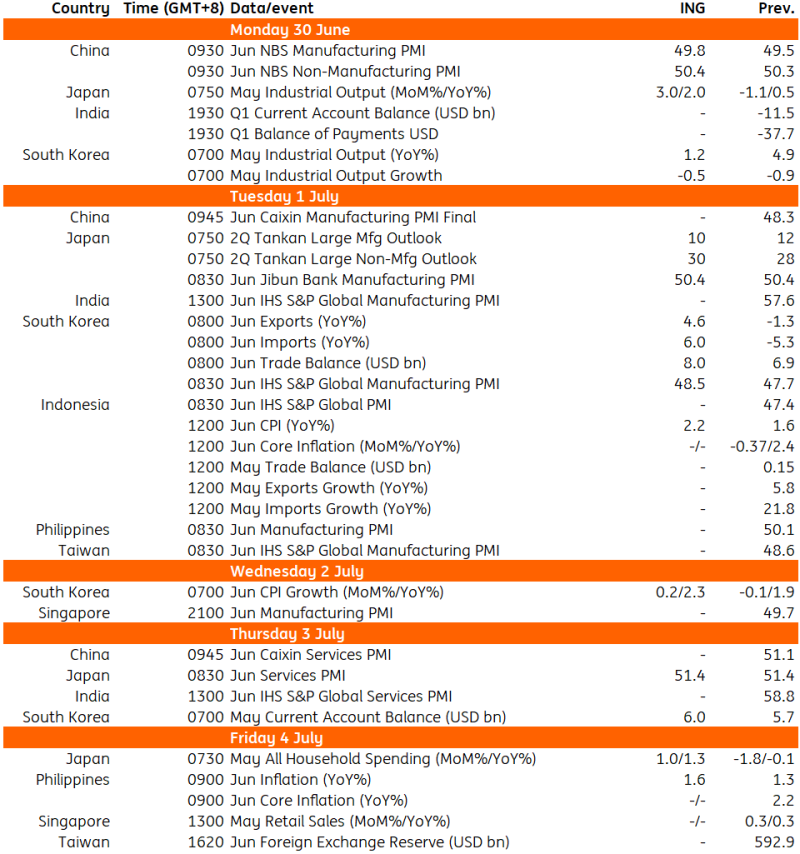

Asia week ahead: Data to show uptick in inflation in South Korea and Indonesia

CPI data will be released in Indonesia, the Philippines, and South Korea next week. A rise in inflation is expected, driven by higher oil prices. Elsewhere, China is set to release its PMI and new export orders, while Japan will publish the Tankan survey and industrial production data.

South Korea: Exports, inflation, and industrial production data

As the end of the 90-day hold on reciprocal tariffs approaches, exports are projected to rebound strongly, primarily driven by the autos and semiconductor sectors. However, there is caution regarding the sustainability of this recovery, with manufacturing PMI expected to remain below the neutral level.

Meanwhile, inflation is expected to accelerate in June, influenced by increases in gasoline and fresh food prices.

Regarding monthly activity data, industrial production is expected to decline for a second consecutive month, as suggested by weak export performance in May. Nonetheless, consumption and equipment investment are likely to improve, supported by a recovery in consumer sentiment and ongoing investments in the IT sector.

Philippines: Slight uptick in inflation expected

We expect a slight pick-up in CPI inflation to 1.6% YpY in June, primarily driven by the surge in global oil prices following the Iran-Israel conflict, resulting in domestic fuel price hikes. However, the increase in domestic fuel prices should be temporary and local pump prices are expected to fall in July.

Indonesia: Inflation likely to rise

CPI inflation should rise above 2% YoY levels. The contribution of transportation to headline CPI inflation has fallen close to zero over the past two months. This should recover now, reflecting higher global oil prices. The indirect impact through higher food prices could also add to headline inflation. We forecast headline June CPI inflation at 2.2% YoY.

Japan: Tankan survey and industrial production data

The Tankan survey is important as the Bank of Japan monitors business sentiment for future investments and hiring. We anticipate a decline in the manufacturing outlook but a modest rise in non-manufacturing. Despite uncertainty over US trade policy, domestic activities should remain strong. May industrial production is expected to rebound from April's decline due to increased production in autos and auto parts.

China: PMI and new export orders

June PMI data will be the highlight of China's data calendar in the upcoming week. The official PMI is set for release on Monday, where we are looking for the manufacturing PMI to remain in contraction but see a modest uptick to 49.8 on the month. Markets are also looking for the non-manufacturing PMI to remain broadly unchanged on the month.

The Caixin manufacturing PMI is set to be released on Tuesday, followed by the services PMI on Thursday. In both reports, the new export orders subindex will be closely monitored to assess any recovery following the recent tariff reductions.

Key events in Asia next week

Source: Refinitiv, ING

Read the original analysis: Asia week ahead: Data to show uptick in inflation in South Korea and Indonesia

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.