Central banks, markets and the economy: Three times wrongfooted

In the US, financial conditions have eased in recent months and weighed on the effectiveness of the Fed’s policy tightening. Jerome Powell recently gave the impression of not being too concerned, so markets rallied, and financial conditions eased further despite the hawkish message from the FOMC. In the Eurozone, another rate hike by the ECB and the commitment to raise rates again in March caused a huge drop in bond yields because markets expect we’re getting closer to the terminal rate. It reflects a concern of not being invested in the right asset class when the guidance of central banks will change: based on past experience, one would expect that bond and equity markets would rally when central banks signal that the tightening cycle is (almost) over. However, as we have seen with the surprisingly strong US labour market report, such positioning comes with the risk of being wrongfooted by the data. What follows is huge volatility.

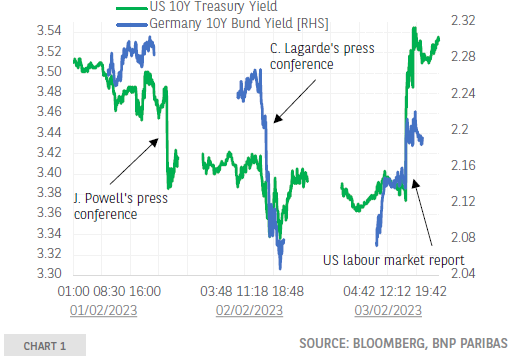

Financial markets are a key channel of monetary transmission. Changes of official interest rates, or expectations thereof, influence the level of government bond yields, corporate bond spreads, equity markets and the exchange rate. Together, they represent financial conditions faced by borrowers and investors whose decisions influence the real economy. It explains why central banks and investors pay particular attention to the evolution of these financial conditions. In the US, they have eased in recent months (charts 2-5) despite the aggressive rate hikes by the Federal Reserve. Treasury yields, corporate bond yields and their spreads versus Treasuries have declined, equity markets have rallied, and the dollar has depreciated. Such easing of financial conditions reduces the effectiveness of official rate increases, so Fed watchers were keen to learn whether Jerome Powell would express an opinion on the topic during his latest press conference. He did so in answering a journalist’s question[1] but by saying that the Fed’s focus is not on short-term moves, he gave the impression of not being too concerned. Unsurprisingly, markets rallied, and financial conditions eased further (chart 1). Not exactly what the Federal Reserve had hoped for with its otherwise hawkish message.

Intraday reaction of 10-year yields

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.