Bank of Canada set to cut again despite inflation uptick

Lingering trade-induced uncertainty continues to weigh on Canadian activity and carries risks of broader jobs market deterioration. We expect the BoC to overlook higher-than-expected jobs and inflation data and cut by 25bp on 29 October. The door may be left open to more easing, and CAD should remain vulnerable against most of the G10.

Sticky dovish pricing despite data

October has delivered broadly hawkish hard data for the Bank of Canada. The September jobs report showed solid 60k employment gains while unemployment held stable at 7.1%. Earlier this week, headline inflation (also for September) rose faster than consensus to 2.4%, with both core measures – median and trim – also accelerating by 0.1-0.2% above 3.0%.

Yet, markets are pricing in 21bp of easing for the 29 October meeting. We are aligned with the consensus majority in expecting a 25bp cut to 2.25% next week. The rationale lies – once again – in the bleak Canadian economic outlook.

Activity and jobs picture remains grim

The Bank of Canada’s quarterly Business Outlook Survey, published earlier this week, is a key input into policy decisions. The third-quarter release showed that while sentiment marginally improved relative to the second quarter, uncertainty around trade policy continues to weigh heavily on investment and hiring plans.

The “future sales” indicator dropped back into negative territory (with more companies reporting expected sales decreases) for the first time in 2025. And the percentage of respondents reporting that indicators of future sales have deteriorated is the highest since the pandemic.

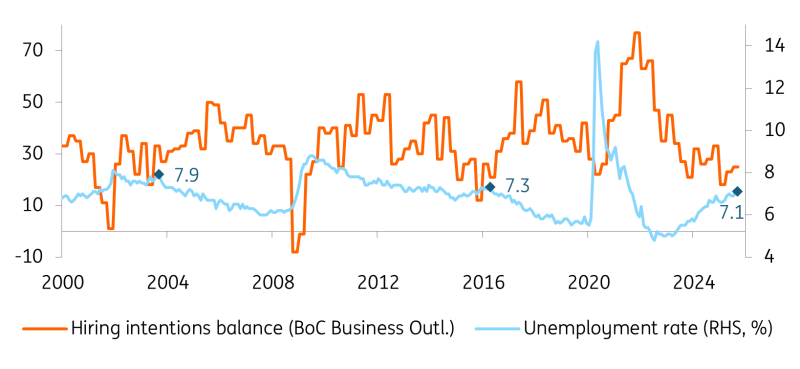

Labour market weakness remains the most sensitive and potentially actionable data for the Bank of Canada. Despite stable unemployment in September and slight improvements in hiring intentions, 63% of firms expect either unchanged (50%, down from 57% in the second quarter) or reduced (13%, up from 10% in the second quarter) workforce levels. Excluding the pandemic period, similar responses have historically coincided with higher unemployment rates – peaking at 7.3% in 2015 and 7.9% in 2003.

Unemployment can rise further, based on BoC survey result

Source: ING, Macrobond

Inflation uptick not too concerning

The BoC survey also pointed to limited inflationary risks, with many firms stating that weaker demand is limiting their ability to pass higher costs through to their selling prices. Wage growth expectations for the next 12 months averaged 3.1% – a steady decline and notably below the 3.6% reported in the September jobs report.

Combined with similar disinflationary trends in shelter costs as seen in the US, the BoC’s baseline projection for CPI to average 2% in 2026–27 still appears realistic. As new economic forecasts are released at this October meeting, we expect the Governing Council to look through the September inflation uptick and proceed with a rate cut.

Communication has leaned dovish

The BoC’s own communication is another factor contributing to our call for an October cut. Governor Tiff Macklem’s 17 October speech – delivered after the jobs data but before the inflation release – downplayed employment gains and highlighted “very soft hiring” across the economy, particularly in tariff-impacted sectors.

The statement accompanying the September rate cut also emphasised risks to growth and the labour market. In particular, it referred to uncertainty about USMCA renegotiations as a major risk. Despite an amicable meeting between Canadian Prime Minister Mark Carney and US President Donald Trump earlier in October, there has been no tangible progress on trade relations, and the risk of tumultuous USMCA talks ahead is likely to weigh on the economic outlook.

It will be hard to shut the door to more cuts

While the October statement and guidance may lean slightly more hawkish than September’s, we believe it will be difficult for the BoC to signal the end of the easing cycle. Tariff-related risks remain elevated, and allowing markets to price in further dovishness could help loosen financial conditions and weaken the Canadian dollar – a positive for exports.

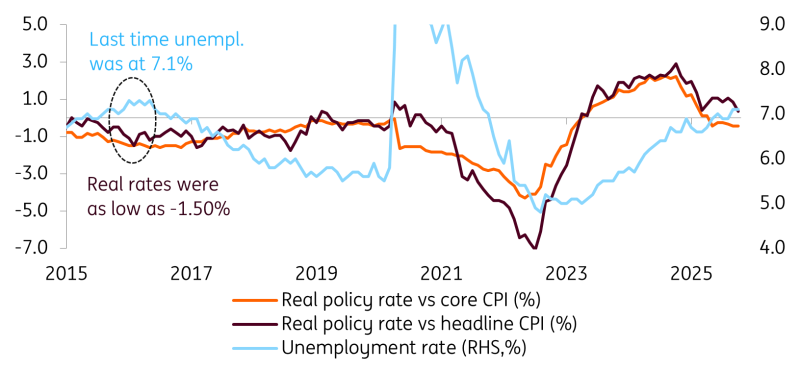

We expect a hold in December, followed by one final cut of 25bp in January, bringing the policy rate to 2.0%. This might look excessively loose, especially relative to the Federal Reserve, but it actually aligns with historical BoC real policy rates, which have often been negative.

As shown below, the last time unemployment was at 7.1%, the real policy rate (both vs core and headline CPI) reached a negative 1.50%, versus the current +0.35% (vs headline) and -0.45% (vs core). Assuming no major uptrends in inflation from here, further easing would not be an aberration.

Negative real rates aren't abnormal in Canada

Source: ING, Macrobond

CAD still looks vulnerable in the crosses

The recent moves in the Canadian dollar have tracked the swings in US sentiment. Net of the short-lived US credit market concerns, the USD rally has dominated G10 FX so far in October, and the loonie is understandably doing better than other majors (euro, pound, antipodeans) given its smaller negative correlation to US dollar strength.

But moving on, we still expect the macro picture in the US to deteriorate, with jobs market and inflation numbers pointing to more Fed cuts beyond the three currently priced in by March 2026. That should pair with BoC easing in placing CAD in an unfavourable position against any other G10 currency outside of the USD.

USD/CAD is around 2.5% overvalued relative to our short-term fair value, and we do expect a return to 1.38 by year-end, primarily driven by USD weakness. But given our call for an October BoC cut and the fact that markets will probably feel little restraint to price in another cut should data justify it, we think it will be a slow decline, with some potential bumps to 1.41 in the near term.

Read the original analysis: Bank of Canada set to cut again despite inflation uptick

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.