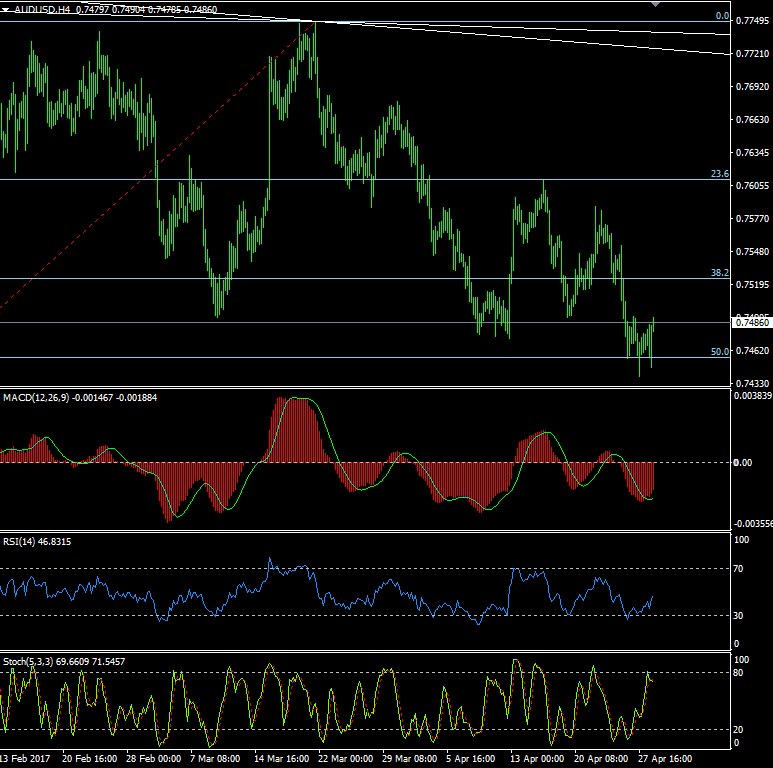

AUDUSD: The price action leaves the recent 0.7440/0.7500 range intact

The Aud was fairly subdued on Friday, near 0.7475 until the release of the US GDP, at which point it fell sharply to a low of 0.7447 ahead of an equally quick recovery to finish the week just below the high of 0.7490.

Over the weekend, China released the official Manufacturing PMI (April): 51.2 (expected 51.7) and the Services PMI (April): 54.0 (prior was 55.1). Both were weaker than expected and caused an early gap lower, to 0.7470 in early Monday trade although this has since been closed, with the Aud currently back at 0.7485.

The price action leaves the recent 0.7440/0.7500 range intact, and with the dailies still looking pretty neutral this could continue through Monday, so a cautious stance is required. The 4 hour momentum indicators are now pointing higher though, and on the topside the initial resistance will be seen at Thursday’s high (0.7491) and then again at 0.7510 and 0.7525. On the downside, support will be seen at 0.7465/70 and then again at 0.7440/50 although this seems a little less likely to be seen again today. If wrong, below 0.7440 would then find only minor support until we reach 0.7385.

As before, from a structural standpoint I prefer trading the Aud from the short side, and selling rallies is preferred although given the look of the 4 hour indicators there may be better levels to do so. Short term traders may want to trade from the long side today, particularly if we open the week with a decent downside gap following the release of the weekend China data.

Economic data highlights will include:

M: AIG Mfg Index, TD Inflation, RBA Commodity Index

T: AIG Services Index, Caixin China Mfg PMI, RBA Interest Rate Decision/Statement, Australian Budget

W: New Home Sales

T: AIG Construction Index, Caixin China Services PMI, RBA Governor Lowe Speech

F: RBA Monetary Policy Statement

Author

Jim Langlands

FX Charts

Jim Langlands began his trading career in the commodities markets in London in 1976, before moving to Australia in 1979 to work as a floor trader on the Sydney Futures Exchange.