Banks posturing for one more round of deflation

“Lower interest rates are deflationary until they become inflationary…”

The financial media has done a good job of pushing the Fed’s inflation at all costs narrative, more accurately dubbed a “reflation.” Nevertheless, investors would be well-served to realize that lower interest rates and the Fed’s policies to bolster liquidity (QE and special lending facilities) are not inflationary until they stimulate bank lending and money velocity. My personal belief is that inflation will indeed rise in the not so distant future - and perhaps even faster than central planners’ can handle. However, several indications suggest that large banks (primary dealers) continue betting on one more bout of deflation in the near term, or at the very least a pause of sorts, before lasting inflationary forces take over. The Fed’s emergency programs start running out soon and markets will soon begin absorbing a wave of delayed defaults.

Deflation risks are likely to persist into 2021 until either more government spending is passed through the US congress, or enough of the existing counterparty risk is flushed out of the financial system.

Reason #1: bank credit

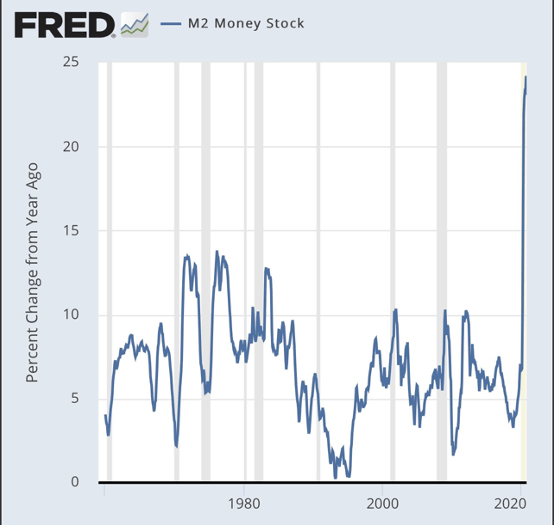

In the debt-based US economic system, more lending is required to achieve rising inflation levels in the official CPI or even sustained inflation in financial asset prices. Those following any financial market news this year recognize there has been a record amount of currency creation via central bank efforts globally. In the US, the M2 money supply has expanded by over 20% in this calendar year alone because the Fed has monetized record government deficits and even ventured into the open markets to purchase debt instruments! Yet even while M2 moves in a parabolic fashion, banks have steadily tightened their lending standards following the initial extension of liquidity back in March.

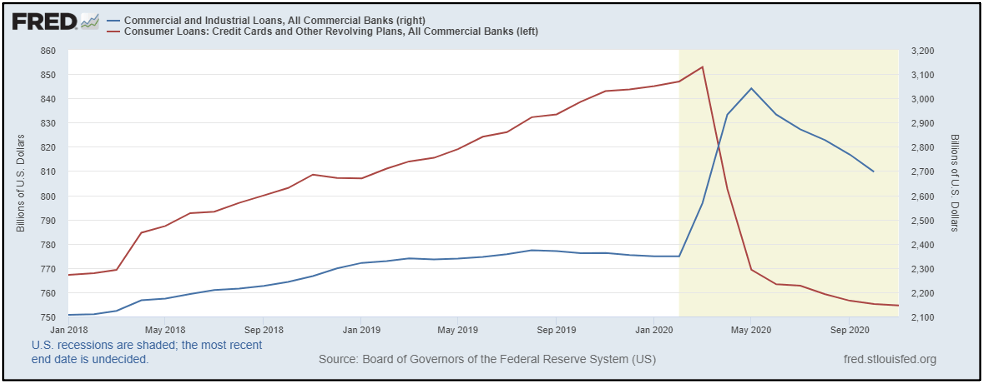

With the M2 money supply growth up by such a staggering amount (chart one below), banks are still not lending at a quick enough pace to create significant inflationary pressures (chart two):

The second chart works contrary to the prevailing narrative that the Fed can produce inflation or boost bank lending to the real economy. Recall that it took until 2014 for commercial and industrial loans to surpass the 2008 peak in the wake of the last financial crisis. The Fed would have preferred this process to unfold much faster, but banks refused to lend at a faster pace. Why should we expect anything different this time around? It seems the masses have forgotten the past decade’s reality of low inflation and low growth against the backdrop of quantitative easing rounds one, two, and three. Remember, banks must lend for the Fed’s narrative to prevail.

Consumer loans are still in a decline along with commercial and industrial loans, as exhibited above, suggesting the Fed may have only “reflated” markets but banks believe the worst financial damages have yet to be absorbed. Primary dealers are not (yet) ready to dance to the Fed’s tune and risk their capital. I’m not suggesting it will take six years for banks to generate real inflation, but they are still behaving as if lending conditions and monetary policy remain too tight given the counterparty risks still out there. Despite the unprecedented fiscal and monetary policy actions we’ve seen this year, more is needed if policymakers expect banks to look past the huge debt burden weighing on the economy and balance sheets.

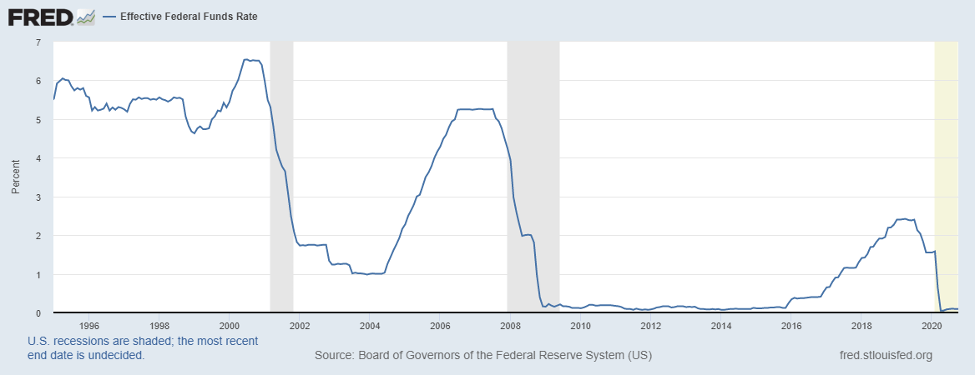

There is another piece to this puzzle that many have seemingly forgotten. This could explain why banks remain so defensive. Remember (see chart below), the Fed Funds Rate had over 600 basis points of room to be cut before hitting the zero bound in the year 2000 and more than 500 basis points in 2008. Before the 2020 crisis even began, the Fed already had cut rates below 2%. This left little room (under 200 bps) for the Fed to cut rates and ease financial conditions.

In potentially the most severe economic crisis in history a 200 basis point decline in the Fed Funds Rate is not going to be stimulative. It has only served to marginally soften capital destruction. The only way the Fed could have matched the “stimulative” effects of their rate cuts in 2000 or 2008 would have been to lower the Fed Funds Rate deeply negative (-2% to -3%). Instead, the Fed elected to abide by the zero bound and expand its other tools massively to boost money supply growth and lending.

The Fed’s hail mary approach has involved financing a record volume of US Treasury issuance this year and the purchases of assets in the open market. This combination explains why the Fed’s balance sheet has expanded much faster than any period in history. It’s very important to also note that the US money supply expands at the fastest rate when the Fed monetizes new Treasury bond issuance. Without US government deficits and fresh Treasury bond issuance, the Fed is limited to the monetization of existing securities through their emergency liquidity facilities, which means less money supply expansion.

Based on the charts examined thus far, it seems that the big banks understand a dilemma now presents itself. With a “lame-duck” session underway in congress, it’s unlikely there will be new fiscal spending from the Treasury until the new year. Bank balance sheets will be hit with a record wave of credit losses in the meantime as various emergency programs that were set up by the Treasury earlier this year expire. These programs surely kept many insolvent entities alive and will end after the holiday season. It seems the soonest the Fed and banking system can hope for a meaningful dose of new fiscal spending will be sometime after Biden takes office in late January of 2021.

Without new Treasury issuance for at least a few more months, the only variables capable of stimulating credit growth from banks is either even lower interest rates, more Fed liquidity via open market asset purchases, or simply more creditworthy borrowers. The problem is that firstly, creditworthy borrowers don’t just grow on trees, the Fed has already said it won’t implement negative rates, so those are off the table. The only backstop remaining seems to be whatever firepower is left in the Fed’s special facilities. Treasury Secretary Mnuchin may have recently extinguished the last remaining glimmers of hope with is the announcement that the Treasury will be pulling back its emergency funding for the Fed’s emergency programs as of December 31st.

This is not a rosy picture if you are betting on inflation in the short-term. Until we see congress act, the risk of another deflationary episode remains significant.

Point #2: Speculators are on the other side of the banks

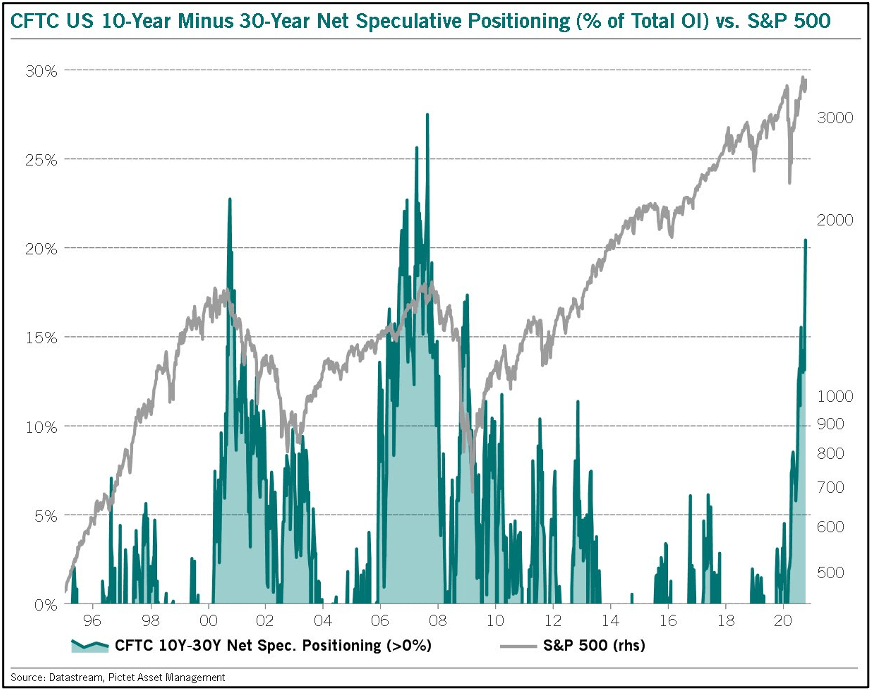

Why would banks be willing to position themselves on the other side of this record speculative bet on rising inflation? Easy - they think the hedge funds and other speculators are wrong for the time being.

The chart above can be expressed quite simply as a near-record surge in the number of speculative bets being placed on rising inflation, with hedge funds accounting for much of this betting. This is also mirrored by the recent overwhelmingly bullish hedge fund positioning in commodities, according to official CFTC data. A lot of steam may still need to be released out of inflation trades and equity markets as banks begin absorbing credit losses in early 2021. At the very least, volatility is to be expected. The recent >10% correction in the price of gold may be an early sign of my theory being priced in. This may also imply that equity prices need to correct once more from their current record highs. This would flush out lots of weak hands (retail traders) and excite those who seek to get into a lasting inflation trade at more attractive valuations.

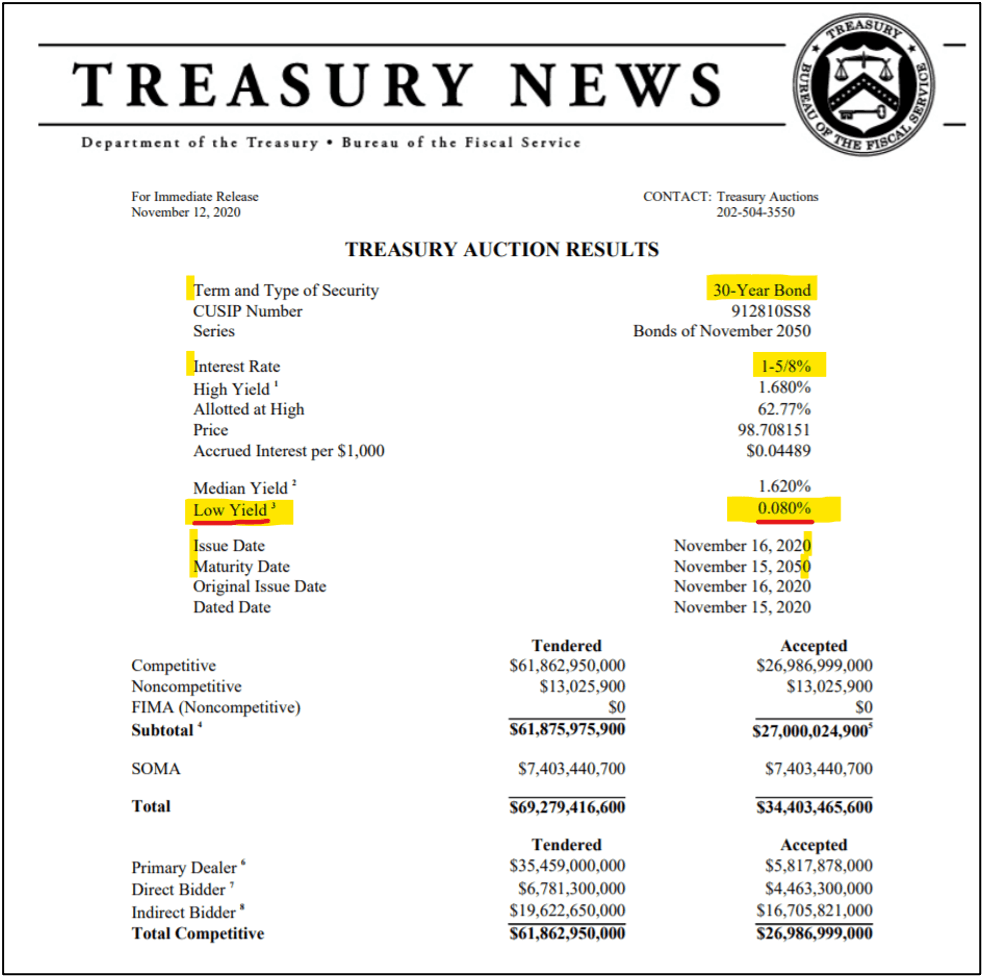

The following data from a recent 30 year US Treasury bond auction is another sign that banks think we need to experience one more round of deflationary conditions to rebalance things before a genuine inflation storm sets in. I have marked up the document to highlight key points.

Yes, a Dealer really bid for a 30-year bond at essentially zero, betting against the mass of speculators who believe yields are going immediately upwards. This may be an extreme example, but it helps to show how some large dealers evidently believe even lower interest rates are needed before significant inflation is sustainable.

With the massive wave of delayed defaults hitting bank balance sheets after the Christmas holidays, it’s worth being extremely careful! It would be unwise to put absolute faith in central planners’ ability to keep equity prices levitated. Investors should recall that insolvency hazards from March remain at large, the only difference is today even more extreme systemic leverage has been added to the mix. Banks still need to alleviate balance sheet pressures caused by lockdowns, risky loans, and insolvent counterparties. Many counterparties are likely ready to file for chapter 7 or 11 bankruptcy after being kept alive by expiring government programs.

Maybe once this bankruptcy wave ends it will finally be time for the inflation monster to rear its head, with the large banks even getting on board to support the Fed’s narrative at last.

Lastly, recall what sparked the “reflation recovery” in March:

In March, the Fed made their emergency rate cut announcement and the markets kept selling off. It was not until the government came in with a promise to add a huge fiscal backstop that things turned around for good.

Think about it: banks understand that the Federal Reserve takes collateral out of the financial system through their QE and adds only bank reserves. The Fed needs fresh securities to monetize if they hope to meaningfully expand the money supply without starving the system of collateral (mainly Treasuries)! Jeff Snider is one monetary expert economist who covers this in extreme detail, and I highly recommend his work to anyone interested in the inner workings of the monetary system.

It should now make perfect sense why Jerome Powell and other Fed members have been appearing on cable news to call for more fiscal spending. This is a warning, make no mistake about it. Fed officials rarely make such comments publicly. They know there is a need in the banking sector for more Treasury issuance; they need new securities to monetize before liquidity runs dry. Unfortunately for the Fed, November’s election results now make it unlikely for Washington officials to pass large spending bills, even once Biden takes office. If Republicans win the Georgia runoffs, their Senate majority may put a lid on the Democrat’s spending.

Conclusions:

Right now we are seeing markets in a euphoric state, lacking a trustworthy fiscal backstop amidst a “lame duck” congressional session. The Fed is sounding the alarm, but they have been met by deaf ears in Washington.

As mentioned at the outset: lower interest rates are at first a signal of deflationary conditions in the banking sector, until the point at which banks believe it to be a sound business decision to boost lending. Only at that point will lower rates help accelerate credit expansion and real inflation. Investors need to understand a Fed narrative alone is not enough to fool the big banks into lending. Massive banking institutions aren’t novices conditioned to “buy the dip” - they react to real fiscal and monetary policy moves. They understand the difference between narrative and arithmetic. Right now, arithmetic suggests that deflation protection is running thin as we head into the holiday season. The inflation crowd likely has it right in the long term, but might be early to the party.

Hold onto your hats, because this crisis is still far from over. Financial assets broadly, especially high yielding corporate debt and the more leveraged companies in the large indices are still at risk of a liquidation event. Balance sheets remain over-leveraged across the board, and investors would be smart to consider limiting exposure to the coming defaults and heightened counterparty risks by owning highly liquid securities and also tangible assets that will survive no matter what. Raising cash is never a bad idea either, at least until some of the economic uncertainty is behind us with regards to the new administration’s Treasury policy and more.

Author

Miles Ruttan

Bytown Capital

Miles' focus at the firm is to oversee our macro analysis, with the emphasis being placed on global credit and liquidity flows.