AI keeps stocks flying while Oil warns about inflation's comeback

The Nasdaq 100 spent the first week of June doing what it has been doing for months – grinding higher and dragging the rest of the tech sector with it. Inflation, meanwhile, decided not to cooperate. May CPI came in at 4.2%, the hottest reading in more than three years, while oil prices stayed supported by events in the Middle East. None of that was supposed to make growth investors comfortable. Yet here we are.

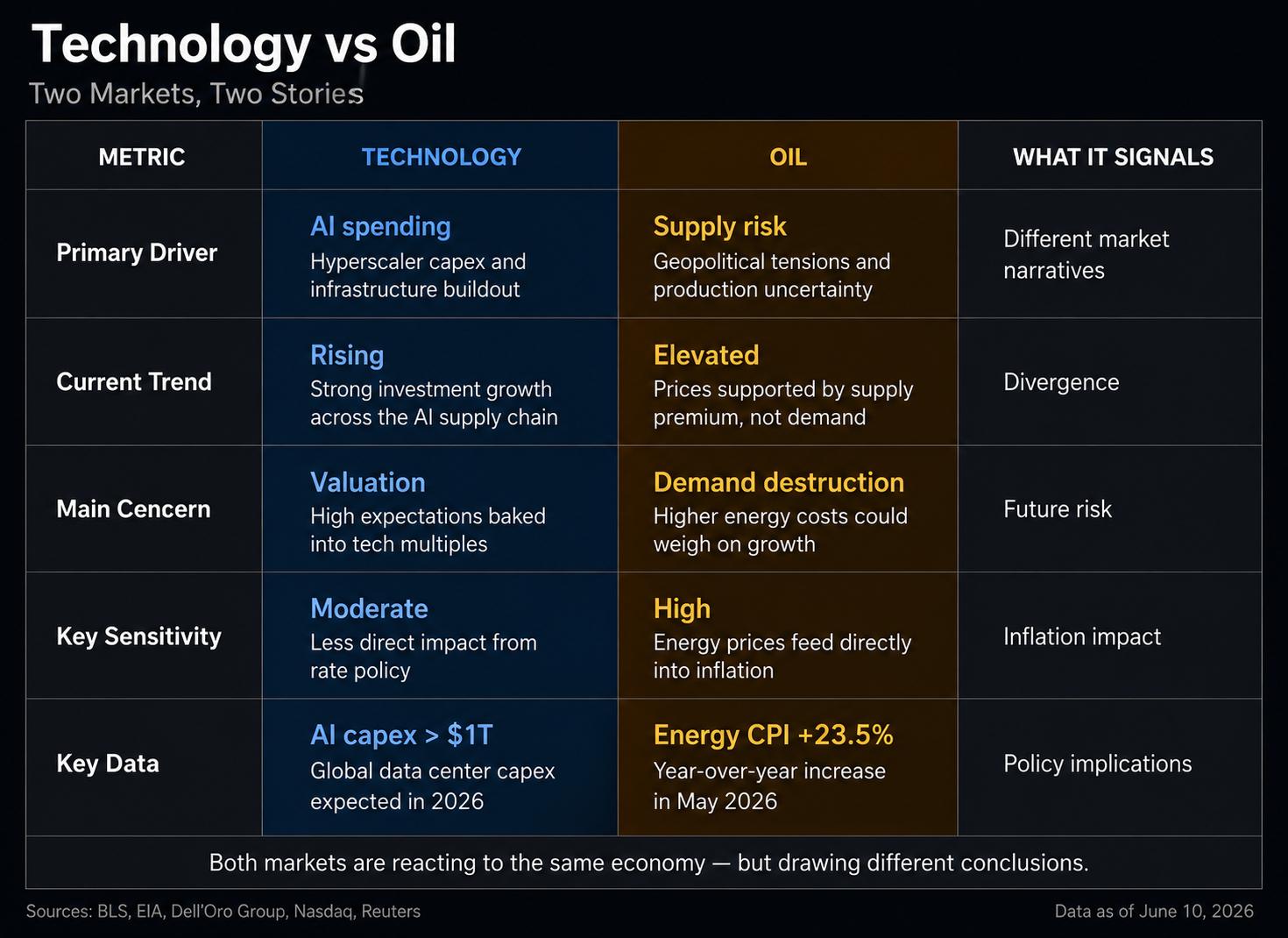

Those developments might seem difficult to reconcile. For traders watching the US100 vs WTI, however, the gap between the two markets has become one of the defining macro stories of 2026.

Why investors keep buying technology

The latest rally in tech stocks and inflation concerns did not emerge from optimism alone. Corporate spending plans continue to support the growth story.

Nvidia's Vera Rubin platform moved closer to deployment, easing some of the concerns that had surrounded AI hardware constraints earlier this year. At the same time, hyperscale cloud providers continue spending aggressively on data centers, networking equipment, power infrastructure, and accelerator deployments. According to a June report from Dell'Oro Group on AI infrastructure investment trends, global data center capital expenditures are now expected to exceed $1 trillion in 2026 as AI-related construction and hardware spending continue to expand.

That spending cycle sits at the center of current AI investment trends. Unlike previous technology booms, the biggest buyers are not speculative startups chasing funding rounds. The money involved is hard to ignore. Microsoft, Amazon, Alphabet, and Meta are spending at levels that would have sounded unrealistic not long ago.

That spending sits at the heart of many AI investment trends and 2026 forecasts. Demand for computing power keeps growing, and so far there are few signs that the companies building AI infrastructure are preparing for a slowdown.

At the same time, much of the discussion has moved toward agentic AI investment trends. The idea is simple enough: if software ends up doing more work on its own, it will need even more computing resources behind the scenes. Investors have been quick to connect those dots.

Expectations that these applications will require more computing resources have strengthened demand forecasts throughout the AI supply chain.

As a result, Nasdaq and S&P 500 record highs have persisted even as inflation concerns have returned. Equity investors continue focusing on future earnings potential rather than today's macroeconomic headwinds.

What Oil is telling the market

The message coming from oil looks very different.

The May CPI report released on June 10 showed energy prices rising 23.5% from a year earlier. Gasoline prices increased 40.5%, while fuel oil climbed 58.9%. According to the U.S. Bureau of Labor Statistics, energy was one of the clearest sources of inflation pressure in the May report.

At the same time, WTI crude oil has struggled to establish a clear direction. Prices remain supported by geopolitical uncertainty, yet demand expectations have weakened noticeably. The U.S. Energy Information Administration's June outlook points to softer global petroleum consumption than expected earlier in the year.

That contradiction explains why nasdaq vs. oil has become such a closely watched macro relationship. Oil is usually easier to read than this. Higher prices often go hand in hand with stronger demand. Lately, though, traders have been paying at least as much attention to supply risks as to consumption trends.

That is not great news for the Fed. More expensive energy can keep inflation under pressure even if parts of the economy are already starting to cool. That dynamic helps explain the widening gap between asset prices and signals coming from parts of the real economy.

For traders evaluating the liquidity trade vs. the real economy, oil continues to serve as a reminder that inflation pressures have not disappeared.

The trading implications of the divergence

The core thesis behind Trade Nasdaq vs. Oil is straightforward. Equity investors continue betting that AI-related earnings growth can outweigh the drag from higher energy costs and restrictive monetary policy.

There is a reasonable case for that view. Corporate investment remains strong. Earnings expectations for major technology companies continue to improve. Several analysts tracking Taiwan AI investment trends note that semiconductor manufacturers are still expanding Taiwan AI packaging and production capacity to support expected AI demand through the second half of the year.

Yet the risks are becoming harder to ignore.

Author

Amir Razak

Versus Trade

Malaysian-born market analyst Amir Razak cuts through the noise every week, breaking down Versus Pairs and explaining what is really driving one asset ahead of another.