Central banks: The need and courage to act

Elevated inflation, if left unaddressed, could cause a de-anchoring of inflation expectations, an increase in risk premia, greater price distortion and hence longer-term costs for the economy. Although at first glance, central banks face a dilemma – hiking interest rates to lower inflation at the risk of causing an increase in unemployment or focusing on the labour market and accepting the risk that inflation stays high for longer –, they can only choose between acting swiftly or face an even bigger challenge later to bring inflation back under control. Recent statements by officials of the Federal Reserve, the ECB and the Bank of England acknowledge the need to act but their decisions and guidance are very different and reflect the differences in the macro environment.

In 2015, former Federal Reserve chair Ben Bernanke published ‘The courage to act: a memoir of a crisis and its aftermath’. The title springs to mind when watching the recent press conferences of Fed chair Jerome Powell and Bank of England governor Andrew Bailey1 as well as reading a recent speech of Banque de France governor François Villeroy de Galhau2.

Bernanke’s book provides great insight into the global financial crisis of 2008-2009, its causes, consequences and the policy action it necessitated. Today, the crisis is about elevated inflation and the longer-term cost it would entail if left unaddressed. There is clearly a need to act but it takes courage, considering that, firstly, part of the jump in prices is caused by a negative supply shock, which acts as a headwind to demand and, secondly, monetary tightening will slow down growth and may even cause an increase in the unemployment rate.

In this respect, A. Bailey was particularly clear. Although the unemployment rate in the UK is expected to decline further in the nearterm, to 3.6% in the second quarter, it is projected to reach 5.5% in three years’ time given the sharp slowdown in activity, to which monetary tightening will have contributed. J. Powell acknowledged that “there may be some pain associated with getting back to that [i.e. bringing inflation back to target]”3. This looks like a highly uncomfortable dilemma, but, according to the central bankers, the way to react is clear. “The big pain is in not dealing over time, is in not dealing with inflation, and allowing it to become entrenched.”4 A similar point was made by F. Villeroy de Galhau: “entrenched inflation would mean less confidence, higher risk premia, and greater price distortion, hence less long-term growth.”

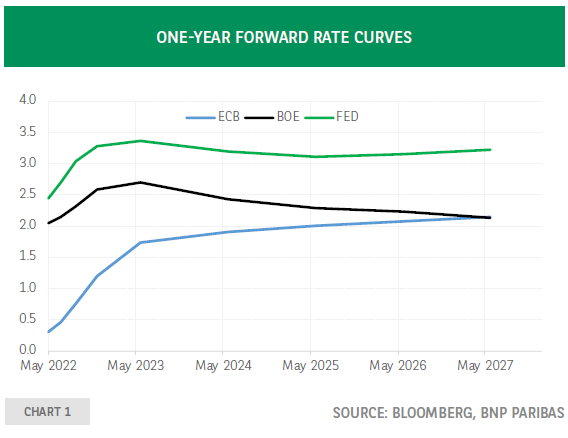

Although the three central banks have a shared objective – bringing inflation under control –, markets expect their respective journeys to be very different (chart 1). This is a reflection of differences in terms of guidance and macro environment. Quoting A. Bailey, “the United States is facing what looks like a demand shock…, the euro area by contrast is facing a supply cost shock… and in the UK we’re seeing elements of both, like the euro area we’re experiencing a sharp terms of trade shock… but our strong labour market is more akin to that in the US.”

In the US, global supply shocks, strong demand and a very tight labour market force the Federal Reserve to tighten ‘expeditiously’5. After the 50bp rate hike at its May meeting, similar increases should follow at the next couple of meetings. Moreover, the reduction of the size of the balance sheet will start in June, although the economic effect is hard to assess with any precision.

In the euro area, the approach will be far more gradual. Compared to the US, the supply shocks play a bigger role, it is more exposed to geopolitical uncertainty caused by the war in Ukraine, wage growth is slower and the labour market is under less pressure than in the US. Based on recent statements of several ECB governing council members, a July hike of the deposit rate looks increasingly likely and more increases should follow.6

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.