Bank of Japan holds policy rate steady and plans slower tapering

The Bank of Japan kept its policy rate at 0.5%, reducing Japanese Government Bond purchases from 400bn yen to 200bn yen starting in April 2026. Governor Kazuo Ueda is cautious about US tariffs and their negative impact on investment and wages, while expressing no immediate concerns about inflation. We no longer expect a hike in the third quarter.

The BoJ is trying to avoid volatility in JGB markets

The BoJ's decision to keep the policy rate unchanged while reducing JGB purchases reflects a careful approach to managing market expectations.

The BoJ highlighted that slowing quantitative tightening (QT) aims to enhance JGB market functioning. The central bank also emphasised that it will maintain flexibility, adapting to any sudden market changes. Today's decision appears to be influenced by recent volatility in JGB markets. Governor Ueda noted that a quick tapering may raise market volatility, resulting in a negative impact on the economy, and the BoJ seems like it is trying to avoid disrupting the market reaction.

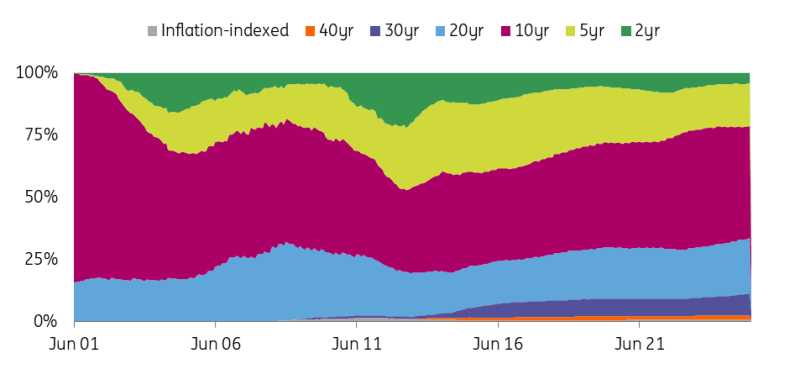

Since the BoJ's JGB holdings are concentrated in long-term maturities, slower QT is expected to have a greater impact on long-term market rates and less on the policy rate. Governor Ueda has also previously stated that balance sheet reduction should be viewed separately from the policy rate decision. Thus, slower QT doesn't necessarily mean slowing rate hikes.

The BoJ's JGB holding by maturity – QT has a bigger impact on the long-end JGBs

Source: CEIC

The BoJ will maintain a wait-and-see stance for longer than expected

However, the Governor's remarks at the press conference suggested a reinforcement of the dovish stance. He stated that inflation expectations have not yet anchored at 2% and expressed concerns about tariffs potentially affecting future wages. He indicated that tariffs could impact winter bonuses and next year's spring wage negotiations. This has prompted us to further delay our calls on the timing of the next rate hike. We have argued before that the BoJ could hike as early as July as underlying inflation is rising, but we now see a clear dovish leaning from the BoJ and no rate hike is expected in the third quarter of this year.

Governor Ueda attributed the majority of downside risks to US trade policy. Therefore, we think that unless Japan and the US reach an agreement on tariffs, the BoJ is likely to maintain its current rate stance. Unlike early expectations that Japan might make a deal with the US, negotiations have dragged on longer than expected. Thus, the BoJ's action may be delayed to early 2026.

Although the current assessment on inflation is missing the BoJ's expectations, the central bank expects the price trend to be in line with its goal in the outlook in 2H25; thus, if underlying inflationary pressures continue to build in the coming months, the BoJ may hike in the fourth quarter of this year.

We see inflationary pressures are broadening. The earlier price gains of rice and food have been passed on to services prices and other manufactured prices. We also see a gradual pick-up in rents over the next few months. So, if core inflation continues to stay above 2% for the coming months, a rate hike by the BoJ is still possible in 4Q25.

Read the original analysis: Bank of Japan holds policy rate steady and plans slower tapering

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.