Australian Dollar Price Forecast: Bulls look at the RBA

- AUD/USD regains pace, retargeting the 0.7100 barrier on Monday.

- The US Dollar loses momentum as geopolitical tensions seem to subside (kind of).

- The RBA is seen further tightening its monetary policy at its Tuesday meeting.

The Australian Dollar (AUD) stays strong amid elevated inflation at home and the Reserve Bank of Australia’s (RBA) hawkish tilt. This combination keeps the door open for AUD/USD to rise even higher, and it also helps guard against occasional drops. But worries on the geopolitical front should keep rallies from going too high for now.

The generalised improvement in the risk-linked galaxy lends support to the Australian Dollar in quite a promising start to the new trading week, with AUD/USD leaving behind two consecutive daily pullbacks and regaining some upside traction well north of the key 0.7000 threshold.

The pair’s daily bounce comes on the back of renewed selling interest in the US Dollar (USD), as tensions in the Middle East appear to be shrinking a tad.

Australia, steady growth keeps the Aussie supported

Australia’s macro backdrop continues to offer a reasonably solid floor for the Australian Dollar.

Growth remains respectable, inflation is still proving sticky, and the Reserve Bank of Australia (RBA) continues to lean on the hawkish side. For currency markets, that combination tends to keep a meaningful cushion under the Aussie.

Recent data reinforce that view. February’s final Purchasing Managers' Index (PMI) readings showed manufacturing at 51.0 and services at 52.2, both comfortably in expansion territory and broadly consistent with an economy that continues to grow at a steady pace.

Consumer activity is also holding up better than many expected. Retail spending remains resilient, while the trade balance continues to provide support, with the surplus reaching A$2.631 billion in January.

At a broader level, the economy continues to expand at a healthy rhythm, as the Gross Domestic Product (GDP) expanded by 0.8% QoQ in the October to December period and 2.6% YoY, comfortably above the bank’s estimates.

The labour market is beginning to cool slightly, but there are still no signs of a sharp deterioration: the Employment Change increased by 17.8K in January, while the Unemployment Rate held steady at 4.1%. In other words, the slowdown still appears gradual and orderly rather than abrupt.

Progress on inflation, however, remains slow.

January’s headline Consumer Price Index (CPI) held at 3.8% YoY, slightly above expectations, while the Trimmed Mean measure edged higher to 3.4% YoY. The overall direction remains downward, but the pace of disinflation is proving slower than policymakers would ideally like.

From the RBA’s perspective, the job is clearly not finished. The central bank still expects inflation to peak around the second quarter of 2026 before gradually returning toward the midpoint of the 2–3% target band by mid-2028.

Inflation expectations are also showing signs of persistence. The Melbourne Institute’s Consumer Inflation Expectations survey rose to 5.2% in March from 5.0% previously.

China, stabiliser rather than growth engine

China’s role in Australia’s economic outlook has also evolved.

Rather than acting as a powerful engine for global growth, the Chinese economy currently looks more like a stabilising force.

At first glance, headline figures still suggest a reasonably solid trajectory. China’s GDP grew by 4.5% YoY in Q4 2025. Retail Sales also increased by 2.8% YoY in the January to February period, while trade data remained strong after the surplus reached $213.62 billion in the same period, with exports up 21.8% and imports rising 19.8%.

Business surveys, however, paint a more nuanced picture after the official PMI readings from the National Bureau of Statistics (NBS) remained in contraction territory in February, with manufacturing at 49.0 and services at 49.5.

Private surveys tell a somewhat stronger story. The RatingDog indicators remained comfortably in expansion territory, with manufacturing at 52.1 and services at 56.7, both slightly higher than the previous month.

Inflation pressures remain subdued. The Consumer Price Index (CPI) rose just 0.2% YoY, while the Producer Price Index (PPI) remained in deflation at minus 1.4% YoY.

Meanwhile, the People’s Bank of China (PBoC) left the one year and five year Loan Prime Rate (LPR) unchanged at 3.00% and 3.50% in late February, as widely expected.

For the Australian Dollar, the takeaway is fairly straightforward. China is no longer acting as a major drag on the outlook, but it is not yet providing a powerful growth impulse either.

RBA, policy stays firmly restrictive

Attention in Australia is now turning to the upcoming interest rate decision from the RBA, where investors widely expect another 25 basis points increase that would lift the Official Cash Rate (OCR) to 4.10%.

Following the latest rate increase, Governor Michelle Bullock said financial markets have remained broadly orderly despite the escalation of tensions in the Middle East. For Australia, the implications are mixed. As a major energy exporter, higher commodity prices can support national income, although a prolonged geopolitical shock could still weigh on household spending.

Bullock also stressed that inflation remains too high and reiterated that anchoring inflation expectations remains the Board’s top priority. Policymakers will therefore continue to monitor incoming data closely, with each meeting effectively remaining live.

She also acknowledged that if labour market tightness persists, the Unemployment Rate may need to rise somewhat in order to help bring inflation back under control.

Markets currently assign roughly a 72% probability of another quarter percentage point increase tomorrow and just over 72 basis points of tightening by year-end.

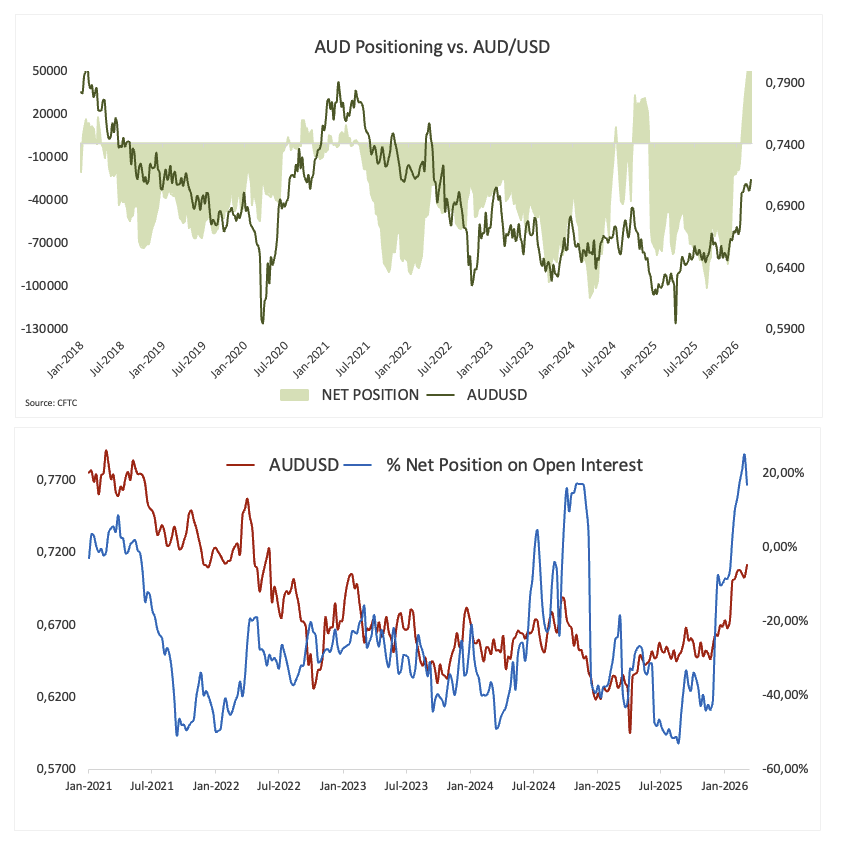

Positioning: speculators trim bullish AUD bets

The latest figures from the Commodity Futures Trading Commission (CFTC) show that speculative positioning in the Australian Dollar eased during the week to March 10.

In fact, non-commercial traders reduced their net long exposure to around 54.2K contracts. The drop from the previous week signals a clear trimming of bullish bets on the Aussie among large speculative accounts.

At the same time, open interest climbed to nearly 316K contracts, pointing to a noticeable increase in market participation.

This combination sends a message that is comparable to what we have seen in other G10 currencies. Net longs went down, but open interest went up, which means that the move wasn't just a big sell-off. Instead, the statistics suggest that investors are actively repositioning, with some cutting down on their bullish exposure and new positions entering the market.

Even after the change, the overall structure is still net long AUD, which means that the general mood toward the currency is still positive.

The most recent positional snapshot shows three indications.

First, the bullish bias toward the Aussie is still there, although it has weakened a little since the recent cutting of longs.

Second, the increase in open interest shows that the market is becoming more two-sided, with more people joining instead of the market only lowering risk.

Third, the AUD's position is still very vulnerable to global macro storylines, especially changes in the forecast for the US Dollar and how China's economy is going.

Overall, the bullish posture is slowing down rather than changing the way people feel about the Aussie.

What's going to happen next with AUD/USD?

Near term: the pair will probably keep following the US Dollar and the larger geopolitical situation. Changes in trade policy, strong US statistics, or more violence in the Middle East may swiftly change how people feel about the market. Tuesday’s RBA meeting will be the next key event.

Risks: The AUD is, by nature, prone to cycles. It often falters when global investors grow wary, when China's economy decelerates, or when the US Dollar unexpectedly gains strength. Ultimately, the outlook is cautiously optimistic, though contingent.

Technical levels

In the daily chart, AUD/USD trades at 0.7060. The near-term bias is mildly bullish as spot holds well above the rising 55-, 100- and 200-day Simple Moving Averages (SMAs), which cluster in the 0.66–0.69 region and underline a medium-term uptrend. Price has bounced from the 23.6% Fibonacci retracement at 0.6976, measured from the 0.6421 low to the 0.7147 high, showing buyers defending shallow pullbacks within the broader advance. The Relative Strength Index (RSI) has recovered to 51 after easing from overbought territory, indicating momentum has normalised but remains consistent with a modest upside bias rather than a full reversal.

Immediate resistance is located at the recent horizontal cap near 0.7158, with the 0.7147 swing high reinforcing this ceiling; a daily close above this area would open the way toward 0.7283, followed by the more distant 0.7661 barrier. On the downside, initial support is seen at the 23.6% retracement at 0.6976, ahead of the horizontal level at 0.6897, where a break would expose the 38.2% retracement at 0.6870. Deeper losses would then bring the 0.6660 and 0.6593 supports into focus, where they converge with the rising SMAs, a zone that would need to give way to challenge the broader bullish structure.

(The technical analysis of this story was written with the help of an AI tool.)

All in all

In the meantime, Australia's robust internal economic indicators and a relatively aggressive RBA should support a generally positive trend for spot.

That being so, the AUD's strength is still conditional; it usually does best when people are willing to take risks throughout the world. If global tensions rise or the market becomes more volatile, the US Dollar might swiftly reclaim the upper hand, placing further pressure on the pair.

RBA FAQs

The Reserve Bank of Australia (RBA) sets interest rates and manages monetary policy for Australia. Decisions are made by a board of governors at 11 meetings a year and ad hoc emergency meetings as required. The RBA’s primary mandate is to maintain price stability, which means an inflation rate of 2-3%, but also “..to contribute to the stability of the currency, full employment, and the economic prosperity and welfare of the Australian people.” Its main tool for achieving this is by raising or lowering interest rates. Relatively high interest rates will strengthen the Australian Dollar (AUD) and vice versa. Other RBA tools include quantitative easing and tightening.

While inflation had always traditionally been thought of as a negative factor for currencies since it lowers the value of money in general, the opposite has actually been the case in modern times with the relaxation of cross-border capital controls. Moderately higher inflation now tends to lead central banks to put up their interest rates, which in turn has the effect of attracting more capital inflows from global investors seeking a lucrative place to keep their money. This increases demand for the local currency, which in the case of Australia is the Aussie Dollar.

Macroeconomic data gauges the health of an economy and can have an impact on the value of its currency. Investors prefer to invest their capital in economies that are safe and growing rather than precarious and shrinking. Greater capital inflows increase the aggregate demand and value of the domestic currency. Classic indicators, such as GDP, Manufacturing and Services PMIs, employment, and consumer sentiment surveys can influence AUD. A strong economy may encourage the Reserve Bank of Australia to put up interest rates, also supporting AUD.

Quantitative Easing (QE) is a tool used in extreme situations when lowering interest rates is not enough to restore the flow of credit in the economy. QE is the process by which the Reserve Bank of Australia (RBA) prints Australian Dollars (AUD) for the purpose of buying assets – usually government or corporate bonds – from financial institutions, thereby providing them with much-needed liquidity. QE usually results in a weaker AUD.

Quantitative tightening (QT) is the reverse of QE. It is undertaken after QE when an economic recovery is underway and inflation starts rising. Whilst in QE the Reserve Bank of Australia (RBA) purchases government and corporate bonds from financial institutions to provide them with liquidity, in QT the RBA stops buying more assets, and stops reinvesting the principal maturing on the bonds it already holds. It would be positive (or bullish) for the Australian Dollar.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.