BoE: Less pessimistic, but negative rates still under review

At its August policy meeting, the Bank of England has announced that the bank rate and asset purchase target remain unchanged at 0.1% and £745bn, respectively. The vote was unanimous. Growth expectations were less pessimistic than they had been in May and inflation is seen to return to target in two years. Yet negative interest rates remain under review.

Size of the decline cut, yet negative rates still under review

The Bank of England's August Monetary Policy Report has followed the lead of May in providing an indicative path for key variables based on the central bank’s illustrative scenario.

In May, this had seen the UK economy shrinking by 30% in the first six months of the year, but a fairly sharp bounce back meaning a full-year contraction of 14% and a 2021 recovery of 15%. The BoE has revised this scenario to show a 20% decline in 1H20, meaning a 9.5% contraction this year and a 9% recovery in 2021. We are forecasting a 2020 contraction near 10% and a 2021 recovery closer to 6%.

We are forecasting a 2020 contraction near 10% and a 2021 recovery closer to 6%.

On unemployment, the Bank now sees unemployment rising to 7% later in the year (versus 9% previously) as the Chancellor’s job retention scheme is unwound and firms are sadly forced to let employees go. In the new report, what stands out for us is that the 2021 CPI path is revised to 1.75% from just 0.5% seen in the May report. Inflation is seen roughly on target in two years’ time, in theory then reducing the need for more monetary accommodation.

In choosing to keep the Bank Rate and the APP target unchanged at this meeting, the BoE still has the door open for further policy action – probably at the November meeting when a new MPR is released and we will know more about the UK’s future relationship with the EU. Notably, the BoE’s scenario assumes that the UK moves to a comprehensive free trade agreement with the EU by 2021.

We expect the market to stay very invested in the negative rates debate well into 2021.

On negative rates, the MPR dedicates a box to the debate over their effectiveness but concludes that they are still under review. Indeed there is little incentive to rule out negative rates right now and we expect the market to stay very invested in this debate well into 2021.

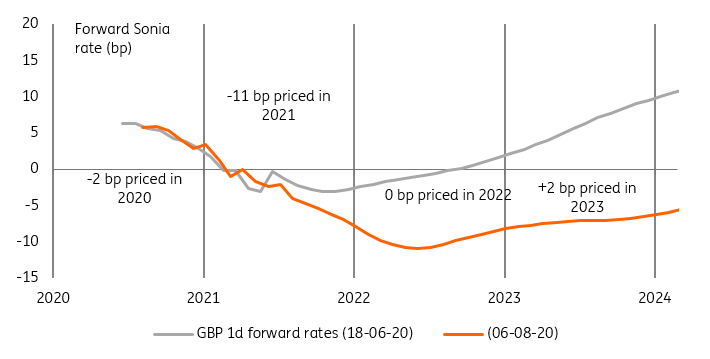

The Sonia curve has made up its mind about negative rates

Source: Bloomberg, ING

Rates: no clear preference for negative rates

Rates markets have already made up their mind about the probability of negative interest rates next year: it is very high, and climbing. The lack of any push back against market pricing today is unlikely to shake that conviction, although the BOE’s review of its effective lower bound (ELB) is still ongoing. From where we stand, this is far from a done deal. The MPR's discussion on negative rates was lukewarm at best. Barring a deterioration of the outlook, we find the risk-reward of positioning for even lower policy rates poor.

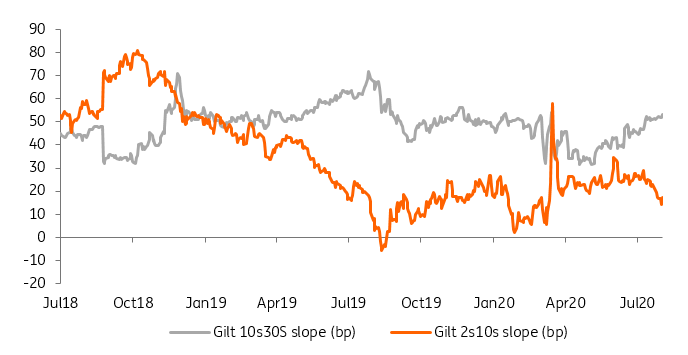

Whilst the GBP swap curve is pricing out further QE

Source: Bloomberg, ING

If the market’s conviction about negative interest rates seems dramatic, the flattening of gilts 2s10s has been no less noticeable. The Gilt rally is by no mean a move specific to GBP rates markets. 2s10s have flattened in USD and EUR as well. The difference lies instead at longer tenors.

The simultaneous re-steepening of GBP 10s30s is a symptom of the BOE’s lower perceived appetite to further expand its balance sheet, as its June QE extension implies a degree of tapering. The move was logical and in line with our expectations, but the BOE’s strategy of keeping as much optionality about its future move as possible means the case for the further divergence of 2s10s and 10s30s is weaker going forward.

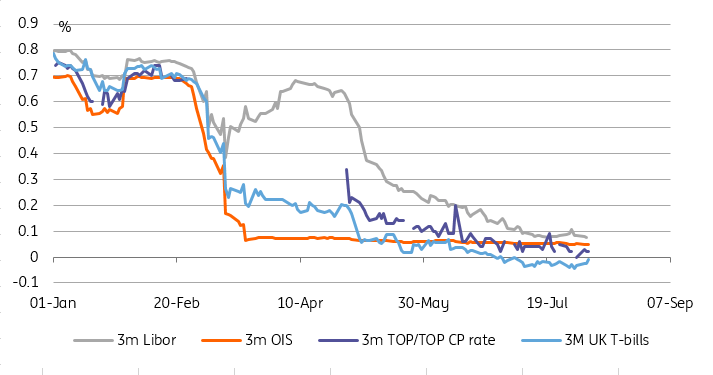

Money markets have fully recovered

Source: Bloomberg, ING

To be sure, the case for further balance sheet expansion is not helped by the sharp improvement in GBP money market conditions. If you thought the Sonia curve is pricing ridiculously low interest rates, wait until you see commercial paper (CP) indices. Admittedly, we have no information about the underlying volumes at these levels, but the TOP/TOP 90d CP index is reporting rates fast converging with 0%, when the corresponding Sonia swap rate is still 0.08%. There has been a similar adjustment lower in GBP Libor.

Temporary respite for GBP

GBP has rallied on a slightly less pessimistic assessment from the BoE. GBP has remained one of the high conviction underweight positioning amongst the speculative community and today’s update from the BoE has no doubt triggered a little more short-covering. Cable may have some more upside on the back of a powerful dollar bear-trend – especially if the 1.3200 level breaks.

Yet EUR/GBP should stay supported under 0.90 and we continue to favour 0.92 levels into the Autumn.

Read the original article: BoE: Less pessimistic, but negative rates still under review

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.