Can positive sentiment continue as US earnings take hold?

Market Overview

Perhaps something to do with the upcoming Easter public holidays, but major markets appear to be in a period of relatively calm. Traders await news of further traction in trade talks whilst lacklustre US earnings just pulled the reins on sentiment yesterday. After all the positives of US corporate announcements at the end of last week (JP Morgan and Disney), Monday’s session was a bit of a damp squib as Goldman Sachs and Citigroup took wind out of the sails. Despite this, earnings season has kicked off in decent shape, as 85% of companies have beaten earnings estimates. Traditional lowballing of guidance aside, this is still ahead of the average around 72%. Beyond this though, it will still be forward guidance for the rest of 2019 which determines how well markets emerge. Broader markets have a risk positive skew still as trade talks with US and China seem to be entering the end phase. To get them over the line, it could be all about the “enforcement mechanism”. Perhaps if the US accepts that compliance with the agreement is a two way street, then this dispute can all be put to bed. The risk positive outlook of last week has pulled equities and yields higher, whilst gold and silver teeter on the brink of key support.

Wall Street closed cautiously lower, with the S&P 500 -0.1% at 2905, but with US futures a touch higher by +0.2% the marginal positive bias continues. Asian markets were higher overnight with the Nikkei +0.3% and Shanghai Composite +1.5%. European markets also look solidly higher with FTSE futures +0.2% and DAX futures +0.3%. In forex, there is more of a cautious look to moves, with the yen performing well, whilst the dollar is also edging some gains. The Aussie is underperforming after the RBA minutes increased the potential for a rate cut. In commodities, gold and silver remain under pressure whilst oil is slipping again within its recent consolidation.

The outlook for UK employment in February is the first key announcement of note on the economic calendar. UK Unemployment at 0930BST is expected to remain at 3.9% (3.9% in January) whilst Average Weekly Earnings growth is expected to improve slightly to +3.5% (+3.4% in January). The German ZEW Economic Sentiment is at 1000BST and is expected to post a positive reading at +0.8 in April for the first time in a year (-3.6 in March). The US Industrial Production for March is at 1415BST and is expected to be +0.2% on the month (+0.0% in February) with capacity utilization expected to remain at 79.1% (after an upwardly revised 79.1% in February).

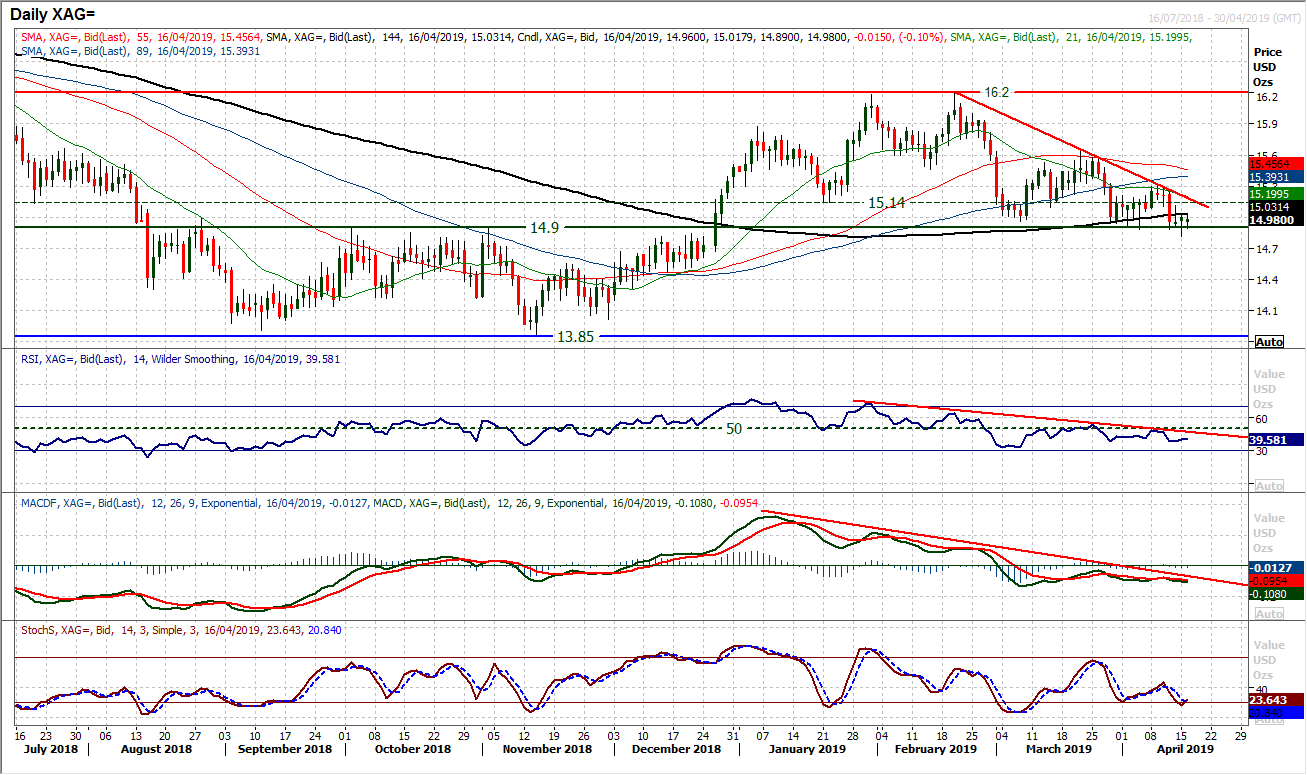

Chart of the Day – Silver

Silver broke key support at $14.90 on an intraday basis in a move that will make gold bulls extremely nervous. Despite rebounding to close above $14.90 this is a big warning sign. (What could this now mean for the crucial $1276 support on gold?) On a medium to longer term basis the support at $14.90 has been a key neckline pivot. However, an intraday breach yesterday took the market to a four month low. With a series of bear signals, momentum indicators confirm the deterioration and there is further downside potential. The RSI has been tracking lower for almost three months and under 40 has further downside potential, as do the MACD lines crossing back lower and similarly the Stochastics. A closing breakdown below $14.90 threatens and would mark a significant downside break. It would open $14.46 as the next support but also means that if momentum really takes hold, a retreat towards $13.85/$14.00 support band could be seen. With a two month downtrend playing out, any unwinding move which fails between $14.90/$15.14 will become a chance to sell.

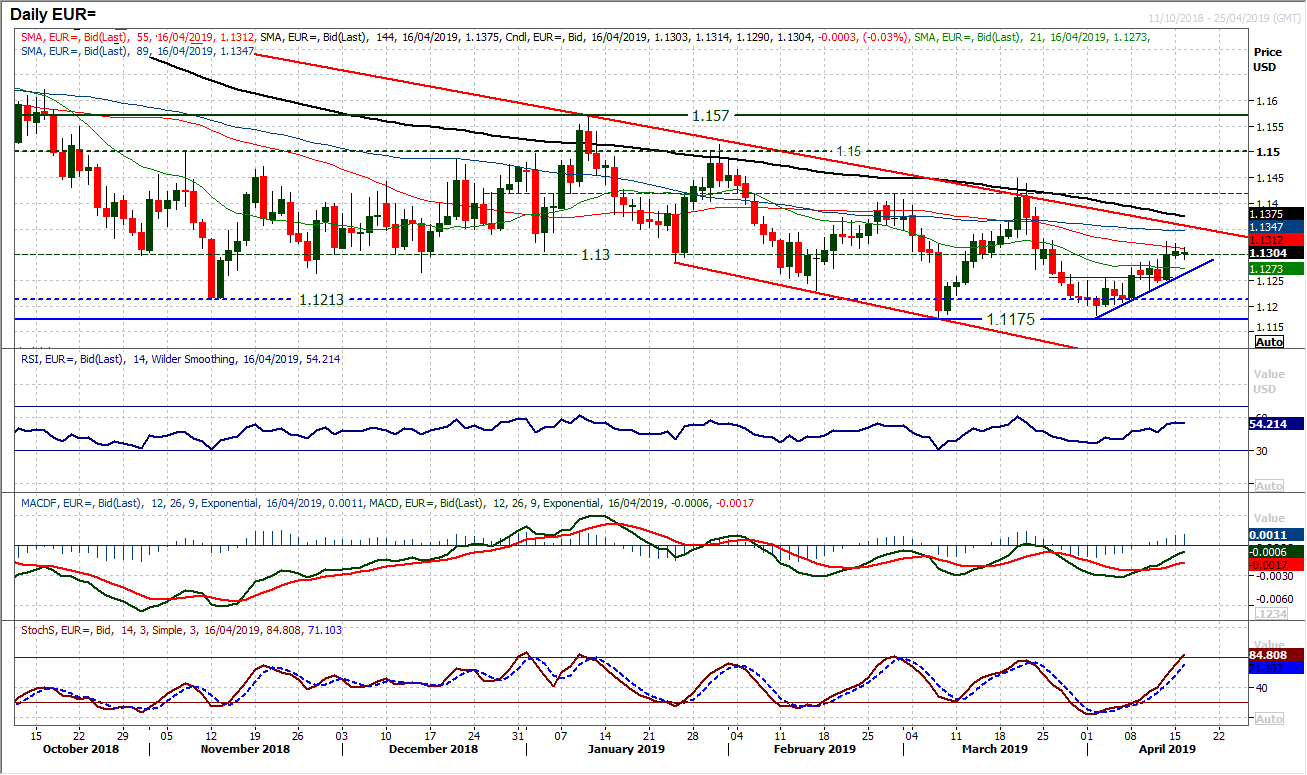

A day of considered consolidation yesterday has seen the euro recovery stall a touch. However, whilst the market continues to run up the two week uptrend, weakness is a chance to buy. Momentum indicators continue to improve, with the RSI above 50 and having upside potential, whilst Stochastics and MACD lines accelerate higher. Whilst the market may have stalled around $1.1325 yesterday, support is forming around the latest near term breakout at $1.1290. The hourly chart shows how momentum indicators have this morning unwound to areas where the buyers tend to resume control. There is a good near term support band $1.1250/$1.1290 now. A move towards the medium term downtrend channel at $1.1355 today is developing.

As the market has consolidated in the past week there is the slightest hint of a move higher threatening. The resistance of the five week downtrend (today at $1.3110) is being tested. However, the market is still struggling for any sustainable upside traction. Can the tick higher on momentum indicators start to develop? Last week’s high of $1.3130 is a barrier that needs to be overcome on a closing basis to suggest that the bulls are beginning to find their feet. However the lower high around $1.3200 is still the main near term resistance. Despite this, there is support building above $1.3000 with $1.3030/$1.3050 being a near term buy zone. There is the slightest positive bias on hourly momentum, but not enough for any real conviction.

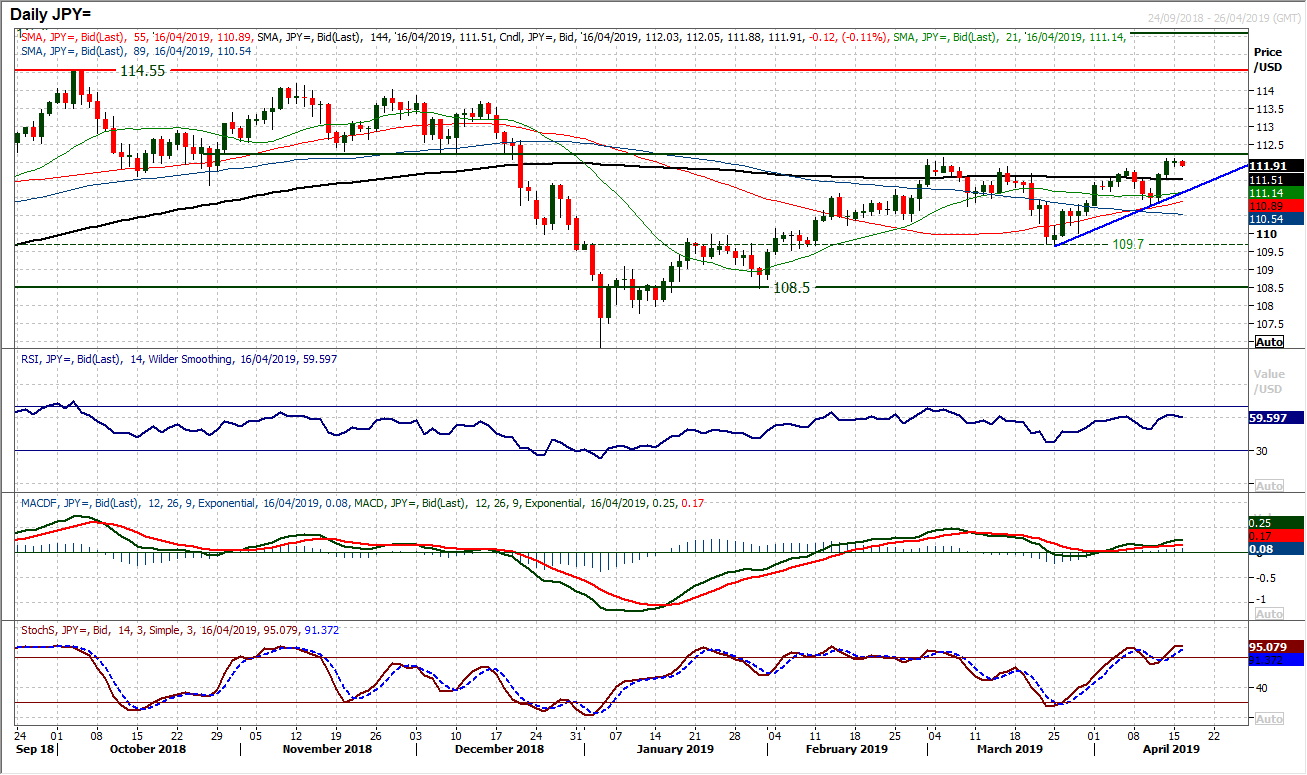

Testing the resistance at 112.10 the bulls have just been unable to generate the sustained traction to make the break. A very tentative session of just 22 pips of range yesterday. This is being followed by further regard to the resistance at 112.10 today as the market again slips. There is an uptrend of the past three weeks (which comes in at 111.15) which suggests weakness is a chance to buy. Positive configuration on daily momentum reflects this. However, there is also a tentative approach to the rally and the resistance at 112.10 and then overhead from the November/December lows 112.20/112.30 which could begin to restrict the upside once more. The importance of support at 110.85 is growing. The hourly chart shows that whilst 111.60/111.80 is intact as support, there is still a positive bias to the near term moves.

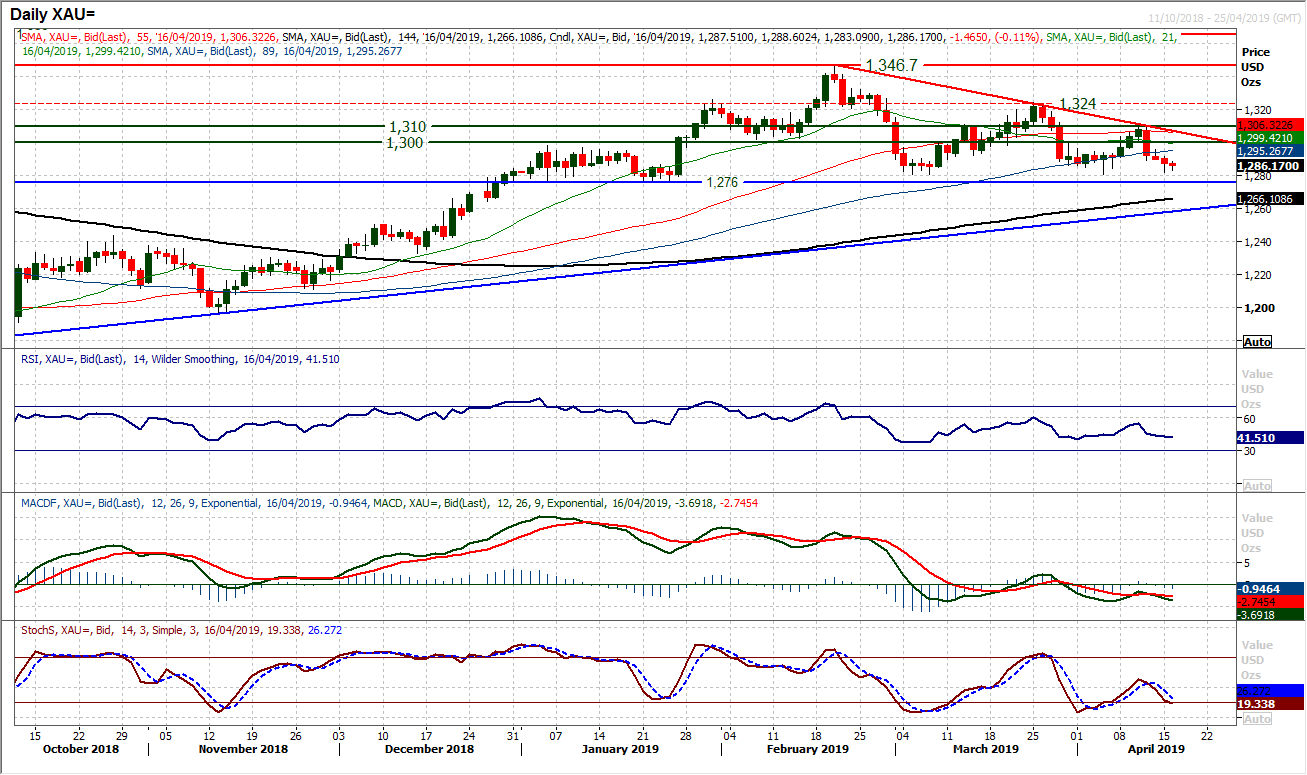

Gold

An intraday downside break on Silver is a red light warning for the gold bulls. The support between $1276/$1280 has been a crucial medium term support for almost four months. However, selling momentum has been growing as the latest rebound failed at $1310. With a series of momentum sell signals the pressure is mounting. Renewed bear crosses on both MACD and Stochastics lines under their neutral points add to the negative momentum. A large head and shoulders top pattern would complete on a close below $1276 and be a big bearish medium term development. Essentially it would imply $70 of further correction to $1206. It would also put the long term recovery under real strain (an eight month uptrend rises at $1258 today). The bulls need to quickly regroup and pull the market back above $1300 to improve the outlook. A two month downtrend falls at $1307 today. The hourly chart shows overhead supply resistance between $1289/$1295. Initial support at $1280.

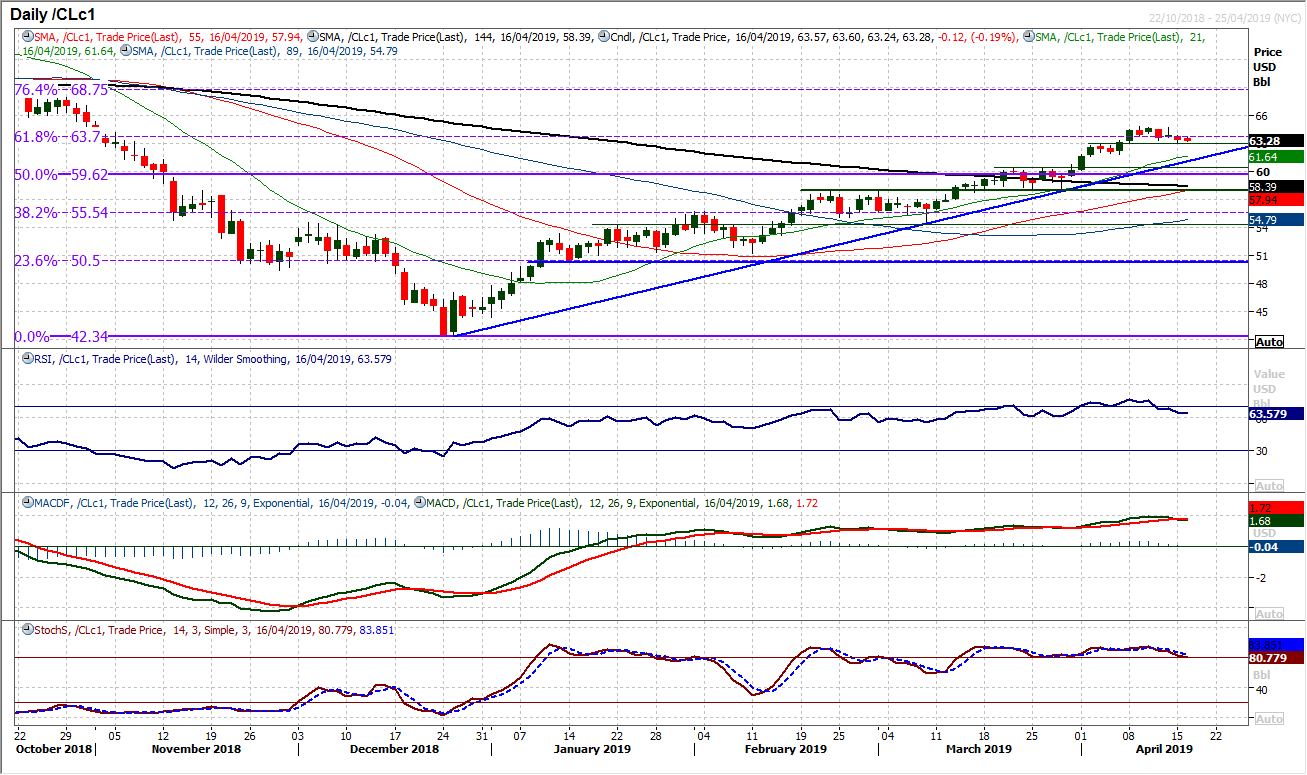

WTI Oil

The latest drift back into support has now been going for the past week. Having hit a five month high at $67.80 mid last week, WTI has been slipping quietly back towards the latest breakout at $63.00. The move has unwound the RSI back from the mid-70s into the mid-60s. The strength of momentum shows the RSI continually finding buyers between 50/60 in recent months. Whilst the support at $61.80 remains intact, this looks to be just another drift to be bought into. The rising 21 day moving average has continually been a basis of support in recent months and comes in around $61.65 today. Support of a near four month uptrend also comes in at $60.40. Whilst there is further room for the corrective slip, this is still likely to be a near term move that is supported for the next leg higher.

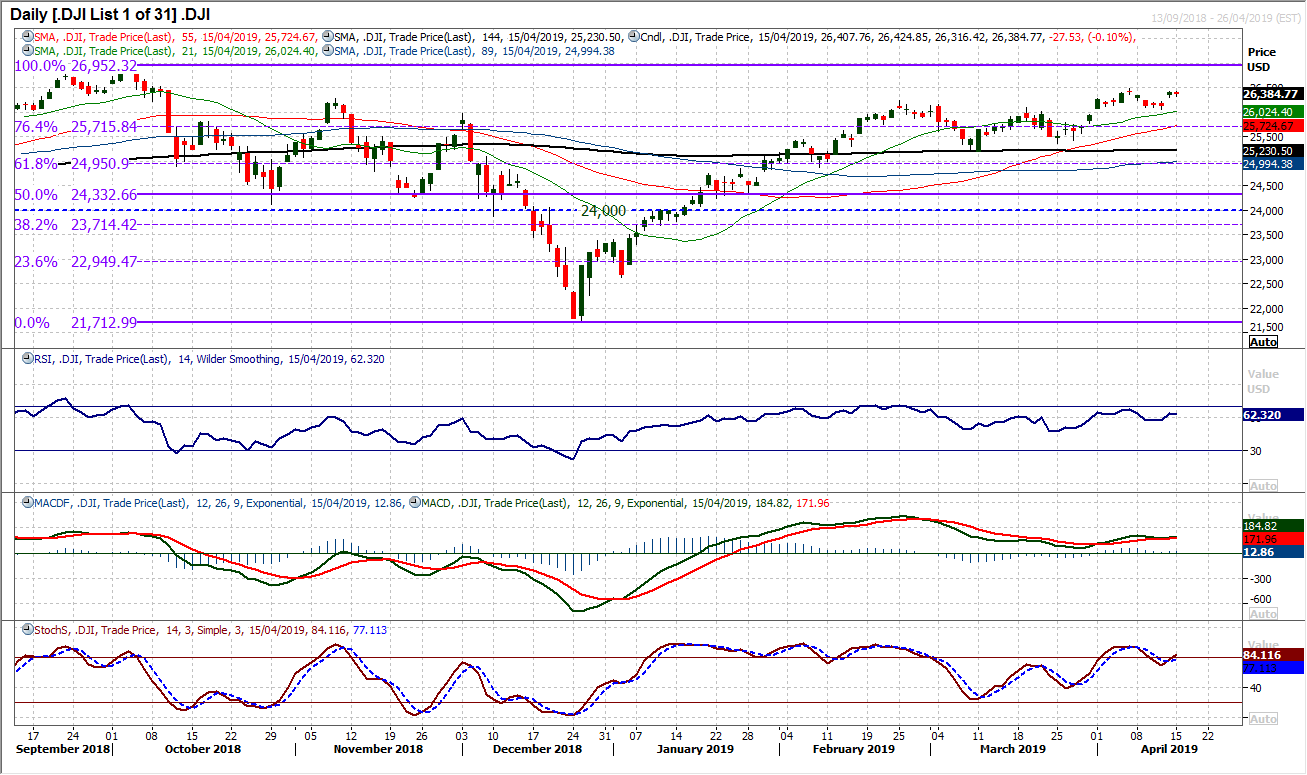

Dow Jones Industrial Average

Into US earnings season this has a big influence on the direction of Wall Street markets. The run higher on the Dow subsequently stalled yesterday on rather drab reports from Citi and Goldman Sachs. However, the technical outlook continues to look towards an upside break above the April high of 26,488. A return to the high of 26,952 should also not be ruled out in due course. This comes with positive configuration across momentum indicators. The RSI is into the 60s and Stochastics ticking higher again towards the 80s. Perhaps the MACD lines which are a touch lackluster, could be stronger, but essentially corrections remain a chance to buy. Support is at 26,062 from last week’s low.

Author

Richard Perry

Independent Analyst