Brexit and the Pound: Plenty of Downside Left

Back in March, I wrote about the coming Brexit apocalypse for the pound. I said that there were only three likely results for the pound: bad, worse and terrible. “Terrible,” I said “would be crashing out with no agreement at all.”

So where are we now? It seems to me that “terrible” is not just the most likely scenario, it’s not even the worst possible scenario anymore. In my view, an interim government under Labour with Jeremy Corbyn at its helm represents the worst of all possible worlds for GBP: economic dogmatism that will frighten markets coupled with a pro-Leave bias. Which is not to say that I’m any great fan of the incumbent Conservative government either, except insofar as I’m an American citizen and so grateful for any group of politicians that make our Congress seem reasonable and well-functioning by comparison.

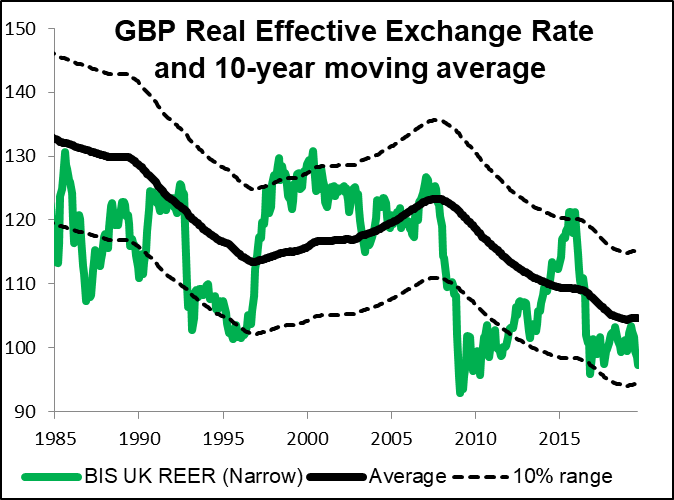

But let’s put politics aside and look at the economics. Where is the pound nowadays? The simplest way to value the currency is relative to its past value. For this exercise, we use the real effective exchange rate (REER): the value of the currency against the country’s major trading partners, adjusted for inflation. It’s important because trade imbalances are one of the major factors moving currencies over the longer term.

On this metric, back in March, the pound was just 1.2% undervalued against a basket of currencies of the major economies. Currently, it’s about 7.1% undervalued – still not at the 10% undervalued line that has sometimes (but not always) been a barrier in the past. That means even under normal circumstances, it can fall further. And as you can see, in extraordinary circumstances, such as the Global Financial Crisis in 2008/09, that 10% line is no barrier to GBP depreciation. (Last time I used the IMF’s calculation for the GBP REER, but this time I’m using the BIS’, which is updated more frequently.)

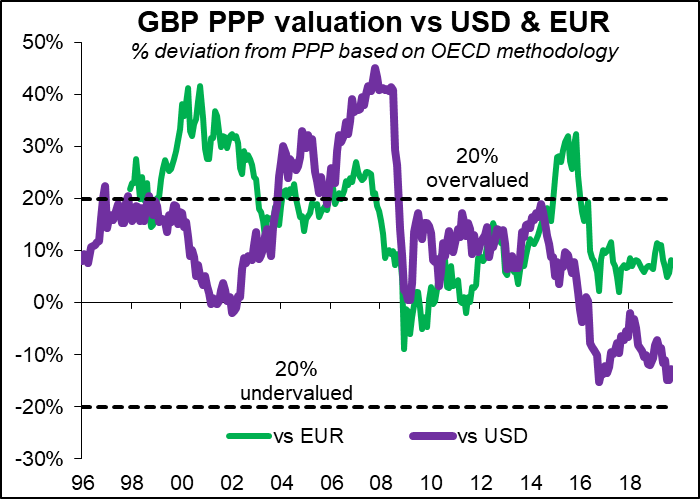

The more theoretical way of valuing the pound would be with purchasing power parity. That’s as close a metric as we can get in forex analysis to seeing whether a currency is “fairly valued.” Looked at this way, the pound is still relatively expensive against the euro. According to the OECD’s way of calculating PPP – taking a large basket of goods and services and pricing them in different countries -- the pound is 12.7% undervalued vs USD but still 8.1% overvalued vs EUR! This compares with -8.7% and +11.%, respectively, back in March. And considering that the EU is Britain’s largest trading partner (51.6% of total trade) vs 10.6% to the US and 7.6% to China, the two dominant USD trading partners, it’s clear that the pound’s value relative to EUR is the more important of the two prices. It’s got far to go before it hits up against the 20% line that has in the past provided some resistance (as that’s about the level where the currency starts to impact trade flows).

For GBP/USD to hit the -20% line, the pair would have to be at 1.14. For EUR/GBP to hit that level, the pair would have to be 1.20 (implying GBP/USD at 1.08, assuming EUR/USD stays at its current rate). It looks like the long-awaited “pound parity party” is coming up!

This analysis so far builds on what I said last time: although the pound has fallen considerably since before the Brexit vote, that doesn’t mean it’s cheap yet. It can still fall further.

Back in March, I made the balance of payments argument for why sterling should fall further: that after Brexit, the current account deficit is likely to widen further (because exports will be held up) while the financial account surplus is likely to diminish (as both direct investment and portfolio investment turns into an outflow). That argument still holds. Now I’d like to focus on the monetary reasons why the pound is likely to weaken, namely: the market isn’t at all discounting the Bank of England’s likely reaction to Brexit.

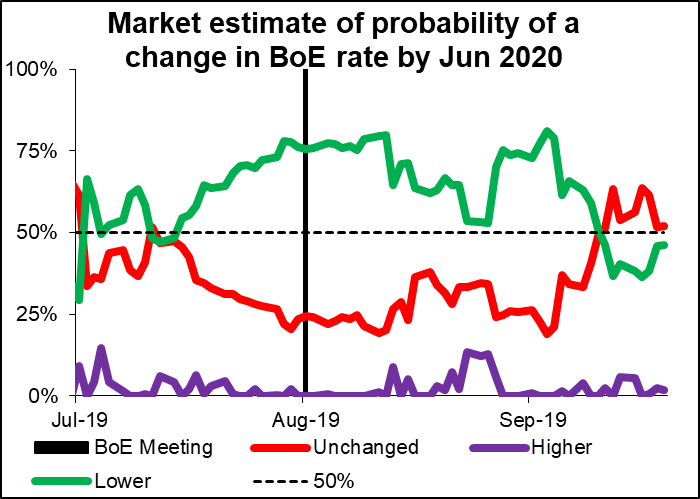

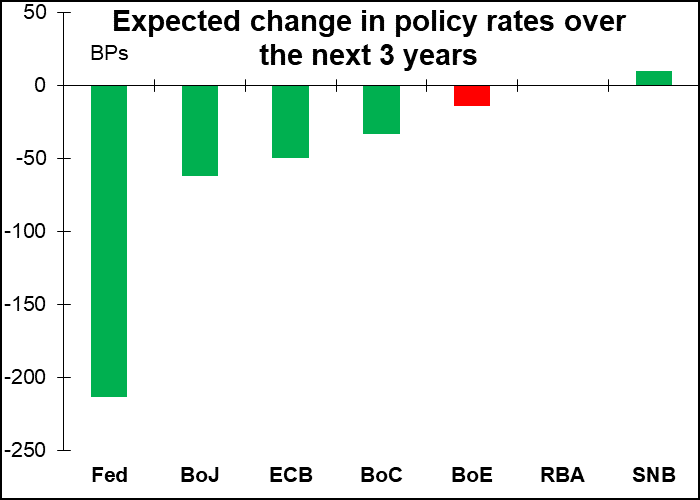

Basically, the market sees little chance of any significant Bank of England easing – it’s only pricing in a 50% chance of even one rate cut by June of next year.

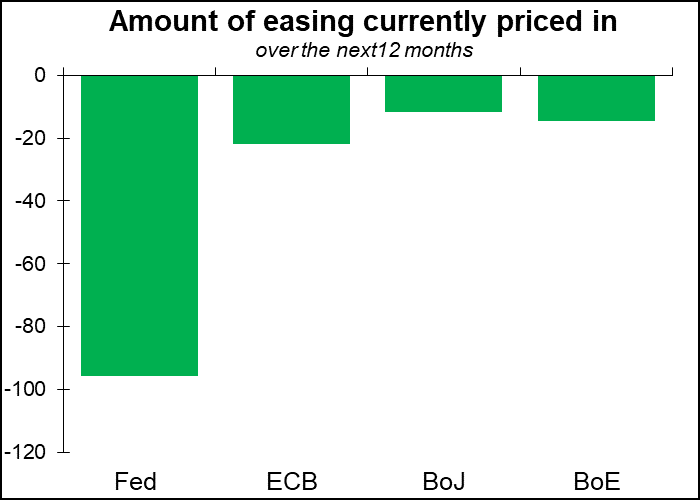

The market is implying that over the next year, the BoE may cut rates about as much as the ECB – which already has negative rates – and the Bank of Japan – which hasn’t had significant inflation for about two decades.

Over the longer term, it’s expected to cut rates very little – even less than the Bank of Japan, somehow.

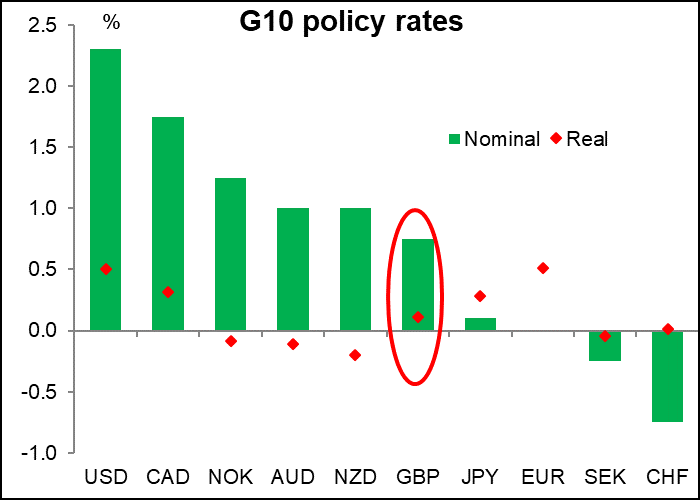

The small number of rate cuts that are priced in probably reflect the fact that Bank’s policy rate may be positive, but it still isn’t that high in international terms, neither in nominal nor in real terms, even if it is positive.

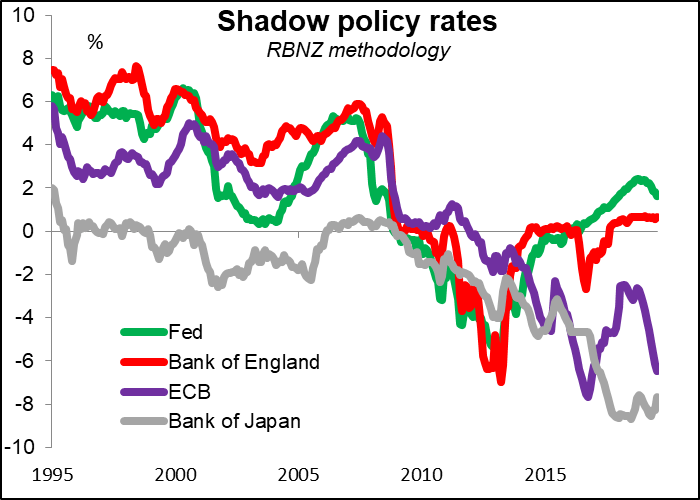

However, that comparison fails to take into account the impact of the quantitative easing that other central banks undertook. If we adjust for that, we get what are called shadow policy rates.* These show much better just how tight UK monetary policy is relative to the Eurozone or Japan. It’s nearly the same as in the US, where rates had been lifted from almost the same starting point (effectively) nine times before coming down once (the graph only has month-end data and so doesn’t encompass the Fed’s rate cut this week).

In other words, UK monetary policy is still very tight and yet the market is only pricing in the minimum amount of loosening – about as much as central banks that are already well into negative territory for their policy rates. Is this reasonable? It was back before Brexit, when the Bank of England was in the process of “normalizing” interest rates (on the assumption that “normal” was still the way the world worked before September 2008). And that’s basically what the Monetary Policy Committee (MPC) would have us believe. Following Thursday’s meeting, they repeated their usual comments that if it looks like Brexit will go smoothly, they would raise rates “at a gradual pace and to a limited extent.” Even in the case of a no-deal Brexit, the Bank’s response “would not be automatic and could be in either direction.”

Does anyone believe that? Will the one rate cut that’s not even fully priced in be enough to fight the biggest shock to the UK economy since James Callaghan had to borrow money from the IMF in 1976? Of supermarket shelves empty while lambs that were destined for foreign markets are being slaughtered by the thousands? Central bankers may be dedicated to fighting inflation but they also have to be aware of what the population is facing. Besides, even the BoE itself said Thursday that if there was “entrenched uncertainty” over Brexit, “domestically generated inflationary pressure would be reduced.” That gives no reason to expect a hike in rates any time soon – and a lot of reasons to expect the Bank of England to join the world’s rate-cutting cycle.

I think the market is being too, too sanguine about the likely impact of Brexit on the UK economy and the Bank of England’s likely response. The rational course in case of a downturn would be for the Bank to cut rates and let sterling act as a “shock absorber” in troubled times. I still see plenty of downside to the pound as the prospect of below-consensus interest rates add another reason to sell on top of impending economic and political chaos.

Author

Marshall Gittler

Trading Analysis