AI could quickly become the Fed’s new problem

A strong economy and a flimsy labor market don’t typically go hand in hand. For the Fed and other central banks, the playbook has long been straightforward: weak hiring calls for lower interest rates, while an overheating economy and inflation above target justify tighter policy. But with AI, that playbook may no longer work.

If firms can sustain, or even increase, output with fewer workers, traditional labor market signals could become harder to interpret, raising the risk of policy missteps with wide-reaching implications for financial markets.

Growth without hiring: Is it possible?

At the micro level, this premise appears contradictory at face value. After all, a successful company would need to hire more workers to increase output and meet rising demand. However, technological progress can allow firms to improve output with a stable, or even a declining, workforce, provided productivity rises at a sufficient pace.

This relationship is presented by the production function, which is generally expressed as Q = f(K,L), where Q is output, K is capital and L is labor. A modified version augments the function with the “productivity factor” (A) and rewrites it as Q = A* f(K,L).

As long as gains in the productivity factor are sufficiently strong, output could continue to grow even if the labor input declines. Companies could also reach a higher output and potentially become more profitable if they can increase A without expanding the headcount.

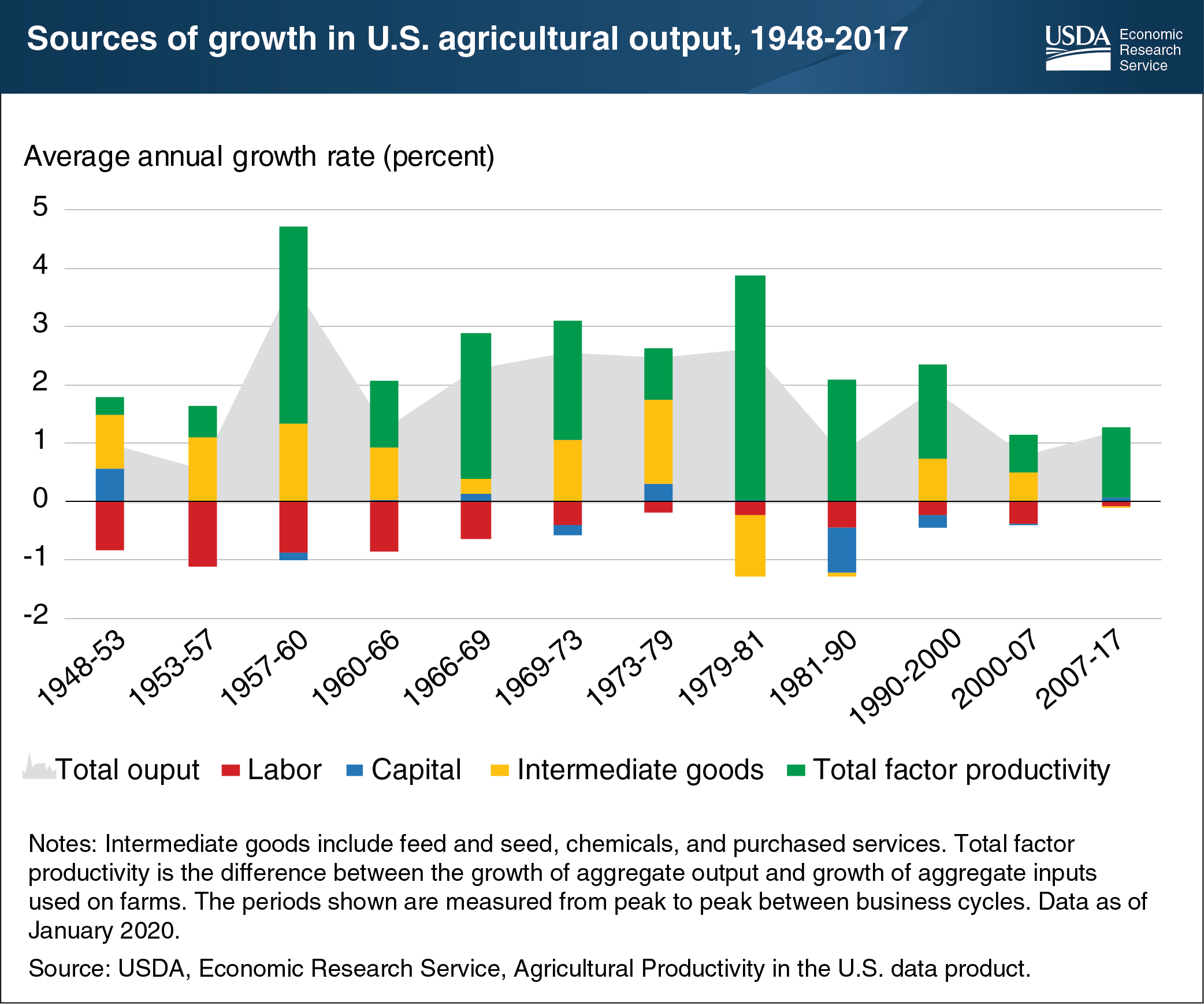

There are historical examples of this dynamic, with the most striking being the agricultural sector. According to the United States Department of Agriculture (USDA) Economic Research Service, the total output produced by US farms nearly tripled between 1948 and 2017, while agricultural labor declined by 76% and the amount of land devoted to agriculture contracted by more than 25%. This divergence highlights that output growth can detach from labor input when there is a strong improvement in productivity through technological progress.

Similar patterns, though not as extreme, can be observed in manufacturing from the 1980s, and during the widespread adoption of computers, software and internet from the late-1990s. Although there was noticeable growth in output and productivity, the impact on employment was less clear as labor was gradually reallocated across other sectors rather than getting eliminated outright.

Where does AI fit within this narrative? Will there be a clear decoupling of output and labor input in the wider economy due to higher productivity, or will the labor displacement remain confined to specific sectors, with displaced labor absorbed elsewhere in the economy, as it has happened before with other technological advances?

There is a unique pattern that emerges with the adoption of AI that could limit job opportunities in the future. In an eye-opening article published in New York Magazine, author Josh Dzieza explains how lawyers and scientists who lost their jobs to AI are now hired by companies on temporary projects to produce training data for more advanced AI models, which could eventually cause more layoffs in these sectors.

Good luck trying to measure technological change

In 1987, economist Robert Solow famously said, "you can see the computer age everywhere but in the productivity statistics." This quote became a testament to how challenging it is to measure the impact of technological advancements on productivity. While the effects of AI are relatively easy to identify at the micro-level, it’s a whole different story when it comes to understanding its aggregate impact on the economy as a whole, with a wide range of estimates.

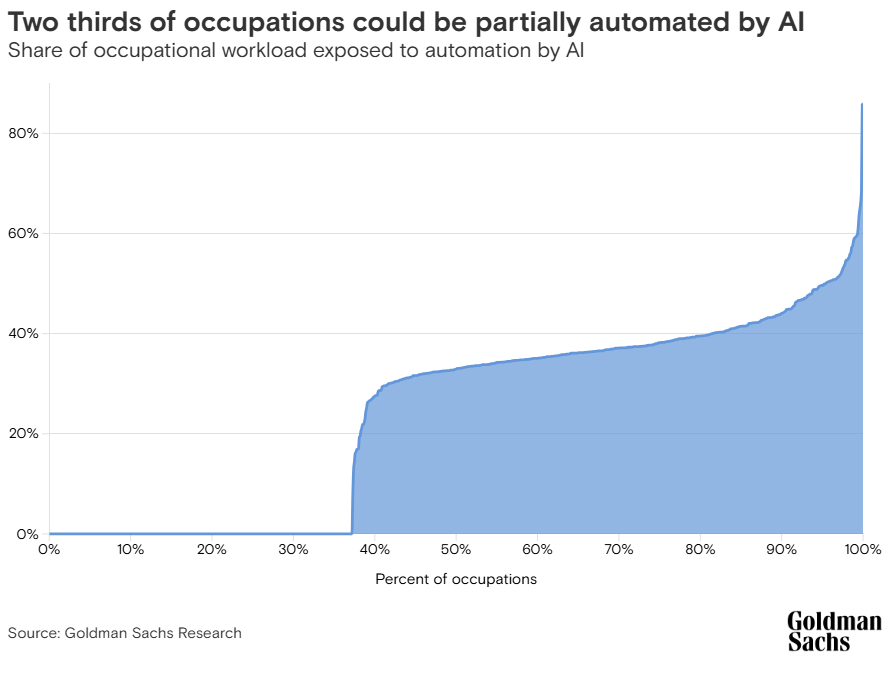

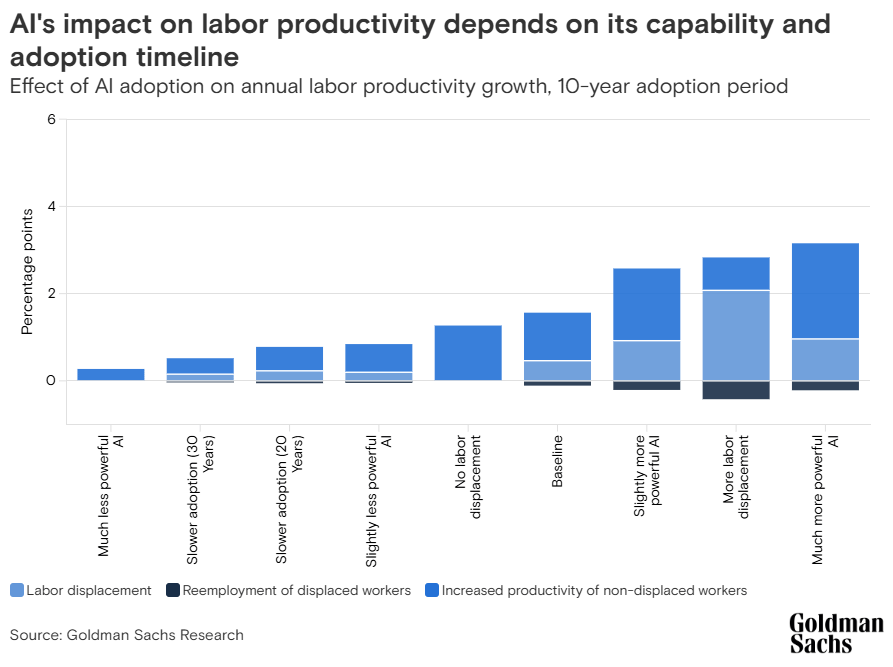

In a research paper titled “The Potentially Large Effects of Artificial Intelligence on Economic Growth,” Goldman Sachs analysts Joseph Briggs and Devesh Kodnani argue that “AI adoption could eventually drive a 7% or almost $7 trillion increase in annual global Gross Domestic Product (GDP) over a 10-year period.”

On a more conservative note, Daron Acemoglu, an Economics Professor at the Massachusetts Institute of Technology (MIT), notes that AI’s positive impact on productivity appears “nontrivial but modest, no more than a 0.71% increase in total factor productivity over 10 years.”

This debate has already reached the Federal Reserve. While speaking at an event at the Yale School of Management, Fed Governor Lisa Cook said that AI can be transformative for the labor market, but acknowledged that there is currently a “low hire low fire regime.” Cleveland Fed President Beth Hammack told CNBC that it is not yet clear what AI will do to the economy, while NY Fed President John Williams said that AI will likely lift the productivity rate but added that it will take a long time to do so.

Taken together, these perspectives point to a key tension. Even if AI is able to generate meaningful productivity gains, both the scale and timing of those gains remain highly uncertain from a macroeconomic and policy perspective.

The Fed’s dilemma

The central bank interest rate is a reactionary tool and lagging in nature. This means that the Fed will only raise interest rates if there is enough data for a sufficient period of time to convince policymakers that inflation will remain persistently high.

On the other hand, the central bank will reduce rates once there is undeniable evidence that the labor market is suffering, which might require consecutive months of increase in the Unemployment Rate or a steady and long-lasting decline in Nonfarm Payrolls (NFP) growth.

Moreover, the interest rate is a limited tool as it can only affect certain aspects of the economy. Lower rates can help companies borrow at lower costs and invest in labor, but they can’t address structural changes in employment due to technological advancements.

This raises the risk of policy misinterpretation. Let’s examine three different scenarios:

1. Labor market is weak and AI-driven growth is underestimated

In such a context, the most reasonable response from the Fed would be to cut interest rates.

With this move, growth could catch up and inflation could reaccelerate, opening the door for a rate reversal. This would:

- Hurt risk-sensitive assets such as stocks

- Hurt the US Dollar initially, but support it later after the policy shift as yields would rise

2. Low-hire environment and resilient growth

In this second scenario, the Fed could assess the economy as being in a “productivity-led growth” state and decide to keep rates higher for longer.

However, in case the AI adoption gains momentum and leads to even fewer job opportunities or more layoffs, it could cause the demand side of the economy to weaken, which would be further exacerbated by high interest rates. In short, AI may delay and mask the transmission from a weak labor market to weak demand, causing the Fed to keep the policy tight.

The concerning part of this scenario is that interest rates can’t fix this problem. Rather, a fiscal policy response or regulation of AI-adoption might be required. Simplifying, this would:

Support stock markets in the near term due to higher profits, but not in the longer term

Support the US Dollar initially, but not for long once market concerns over a downturn grew

3. Labor market cools and AI-driven growth is negligible

In the final scenario, the AI impact on productivity proves to be irrelevant and economic growth fails to gather momentum while the labor market remains cool.

This situation could be seen as a cyclical slowdown in the economy and trigger interest rate cuts. This would pave the way for a classic risk-positive market reaction:

- Support stock markets.

- Weigh on the US Dollar and bond yields.

Conclusion

The rise and adoption of AI introduces a new layer of complexity to the interpretation of macroeconomic data. The good news is that the escalating risk of policy missteps could pave the way for innovation in data collection and assessment.

I personally don’t believe the AI-adoption will lead to a significant improvement in productivity that can be visible in the GDP. However, that won’t stop companies from trying to replace workers with AI to cut costs, at least in the near term.

Hence, a traditional economic slowdown, followed by a loose monetary policy, is the most likely scenario. This is good news for stocks, and bad for the US Dollar and bonds. But again, good luck to the Fed when trying to assess the impact of the technological upheaval that is upon us.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Eren Sengezer

FXStreet

As an economist at heart, Eren Sengezer specializes in the assessment of the short-term and long-term impacts of macroeconomic data, central bank policies and political developments on financial assets.