After the Fed, it’s BoE’s turn

Fed keeps rates steady as expected

The Fed kept rates unchanged yesterday, with Kevin Warsh for the first time at the helm of the central bank. Fed Governors were unanimous in their decision, yet seemed split about the future. The new dot plot is telling, as nine out of 18 are expecting the bank to hike rates by one or more times until the end of the year, in order to lower inflation caused by the high oil prices in the past months. Yet eight are expecting the Fed to keep rates steady, while one seems to be favoring a rate cut.

BoE expected to remain on hold

BoE is widely expected also to keep rates unchanged at 3.75% later today. It’s characteristic that BoE Governor Andrew Bailey highlighted the different position of the BoE in comparison to the ECB, which hiked rates a week ago. Yet the balance of power between the hawks and the doves seems to be shifting among BoE policymakers. We expect the vote count and the bank’s forward guidance to define the market’s reaction to the pound, with a more hawkish approach possibly providing support.

Oil bears ease their dominance

Oil prices continued to drop yesterday, yet the bear’s touch seems to be softening. Market attention remains in the Middle East with hopes for a possible normalisation of the situation being high. Especially the expectations for a swift re-opening of the Straits of Hormuz and a lifting of the US ban on Iranian oil exports, tends to keep the bearish pressure on oil prices.

Gold edges unconvincingly lower

Gold’s price dropped yesterday, losing more than 1% after the Fed kept rates unchanged which had a bullish effect on the USD. The negative correlation of the two trading instruments is still in effect, yet the response of gold to USD’s strengthening was asymmetrically lower. Nevertheless, should the USD continue to rise we may see gold’s price falling and vice versa.

Other highlights for today

Today we get UK’s April employment data, SNB’s, Norgebank’s and CNB’s interest rate decisions, the US weekly initial jobless claims and June’s Philly Fed Business index and Canada’s May PPI rates. In tomorrow’s Asian session, we get New Zealand’s May Trade data, UK’s June GfK consumer Confidence and Japan’s May CPI rates, while BoJ releases the Minutes of the April meeting.

Charts to keep an eye out

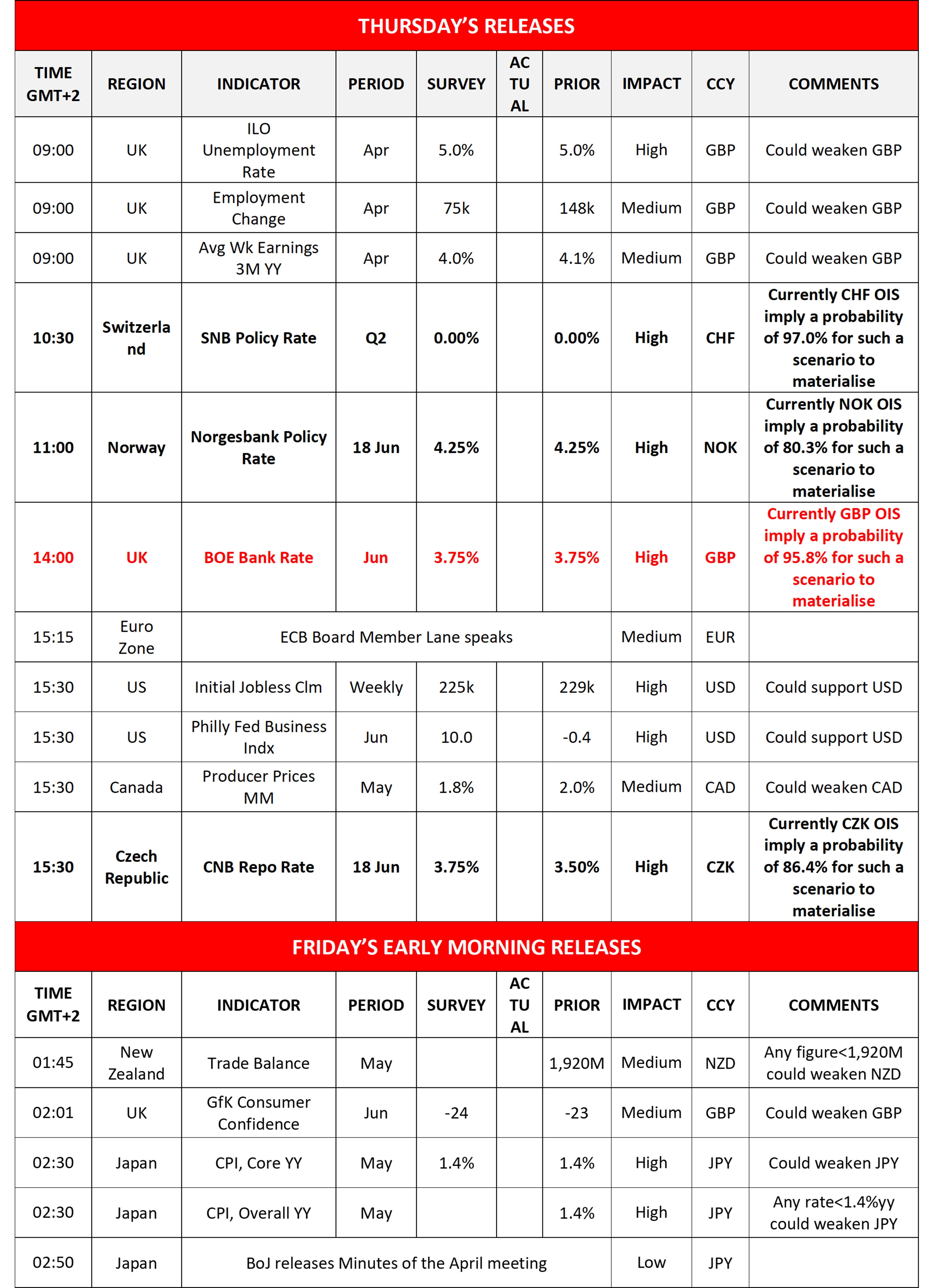

GBP/USD tumbled yesterday, for a short while even breaching the 1.3300 (S1) support line, before correcting higher in today’s Asian session. We maintain our bias for a sideways motion of the pair yet on a technical level we note that the RSI indicator remained between the reading of 50 and 30, implying a bearish predisposition of the market for cable. Should the bulls take over, we may see GBP/USD breaking the 1.3510 (R1) resistance line, which may prove difficult at the current stage. Should the bears be in charge, GBP/USD may break the 1.3300 (S1) support line this time clearly and start aiming for the 1.3155 (S2) support level.

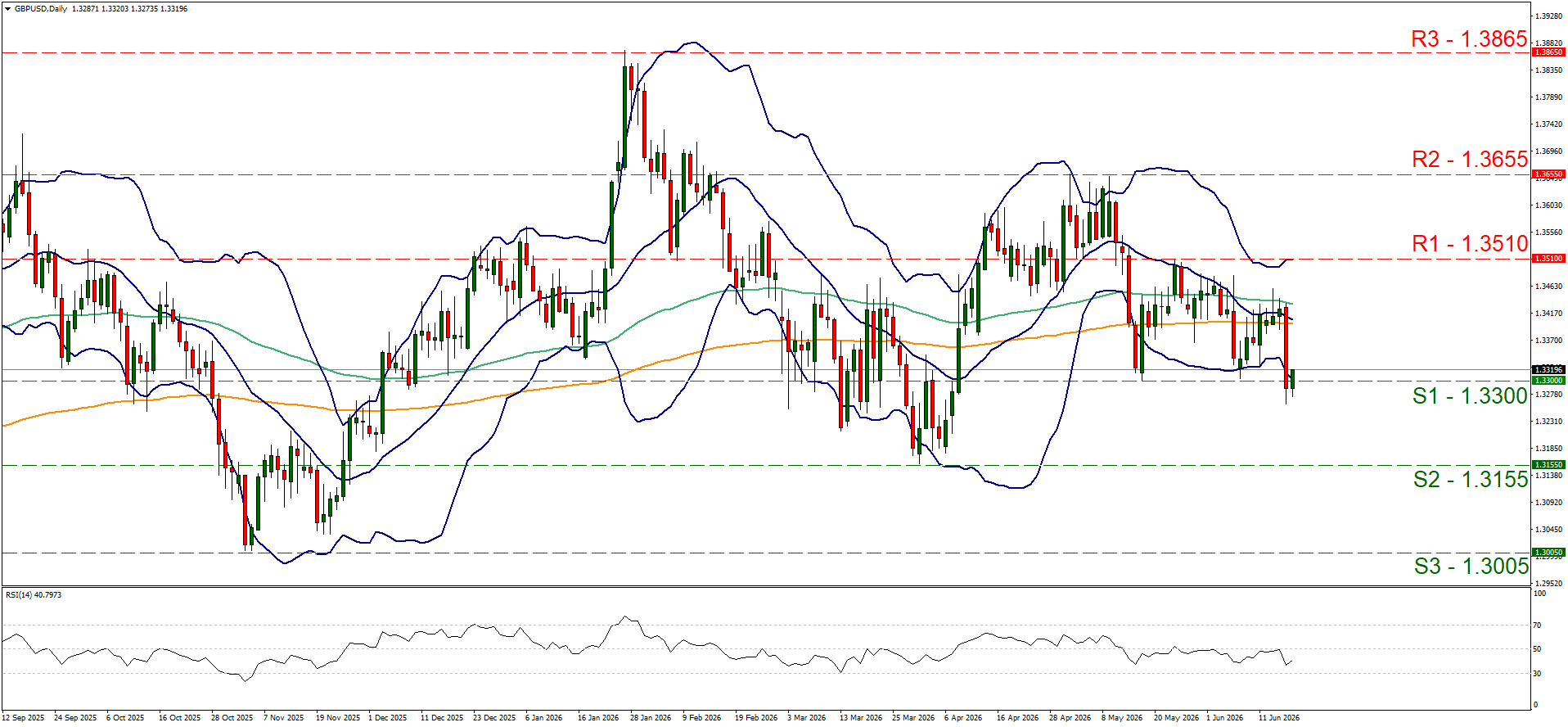

WTI’s price continued to lose ground yesterday, placing come distance between its price action and the breaking the 76.60 (R1) resistance line. We maintain the bearish outlook for WTI, as long as the downward trendline remains in charge, yet note the possibility of WTI being in oversold territory. Should the bears remain in control, WTI’s price may the 69.00 (S1) support line and start aiming for the 60.90 (S2) level. Should the bulls take over, we may see WTI’s price breaking the 82.00 (R2) resistance level, paving the way for the 88.60 (R3) resistance hurdle.

GBP/USD daily chart

- Support: 1.3300 (S1), 1.3155 (S2), 1.3005 (S3).

- Resistance: 1.3510 (R1), 1.3655 (R2), 1.3865 (R3).

WTI daily chart

- Support: 69.00 (S1), 60.90 (S2), 55.00 (S3).

- Resistance: 76.60 (R1), 82.00 (R2), 88.60 (R3).

Author

Peter Iosif, ACA, MBA

IronFX

Mr. Iosif joined IronFX in 2017 as part of the sales force. His high level of competence and expertise enabled him to climb up the company ladder quickly and move to the IronFX Strategy team as a Research Analyst. Mr.