Bank of England keeps policy steady but pushes back against rate cut expectations

The Bank of England may have kept rates on hold, but we're seeing the first signs of pushback against financial markets which are starting to price in rate cuts for 2024. We think investors are right to be thinking that way and we expect the first cut over summer next year.

The Bank of England has kept rates on hold for a second consecutive meeting and, barring some major unpleasant surprises in the data between now and Christmas, it’s fair to say the tightening cycle is over.

On the face of it, this latest decision looks neither surprising nor controversial. Six members voted to keep rates on hold and three for a hike, in line with what more or less everyone had expected. With the exception of Sarah Breeden, where this was her first meeting, the remaining members voted exactly as they did in September – a recognition that we’ve had very little data since then, and what we have had hasn’t moved the needle for policy.

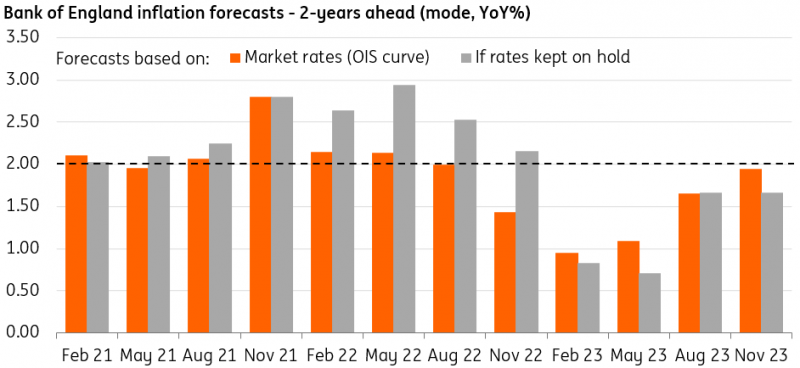

But beneath the surface, we detect hints that the Bank is uncomfortable with markets beginning to price rate cuts for next year. Ahead of the meeting, investors were pricing at least two 25 basis point cuts by the end of 2024. BoE Governor Andrew Bailey is quoted as saying it’s “too early” to be talking about cuts, while the statement says rates need to be restrictive for “an extended period of time”. That's a slight hardening in the language compared to what we'd seen in August and September. And while the Bank’s models forecast inflation a touch below target in two years' time – which is considered to be the time horizon over which monetary policy is more effective – they show headline CPI at 2.2% once an “upside skew” is applied.

That’s policymakers trying to tell us that, at the margin, the amount of tightening and subsequent easing may be insufficient to get inflation back to target. That said, the committee is visibly putting less weight on its forecasts than it once might have done given ongoing uncertainty and poor model performance.

The Bank's models point to inflation at or just below target in two years' time

Source: Bank of England

As has been clear since the start of the summer, this is a central bank whose overriding goal now is to convince investors that it won’t need to cut rates for a significant period of time. However, we believe markets are right to be thinking about rate cuts from next summer. As the BoE itself acknowledges, much of the impact of past tightening is still to hit the economy. We estimate the average rate on mortgage lending, which so far has gone from 2% to 3.1%, will go to 3.8% by the end of 2024 as more homeowners refinance. It will be higher still if the Bank ultimately doesn’t cut rates next year.

We also forecast core inflation to be below 3% by next August – and assuming the jobs market continues to gradually weaken, we think the Bank will be in a position to take its foot off the brake. We’re forecasting a gradual easing cycle that takes Bank Rate back to just above 3% by the middle of 2025 from the current 5.25% level.

Read the original analysis: Bank of England keeps policy steady but pushes back against rate cut expectations

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.