Bank of England to hold rates despite better inflation news

The Bank looks likely to keep rates on hold on 6 November, despite better inflation and wage news. The committee is deeply divided, and we don't expect clear signals on the Bank's next steps. But assuming the Autumn Budget goes as expected, a December rate cut now looks more likely than not.

November is back in play

Suddenly, a Bank of England rate cut on 6 November doesn’t look like such a remote possibility. Having virtually written it off, markets are now pricing a 25% chance of a 25bp cut.

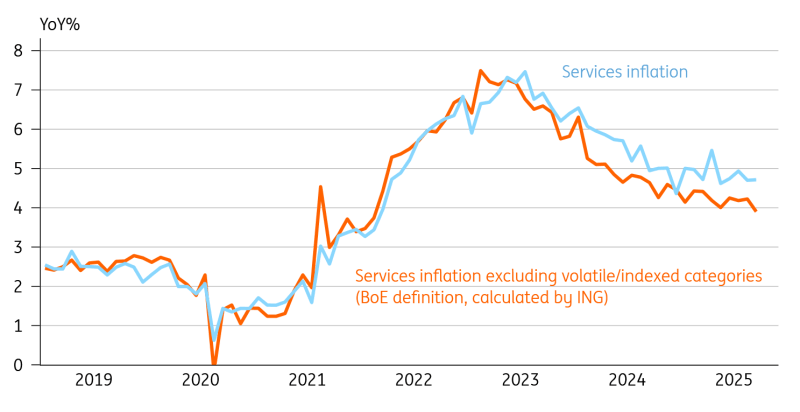

Inflation has almost certainly peaked. Food inflation – a critical concern at the BoE this summer – fell back in September and is now running half a percentage point below official forecasts. Services inflation looks better too; the Bank’s favoured measure of “core services” has slipped below 4%, we estimate. Private-sector wage growth, another key metric for the Bank, has also slowed markedly and is set to end the year below 4%, down from 6% at the turn of the year.

This all comes at a time when the Bank is visibly divided on how problematic inflation really is. The hawks say that 4% inflation risks becoming entrenched. They worry that rising food prices will fuel inflation expectations, risking a repeat of the 2022 energy spike, which morphed into a much more persistent bout of price pressure.

The doves argue that times have changed: the jobs market has cooled a lot from three years ago. Workers lack the bargaining power – and firms the pricing power – to respond to higher inflation and protect their disposable incomes/margins the way they could after the pandemic.

"Core services" inflation is falling back

Bank of England metric calculated by ING, based on methodology contained within the Monetary Policy Report

Source: Macrobond, ING

That’s our view too – inflation should look visibly better into next year. Yet this debate won’t be resolved by one month’s worth of data. The notion of “inflation persistence” is a slow-moving story. These are fundamental differences of opinion on the mechanics of inflation in the UK post-pandemic. More data is needed.

So, having turned more cautious on rate cuts this summer, we don’t think the Bank’s thinking will have shifted as significantly as market pricing has over the past month. That’s why we recently removed a November rate cut from our forecasts – and we’ve not changed our mind since. A hold looks most likely this time.

Beyond the decision itself, three things matter for markets:

Vote split

The two well-known doves – Swati Dhingra and Alan Taylor – are likely to vote for a cut, having done so in September. One or both of them could vote for an aggressive 50bp move. Dave Ramsden is likely to vote for a cut too, having infrequently dissented in favour of further rate cuts over recent months. He recently commented that further cuts were needed. Sarah Breeden has also made dovish remarks as of late, but has never yet dissented against a majority decision in her two-year tenure so far.

That sets up a 6-3 or maybe 5-4 vote in favour of keeping rates on hold, with the minority potentially divided between 25bp and 50bp moves. That suggests it could be close. But remember that four committee members are known hawks who are unlikely to back another cut this time, having objected to one in August. That potentially tees up Governor Andrew Bailey as the deciding vote. But given he’s done little to downplay the chances of a pause in November, we suspect he’ll lean towards keeping rates on hold.

It’s tempting to say such a closely run vote sets the bar low for a December cut, if all it takes is one or two voters to shift. Yet in practice, these vote splits aren’t always a reliable guide to policy shifts in the future. The reality is that the committee has been extremely divided all year.

How the committee has voted in recent months

Taylor originally voted for a 50bp cut in August, only to swing behind a 25bp move after a tied vote. L'delli = Claire Lombardelli

Source: Bank of England

Forecasts

The new projections won’t look that different to August. And that’s another reason to suspect that the Bank’s thinking on rate cuts won’t shift enormously just yet.

Yes, the BoE is likely to mark down its near-term inflation profile in response to the latest undershoot. But its wage growth forecasts appear on track. And with the level of market rate expectations similar to what went into the August forecasts, we doubt we’ll see a massive shift in either growth, inflation or unemployment projections this time.

Forward guidance – A December cut?

The big question is whether the Bank will more firmly open the door to another cut in December in either the policy statement or press conference. We don't think it will, for two reasons.

First, unlike the European Central Bank or the Federal Reserve, the Bank is generally much more reticent to guide markets on specific meetings unless it sees pricing as being very out of line with its own thinking. The last time it did this formally was in November 2022, in the aftermath of the “mini budget” crisis, where market rate hike expectations had surged.

Second – and more importantly – the Bank is waiting on the contents of the forthcoming Autumn Budget. While the contours of the budget are becoming clearer, the Bank’s rules mean it can’t act on government policy until it's official.

We suspect the committee will simply reiterate that further easing will be gradual/careful. And that policy is less restrictive than it was.

That said, for the first time, this meeting will see individual policy members include a summary of their views in the minutes, which are released alongside the decision. Whether that will give us more clues on the near-term direction of policy, we’ll have to wait and see.

Sterling could see a temporary bounce

Sterling came under pressure last month as investors swung behind the view that Chancellor Rachel Reeves would credibly tighten fiscal policy and that the BoE would have to take the strain with earlier rate cuts. In fact, the market last month put a full 25bp back into the 2026 BoE easing cycle.

No rate cut this week and the BoE holding onto some of its hawkish summer narrative could prompt some bearish flattening of the GBP rates curve and a temporary currency bounce. EUR/GBP could briefly make it back to the 0.8730/50 area.

However, a tight budget later this month and a December BoE rate cut should see sterling offered again. Currently, we have a 0.88 end-year EUR/GBP target and 0.90 for next year. But that could be revised higher – especially if Reeves were to blow the doors off with an income tax hike.

Read the original analysis: Bank of England to hold rates despite better inflation news

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.