Bond market update: The bond market is whispering something beyond inflation

- The move in yields is not just macro repricing, it reflects real world reserve flows that the market is now being forced to absorb.

- What looked like a rates story is in part a dollar funding squeeze, with Treasuries and gold both used as sources of liquidity.

- Gold’s weakness reads more like forced selling than a shift in conviction, leaving the broader macro case intact once flows stabilize.

Whispering something beyond inflation

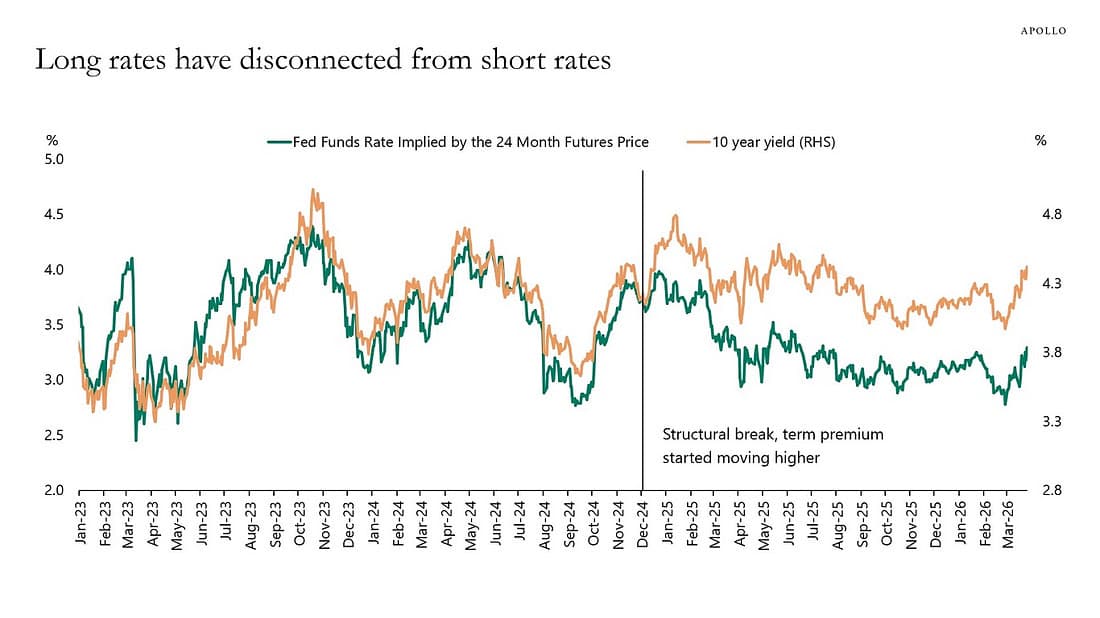

I had been struggling to reconcile why US 10-year yields were trading so far above where the macro backdrop seemed to justify. If you map the short-end spike inflation drift against the 5-year breakeven, the 10-year should arguably have been gravitating closer to 3.9%, not pressing up into the 4.4% area. That gap never looked trivial to me. It looked like a market demanding compensation for something deeper, something it did not fully trust.

Now we may have a more concrete explanation.

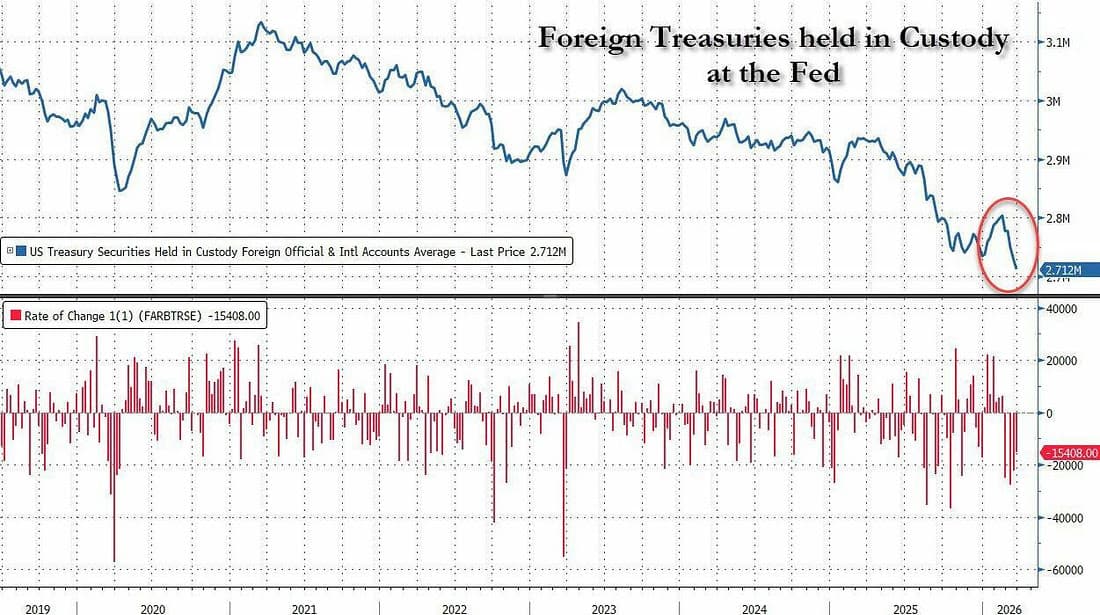

According to custody holding data from the New York Fed, foreign monetary authorities sold Treasuries for five consecutive weeks starting just before the Iran war began in late February. Over that stretch, official holdings held at the Fed fell by more than $90 billion, with the heaviest selling concentrated in the last three weeks. That is not background noise. That is reserve management under pressure, and it helps explain why long-end yields have remained so sticky even as growth signals have softened.

This matters for FX and gold because I had also argued that the tight correlation among gold, FX, and equities had begun to loosen. Once that old market lockstep began to ease, it opened the door for gold buying to re-emerge on its own terms. But before that could happen, the market needed to understand why yields had lurched higher in the first place. If part of that move was not about inflation expectations or Fed repricing, but about forced reserve liquidation, then the gold shakeout starts to look less like the end of the story and more like a buying opportunity aka the debasement trade

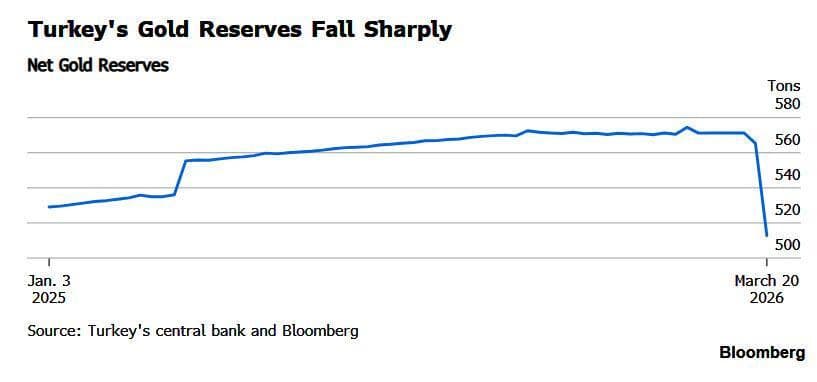

There is a growing body of evidence pointing in that direction. The Financial Times reported that some central banks have been intervening in FX markets to support their own currencies, a process that often requires selling dollar assets. Turkey is a clear example. Since the war began, Turkey’s central bank reportedly sold or swapped around 58 tonnes of gold, worth more than $8 billion, while also selling roughly $22 billion of foreign government securities, mostly Treasuries, from its reserves. That is not portfolio fine-tuning. That is a liquidity response.

The same pressure may also be surfacing elsewhere. Data out of Thailand and India, as cited in the reporting, suggest reserve drawdowns since the start of the conflict, although it remains unclear whether those reductions reflect Treasury sales, dollar deposit use, or a mix of both. Either way, the signal is the same. Countries facing higher oil import costs and currency pressure may be dipping into reserves to steady the ship.

That helps explain why the Treasury market has felt as if it has been trading with an extra premium bolted onto it. Meghan Swiber at Bank of America put it plainly: the foreign official sector is selling Treasuries. Stephen Jones at Aegon Asset Management framed it another way, saying reserve managers may be “stocking the war chest” by cashing out rainy day assets. Both interpretations point to the same conclusion. This was not just a clean rates repricing driven by inflation fears. It was also a flow story.

Apollo

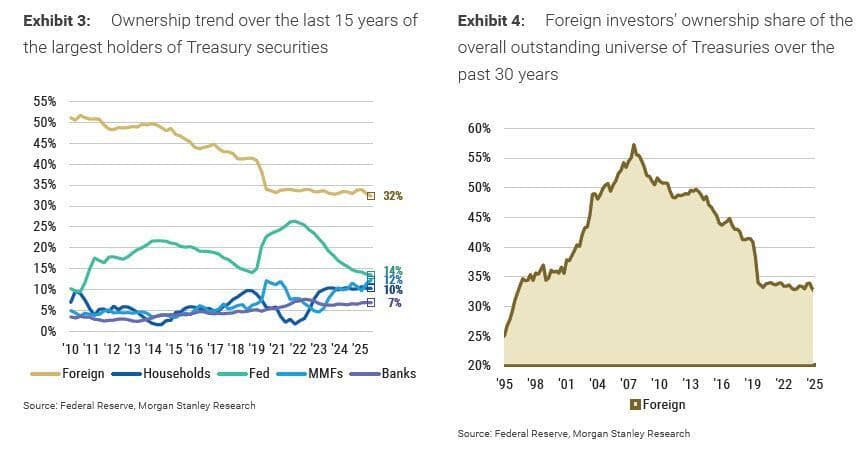

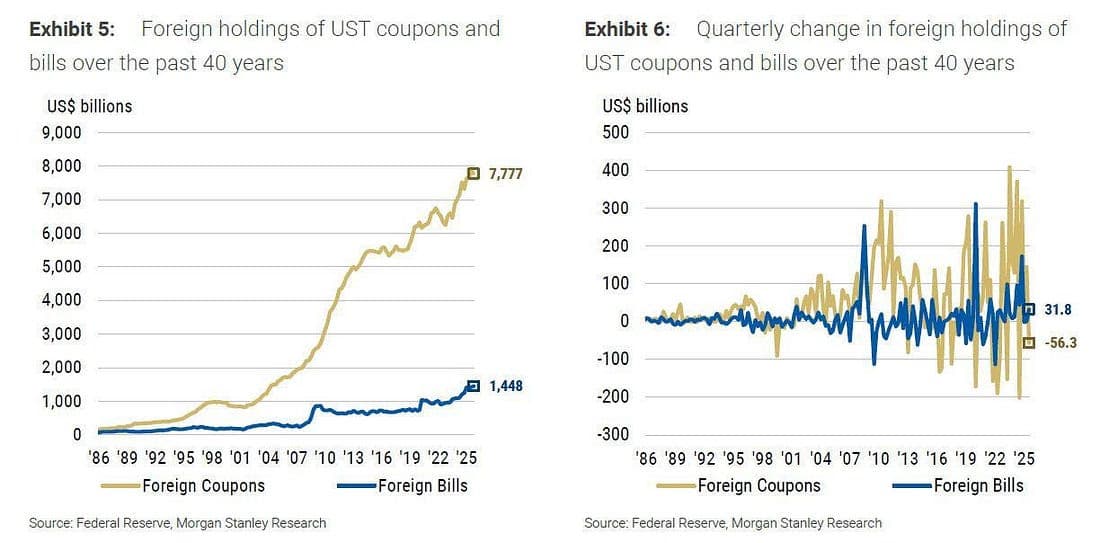

There is also a longer term structural angle that matters. A recent Morgan Stanley rates note showed that foreign ownership of the outstanding Treasury universe has fallen to around 32.4%, the lowest share since 1997. That is a major regime shift. Foreign investors are still large holders in absolute terms, especially in bills and coupons, but their share of the market has been steadily declining for years. In other words, the Treasury market has become more dependent on private sector buyers just as geopolitical stress is making official reserve managers less reliable.

Morgan Stanley’s work is especially useful because it shows this is not a simple “sell America” story. In 4Q25, foreign investors reduced coupon holdings by $56.3 billion, while still adding $31.8 billion in bills. That suggests the move is more about duration preference, liquidity, and policy expectations than a wholesale abandonment of US assets. But once war stress hit, the shorter term scramble for dollars appears to have accelerated the selling pressure, especially in the long end.

For gold, this distinction is critical. Gold did not come under pressure because its long term case disappeared. It came under pressure because in times of stress, the market sells what it can, not always what it wants to. If official players were scrambling for dollar liquidity to defend currencies, fund energy imports, or meet wartime financing needs, then bullion and Treasuries both become sources of cash. That kind of liquidation can hit price hard in the short run, but it does not invalidate the bigger macro case.

In fact, once that forced selling wave runs its course, gold can find its footing again, especially if the market circles back to the same problem that was already there before the war intensified: rising fiscal strain, waning foreign sponsorship of the Treasury market, and a term premium that reflects trust erosion as much as inflation risk.

That is why I do not read the latest gold shakeout as the endgame. I read it as a stress fracture in the global funding system, one that briefly overwhelmed the metal before the deeper narrative had had time to reassert itself.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.