Bank of England preview: Edging towards a 2022 rate hike?

A recent speech by a normally-dovish committee member has sparked a debate on whether the Bank of England will hike rates in 2022, ahead of the Fed. We wouldn't rule this out, though for now we're in the camp looking for the first move in early 2023. Either way, we suspect policymakers will be keen to avoid offering new hints at Thursday's meeting.

The debate on a 2022 vs. 2023 rate hike is heating up

After the excitement surrounding the Fed’s dot plot, Thursday's Bank of England meeting is a good opportunity to ask where the UK will sit in the forthcoming global rate hike cycle.

We know the likes of the Bank of Canada are now talking about a rate hike in 2022, and markets are certainly beginning to think this way in the UK too. There are now roughly two rate hikes priced by mid-2023 – albeit the first of those is a partial one, taking us from 0.1% to 0.25%. We’ve also recently heard from Gertjan Vlieghe, a typically dovish committee member (though one that will shortly leave his post), floating the possibility of a hike later into 2022.

In reality, we don’t think the Bank will say anything particularly new on the timing of rate hikes at this next meeting. Indeed it has recently shied away from saying anything particularly concrete on the timing of a first move. UK policymakers have taken a leaf out of the Fed’s book by signalling it wants ‘significant’ progress on spare capacity before thinking about hiking.

The run of economic data has been encouraging over recent weeks – and indeed it’s clear the economy is now outperforming last summer when restrictions were also low. But the Bank’s view on growth has already been towards the more optimistic end of the spectrum, and the spread of the new Delta variant adds an extra dimension of uncertainty (though our view for now is that the economic impact probably won’t be huge). We also doubt the Bank will feel too compelled to shift market expectations as they currently stand.

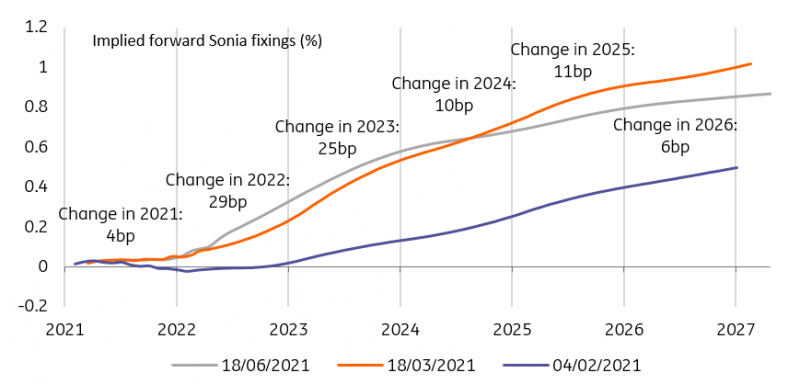

Bank of England rate hike expectations

Source: Refinitiv, ING

We're in the camp looking for a rate hike in 2023

Having said all of that, the last set of forecasts from May (which won’t be updated this time) effectively endorsed the market’s then-view of 20bp of tightening by 2Q23. Forecasts based on that interest rate profile yielded no excess supply by the tail-end of its policy horizon, and kept inflation roughly at 2% - a subtle way of saying that market pricing was roughly sensible.

For now, we’re in the camp looking for the first rate hike in 1Q23. Headline inflation is likely to touch 2.5% later this year, but is likely to die down into mid-2022 as the reopening spikes of the next few months fade. That, in turn, reduces the pressure on policymakers to exit the current level of stimulus.

We certainly wouldn’t rule out an earlier move though. Possible triggers could include a more rapid unwinding of household savings, given the economic outlook is particularly sensitive to even small percentage changes in the amount of the savings stockpile that is spent (the BoE assumes roughly 10%). Wage growth is also key, and there are already anecdotal reports of firms facing shortages of staff in hospitality, though our feeling is that this is likely to prove temporary.

When discussing future rate rises, it’s also worth remembering that the Bank of England, under Governor Andrew Bailey, seems to want some of the heavy lifting to come from shrinking the balance sheet. We wrote about how this could work before last month’s meeting.

GBP rates already in full tightening mode

We typically tend to separate the yield curve in two sections: the front-end which is mostly impacted by domestic economic developments and the central bank's policy outlook, and the long-end where global demand for duration has a greater impact. This broad generalisation clearly doesn’t seem to apply in cases of a perceived Fed policy U-turn. In this instance, both ends of the GBP swap curve reacted to Powell’s hawkish and upbeat tone. We think there is a danger in reading too much into the UK implications heading into the June BoE meeting.

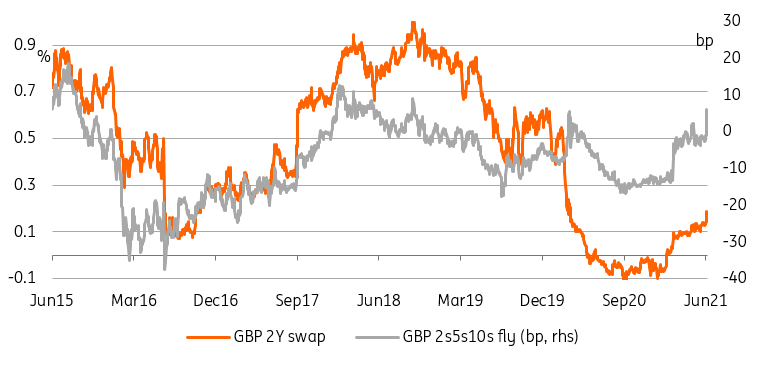

GBP 2s5s10 cheapening shows markets see BoE implications to the Fed’s hawkish tone

Source: Refinitiv, ING

Exhibit A is the cheapening of the GBP 2s5s10s butterfly, no doubt in sympathy with the same occurrence in the USD curve. With a hiking cycle likely to start within two years, the belly of this structure is most sensitive to BoE hike expectations. By that metric alone, tightening bets are as hot as they were in early 2018, in the middle of the previous hiking cycle. There is a clear risk to this move.

Firstly, the read across from the FOMC tone to BoE policy is far from certain, as the BoE already endorsed market pricing of hikes by mid-2023. Secondly, rising Covid 19 cases put the reopening agenda at risk. Even if it is too early to draw firm economic conclusions, a more cautious tone may well impact rates earlier than economic data are impacted.

Of course, there are factors that could explain the 5Y having risen so far ahead of other tenors beyond policy expectations. This brings us to the flattening of the long-end. We ascribe the failure of long-dated sterling rates to rise further after the May spike to a more cautious global outlook, as well as to a dovish tone repeated ad nauseam by other major developed market central banks. This has not prevented 10Y gilts from underperforming Treasuries by roughly 20bp this quarter, but their upside is capped by the global demand for fixed income carry trades. Unlike the cheapening of 5Y GBP swaps, this is a development that is more likely to persist beyond the June BoE meeting.

Read the original analysis: Bank of England preview: Edging towards a 2022 rate hike?

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.