Central bankers switch gear; EUR/NZD reversal

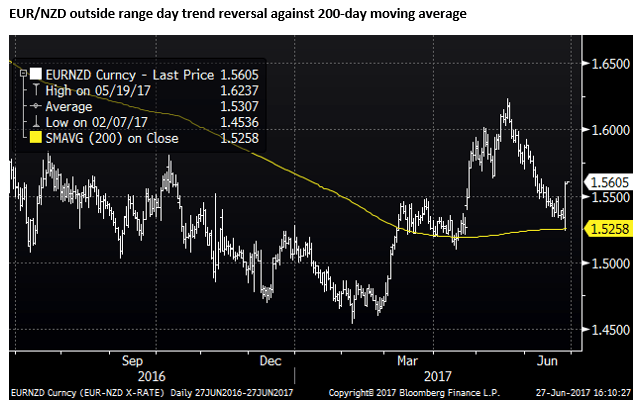

The EUR is on the fly Tuesday after a month or more of consolidation. The catalyst is a speech from Draghi. Coming on the back of a number of more optimistic central bank noises in recent weeks, the market may feel there is something coordinated about these events. As we discussed in our report yesterday, central banks are shifting their focus surreptitiously from inflation targets to real interest rates and financial conditions. In terms of hawkish or less dovish surprises, count the Bank of Canada on 12 June (Speech by Deputy Governor Wilkins), the FOMC meeting on 14 June, the Bank of England 5-3 vote split on 15 June, Bank of England Chief Economist and MPC member Haldane speech on 21 June, Fed Dudley speech on Monday 26 June, and ECB’s Draghi speech on Tuesday, 27 June. The Fed’s Yellen and Fischer also suggested they see risks in recent low levels of global risk premia. We can include the Reserve Bank of Australia in the movement, since it has accepted a lower glide path back to its inflation target in deference to its concern over high house prices and household debt. As mentioned in our report yesterday, this is a warning to equity investors. Equities are already showing fatigue and are vulnerable to a significant correction. Central banks are effectively encouraging some rise in real bond yields. We have noted in the past that the more highly indebted households, in New Zealand and Australia, leaves their currencies more vulnerable to rising global bond yields. The EUR has surged against the NZD, forming an outside range day trend reversal against the 200-day moving average.

Central banks switch gear

The EUR is on the fly Tuesday after a month or more of consolidation. The catalyst is a speech from Draghi. Coming on the back of a number of more optimistic central bank noises in recent weeks, the market may feel there is something coordinated about these events.

An interesting feature of these events is that most, with the exception of the Bank of England, have come despite lower inflation outcomes (sharply lower in fact) in the USA and Canada, and stable Eurozone inflation, and a recent slide in oil prices.

Central bankers are expressing confidence in their medium-term inflation forecasts and models that predict tightening capacity will, given enough time, return inflation to target, notwithstanding what most see as temporary low-inflation trends.

A common theme is that these central bankers are expressing confidence in a broader and more sustained global economic recovery, reducing downside risks and improving their outlook for growth in their tradable goods sectors.

Some of these events, in particular, Dudley’s speech on Monday, and to some extent Draghi’s speech on Tuesday (although certainly much more cautiously), the message is that easing financial conditions helps justify the removal of policy accommodation.

While there were no explicit linkages in BoC’s Wilkins speech on 12 June, one has to suspect that the rapid rise in house prices and household debt was featuring in the Bank of Canada thinking when it signaled a shift to a tightening bias. The Reserve Bank of Australia, since around October last year has made its concern over high house prices and household debt a reason to avoid further rate cuts and accept a lower glide path back to its inflation target.

The theme here is that central bankers are moving towards addressing financial stability concerns now that the economic recovery is looking more secure and asset markets look a bit bubbly, and they are de-emphasising their inflation objectives.

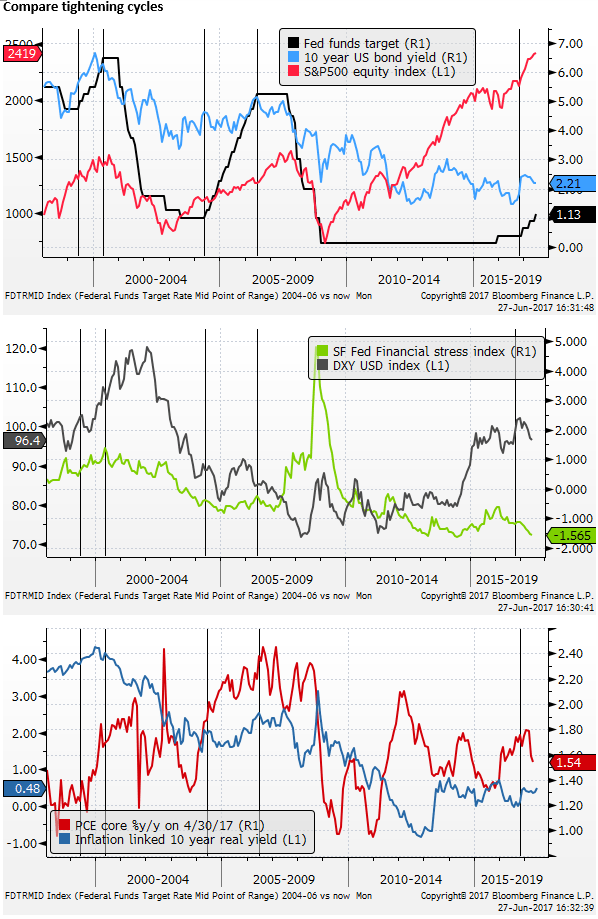

Looking through the lense of the mid-2000s savings glut

Many commentators have been viewing the recent policy tightening steps by the USA, three hikes since December last year, and the announcement of asset (Treasury and Agency bonds) holdings unwind plan, through the lense of the Fed’s steady policy tightening path from 2004 to 2006.

The common theme is that both the 2004/2006 experience and the recent experience appeared to occur in the context of easing financial conditions. Even though in the early period, the Fed were tightening twice as fast (25bp at every meeting, at six-week intervals), long-term bond yield tended to fall during the early phase of these tightening cycles and the stock market continued to rally. In essence, it did not feel like policy was being tightened; financial conditions were little changed or eased.

Former Fed Chairman Alan Greenspan was the principle architect of the 2004 to 2006 tightening cycle. He took care to send a message that the policy tightening path was on a gradual and stable trend to ensure it did not shock the market. Similar to recent Fed’s gradual guidance.

Both Greenspan and his replacement in 2006, Bernanke, spoke of a ‘savings glut’ holding down bond yields despite the policy tightening. For the most part, this reflected a large current account imbalance between the US and China and a number of other Asian countries, and these Asian countries pursuing stable currency policies and hoovering up US Treasuries. The stable bond yields at the time were perhaps more surprising in that US inflation was above the 2.0% target and rising, such that real yields were falling through the first half of this 2004/06 period.

The mistake, well-documented hindsight, was that Greenspan Fed did not fully appreciate the financial stability risks that were building up during this period, culminating in the 2007/2009 period of financial crisis.

The lesson from this period featured in Dudley’s speech on Monday when he used this period to illustrate the importance of taking account of financial conditions when calibrating monetary policy. He said, “For example, during the mid-2000s, financial conditions failed to tighten even as the Federal Reserve pushed its federal funds rate target up from 1 percent to 5¼ percent.”

Dudley suggests that the Fed should have tightened faster or made noises that it might have to if investors did not control their risk-taking.

Looking through the lense of the late-1990s Dotcom boom and bust

Since we are looking at parallels with past episodes, the speech by Dudley on Monday suggests that Fed the may be channeling some of the messages Greenspan sent during the earlier policy tightening cycle that preceded the popping in the ‘Dotcom bubble’ (from April 1999 to Jun-2000).

A key similarity between now and then is that policy tightening began when inflation was well below the Fed’s 2% target. At that time Greenspan focused more on real interest rates and bringing them into line with real economic growth to better balance the economy and risk taking. He was at that time, perhaps belatedly, more concerned with the high and rising equity market than he was with the excesses in the mid-2000s that were more related to the housing market.

In the current conditions, inflation is not the primary concern either, but Dudley’s speech suggests that he has become more wary of rising equity prices and broader evidence of excesses in financial markets that suggest they may need to tighten rates even if inflation is not an imminent threat. In essence, it appears he sees room to raise real interest rates to limit potential unwanted financial stability risks; in a similar vein to Greenspan in the late 1990s. The tight labour market helps justify policy tightening now and then.

The fact that inflation is still below target suggests that some policy accommodation is still appropriate, such that effective real rates across the yield curve should still tend to be below potential growth, and risk premiums for credit and equity capital should be still below average. However, the recent evidence suggests these risk premiums and long-term real yields may not be reflecting any policy tightening to date; and thus Dudley is emboldened to push on with policy tightening, even if recent economic activity and inflation data have been underwhelming.

As we discussed yesterday, the views expressed by Dudley should be a warning to equity investors. Stocks have already been showing fatigue recently, and a Fed that is prepared to persist with its policy tightening path, despite lower inflation outcomes and stalling activity, is generating risk of a substantial correction.

Fed vs. the data, Dudley writing calls on the S&P, 27 June

Draghi – confidence, persistent and prudent

Draghi’s speech today was much more cautious, but had some of the same themes.

Draghi said, “So for us to be assured about the return of inflation to our objective, we need persistence in our monetary policy”. In other words, we should expect a long period to come of QE and low rates.

However, he also said, “We need prudence. As the economy picks up we will need to be gradual when adjusting our policy parameters, so as to ensure that our stimulus accompanies the recovery amid the lingering uncertainties.” It’s subtle, but prudence here means we need to reduce stimulus (carefully, mindful of the risks) as the economy approaches its potential.

He laid the groundwork for a tapering in policy next year, saying, “As the economy continues to recover, a constant policy stance will become more accommodative, and the central bank can accompany the recovery by adjusting the parameters of its policy instruments – not in order to tighten the policy stance, but to keep it broadly unchanged.”

Illustrating that, like Dudley, he is mindful of financial conditions, he said, “But there is an important caveat that we need to consider. Financing conditions are not only determined by the calibration of central bank instruments, but also by other market prices, some of which are significantly affected by global developments.”

These are hardly what you would describe as hawkish comments, and yet it did appear that German bund yields led the rise in US yields on Tuesday.

Perhaps it is the case that the market has gotten more tuned into the evidence that central banks more generally are shifting gear, and Draghi’s comments bring the ECB into this realm as well.

Euro yields and the EUR exchange rate were probably also impressed by the broader sense of confidence Draghi displayed in his speech. Reiterating and placing more emphasis on the messages he delivered at the last ECB policy meeting in which the ECB removed its assessment of downside risks for the economy and said the risk of deflation had disappeared (even though it downgraded its inflation forecasts) and expressed confidence that the ECB would achieve its 2% inflation mandate in the medium term.

In this speech, he said, “The threat of deflation is gone and reflationary forces are at play.” He also spoke extensively about the reasons for the slow response in inflation to the closing output gap, describing these forces as “temporary” that “should not affect medium-term price stability”. In essence, be patient, we are more confident we will get there.

The EUR has consolidated for around a month, setting the scene for its break up today. The gains are supported by relatively strong growth momentum, a much improved political environment, and an Italian government bank bailout that appeases voters and strengthened regional financial assets.

While EUR was breaking, up, NZD responded to the correction in US and global bond yields, generating a rapid reversal in the EUR/NZD cross. It would not surprise if this new trend continues for the time being.

Author

Greg Gibbs

Amplifying Global FX Capital

Greg has had a long career in foreign exchange. He began his career at the Reserve Bank of Australia in 1989 and in the early 1990s he was the first economics graduate at the Bank to be assigned to the foreign exchange dealing desk.