Tech rout weighs on US stocks as the USD clocks a fresh 2026 high

Equities: AI doubts weigh on tech, Nasdaq 100 Sinks 3.3%

Major US equity benchmarks ended Tuesday’s session considerably in the red, with the Nasdaq 100 down 3.3%, the S&P 500 off by 1.4%, and the Dow Jones down 0.1%. Stocks were largely weighed down by tech amid doubts over the AI-driven rally; the Philadelphia Semiconductor Index (SOX) slid nearly 8%.

Overnight in Asia, however, things are a little calmer, with Japan’s Nikkei 225 down around 0.2%, and South Korea’s KOSPI up 3.7%, with US equity index futures also trading modestly in the green this morning.

Yields fall as traders rotate out of risk

US Treasury yields fell across the curve on Tuesday, with investors bidding government debt as traders unwound some equity exposure. However, it is worth remembering that yields have risen since the Fed’s latest meeting, when 9 of the 18 officials who submitted a dot indicated they expect higher rates this year.

USD hits fresh YTD peak on Fed tightening bets

In the FX space, the USD index caught a bid, adding 0.4% by the close and refreshing YTD highs at 101.43, as markets toy with the idea of policy tightening sometime this year (money markets are pricing in 16 bps). It was a quiet one for the USD/JPY as intervention fears remain front and centre, though the pair is still on the doorstep of entering levels not seen since 1986.

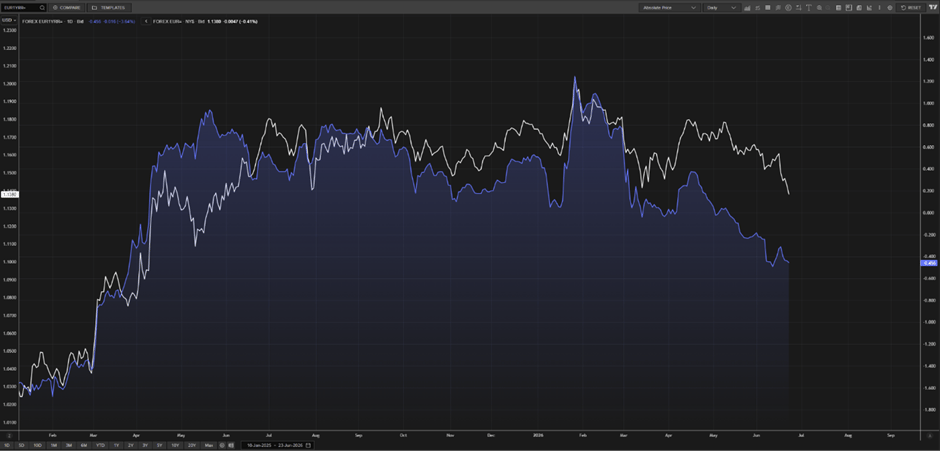

The EUR also clocked fresh YTD lows of US$1.1376, reaching levels not seen since mid-2025. This was a combination of comments from ECB’s Christine Lagarde on Monday, weaker-than-expected German PMI numbers, and, of course, USD upside.

It is also worth noting that this downside move is backed by EUR/USD 1-year risk reversals (see chart below) hitting 0.46%, indicating that the premium for euro puts over calls has reached its lowest level since Trump’s initial tariff shock in early April 2025.

Mixed aussie CPI clouds RBA outlook

Higher-beta currencies – such as the AUD and NZD – collapsed amid the sell-off across risk. We also had the May Australian CPI inflation data land overnight, and this was an important print. However, it came in mixed. Headline YY CPI inflation eased to 4% from 4.2% in April (markets expected 4.3%), while the YY trimmed-mean CPI came in higher at 3.6%, surpassing the 3.5% consensus and April’s 3.4% reading.

There was not a lot to do with this report from a trading perspective, with underlying inflation suggesting pass-through of price pressures and a greater chance of RBA tightening, but a softer headline indicates lower energy-related inflation.

Day ahead: Eyes on Australian jobs data and US PCE inflation looms Thursday

As for the day ahead, we have a relatively light data slate, with focus turning to the May Australian jobs report and the May US PCE inflation numbers on Thursday. I will publish a more in-depth preview for the PCE data in tomorrow’s briefing, but the Aussie labour market will be interesting during the Asian session, following April’s report, which showed job losses and rising unemployment.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,