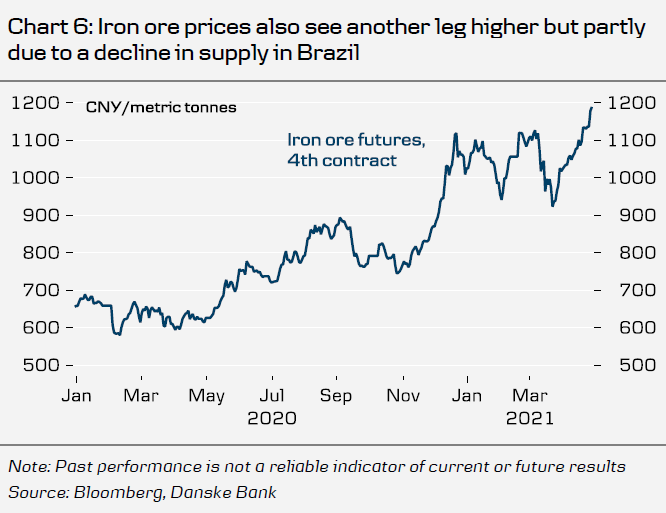

Metal prices rally again: Industrial metals such as copper and aluminium have rallied again lately in another sign, that manufacturing is still growing at a robust pace (chart 5). Iron ore prices have seen a new leg higher as well (chart 6) but it’s partly related to production challenges in Brazil.

Financial risks resurfacing: State-owned financial company Huarong Securities came under severe pressure lately after concerns arose about its financial health with little signs the government would bail it out. A failure to report 2020 earnings by the March 31 deadline triggered fears of looming bankruptcy and its’ dollar-denominated perpetual bond dropped as low as 45 in price from above 100. Losses spread to other companies in a sign of contagion as a reassessment of the previous implicit state guarantee is taking place. Calm has been restored, though, as Chinese regulators have asked some banks not to withhold loans in a sign that it will not be allowed to go bankrupt after all but might instead be restructured.

USD/CNY falls back again: A renewed weakening of the USD has also pushed down USD/CNY back below 6.50. On a 12M horizon we still look for the USD to strengthen, though, and USD/CNY to trend higher.

US and China to cooperate on climate: At least in one area, the US and China have agreed to cooperate. That was the main result of a meeting in Shanghai between John Kerry and Chinese special envoy on climate Xie Zhenhua (see joint statement). A few days later Chinese President Xi Jinping participated in US President Joe Biden’s Leaders Summit on Climate. China made no new commitments but has already vowed to peak emissions no later than 2030 and reach carbon neutrality in 2060. Xi Jinping also stated China would “strictly control coal-fired power generation projects”.

Vaccinations continue at 2-2½% pace per week: A total of 225mn vaccines have now been administered corresponding to 16% of population.

Author

Allan von Mehren

Danske Bank A/S