BOE Preview: Will Carney drop the hawkish bias? Brexit is not the reason and GBP/USD may fall

- The BOE is set to leave interest rates and its guidance unchanged.

- Rising Brexit uncertainty is paralyzing policymaking.

- If Governor Carney drops the bank's hawkish bias, GBP/USD may drop.

The UK is set to be the first country to leave the EU – and its central bank the only one that wants to raise rates. The Bank of England has been foreseeing a path of gradual rate rises for long months – but has not budged – because of Brexit. The bank is waiting to see when and how the UK leaves the EU before making a move.

And while the BOE is set to leave the interest rate unchanged – it may drop its intentions to raise rates. The chances are rising – and not due to Brexit.

Reasons to worry

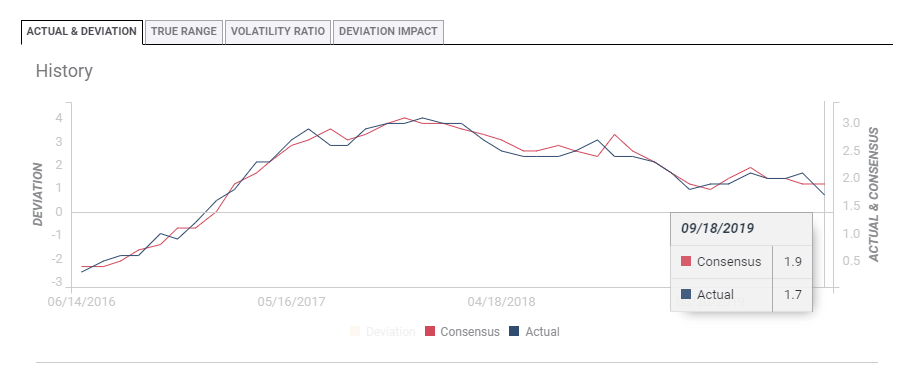

The most recent inflation figures for August have shown a significant deceleration in prices. The annual Consumer Price Index slipped from 2.1% to 1.7% – below expectations. Moreover, prices dropped despite a fall in the exchange rate, which pushes the prices of imported goods higher.

Here is how inflation has developed lately:

Another source of worry is related – yet not entirely – to Brexit. Investment in the UK has been falling for long months. This decline implies lower economic activity in the medium term – that the BOE is focused on. However, investment in other developed countries is falling as well.

And a look at other countries' central banks is also of interest. The BOE makes its announcement one week after the European Central Bank cut rates and announced a new bond-buying scheme. Moreover, the US Federal Reserve and the Bank of Japan will have introduced or signaled more stimulus less than 24 hours ahead of the London-based institution's decision.

Can Mark Carney, Governor of the Bank of England, remain hawkish while his major peers are leaning to more stimulus and acting?

Reasons to be cheerful or at least wait

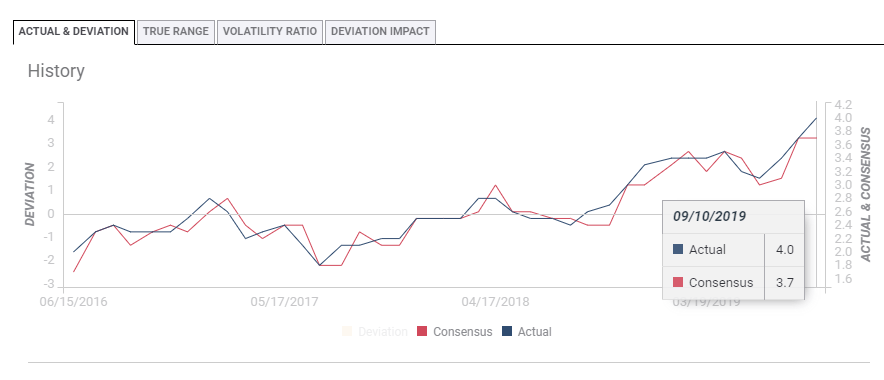

On the other hand, UK wages have been rising at a faster clip – hitting a 4% annual rise when including bonuses. When salaries increase, consumers have more disposable income to spend.

Here is how wage growth has developed of late:

And despite Brexit uncertainty and slowing global growth, UK Gross Domestic Product rose by 0.3% in July – better than expected.

With some signs of economic improvement, there is no need for the BOE to rock the boat and change its guidance. Brexit has also taken a positive twist since the bank's latest decision in August – at least that is what the pound's surge is reflecting. Carney and his colleagues may see the law that prevents a hard Brexit as another reason not to move.

Scenarios for the BOE and GBP/USD

The most likely scenario is that the BOE refrains from making significant changes to its statements – and most importantly, leaves its intentions to raise rates intact. It may acknowledge recent economic data – both the worrying drop in inflation and the encouraging increase in wages. However, they may stop at mentioning the data without indicating any consequences.

In this scenario, GBP/USD may trade choppily, and the reaction may come from the voting pattern. In the past few decisions, all nine members of the Monetary Policy Committee voted to leave rates unchanged. If any of those members dissents and votes for a cut – GBP/USD may temporarily drop. And in the unlikely case of a vote in favor of a hike – sterling may rise.

However, one or two dissenters are unlikely to trigger any meaningful movements – as the focus will remain on Brexit. The chances of dissent are low.

The pound may react adversely – and persist in falling – if the BOE removes its hawkish bias and shifts to a "wait-and-see" mode. That would mean that even if Brexit is postponed for an extended period or canceled altogether, the BOE will not hurry to raise rates – and that the economy has more deep-rooted issues. In the more extreme case of opening the door to cutting rates – GBP/USD may plunge.

Conclusion

The BOE is set to leave its interest rate unchanged at 0.75% on September 19, at 11:00 GMT. In the mo of no change in the bank's intentions to raise rates, GBP/USD is unlikely to change course. If it decides to abandon this stance, GBP/USD has room to fall.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.