A strong NFP paints markets red

The first week of June in the financial markets was dominated by a single macro trigger: the US May nonfarm payrolls report, released on Friday, June 5. What looked like a routine end-of-week data print turned into the sharpest cross-asset selloff in more than a year. The Nasdaq Composite shed over 4%, the S&P 500 snapped a nine-week winning streak, gold slid from session highs near $4,514, and Bitcoin briefly tested the $60,000 area.

The narrative that had carried risk assets through spring — a softening labour market opening the door to Fed easing — was effectively reversed in one morning. Instead of pricing in rate relief, traders began to reprice the path toward a more hawkish Federal Reserve, with CME FedWatch odds of at least one rate hike in 2026 climbing above 55% shortly after the release.

The NFP surprise: 172K vs ~85K expected

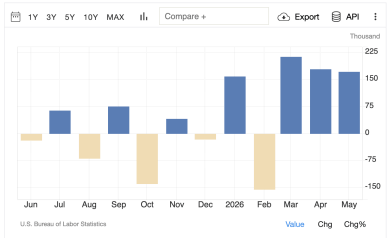

According to the US Bureau of Labor Statistics, total nonfarm payroll employment increased by 172,000 in May, while the unemployment rate held steady at 4.3%. Economists had generally expected a gain of roughly 80,000–85,000 jobs — meaning the actual print more than doubled consensus.

The report also carried meaningful upward revisions. March payrolls were revised up by 29,000 to +214,000, and April was revised up by 64,000 to +179,000. Combined, March and April

employment is now 93,000 higher than previously reported, reinforcing the picture of a labour market that is not cooling as quickly as markets had hoped.

Sector composition was mixed but constructive for the headline number. Leisure and hospitality added 70,000 jobs, local government rose by 55,000, and health care added 35,000. Financial activities declined by 22,000, continuing a downtrend from the sector's peak in May 2025. Average hourly earnings rose 0.3% month-on-month and 3.4% year-on-year, in line with expectations — enough to confirm wage growth without adding a fresh inflation scare on the day.

For markets, the takeaway was straightforward: the US economy is still creating jobs at a pace that reduces urgency for near-term rate cuts. The "good news is bad news" dynamic returned in full force — strong employment data lifted the US dollar and bond yields, while pressuring duration-sensitive equities and non-yielding assets.

Friday's red day: Nasdaq, gold and crypto in sync

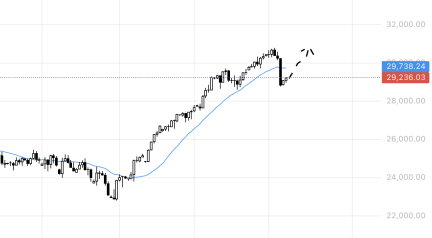

The Nasdaq Composite recorded its worst single-day decline in more than a year, falling roughly 4.0–4.2%. Growth and AI-linked names, which had led the nine-week rally in the S&P 500, bore the brunt of the move as higher-for-longer rate expectations compressed valuation multiples.

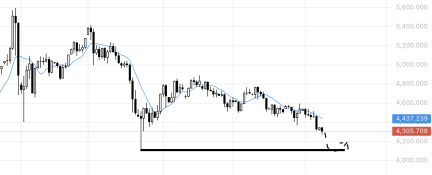

Gold (XAU/USD) also declined, despite its traditional role as a geopolitical hedge. The metal dropped from intraday highs near $4,514 toward the $4,300 area, underscoring that this was a dollar-and-yields-driven repricing rather than a simple flight from equities into safe havens.

Bitcoin followed the same macro script. BTC/USD fell from above $63,000 toward the $61,900 range, with some venues printing brief wicks below $60,000 before a modest bounce into the close.

The VIX spiked on Friday as equity implied volatility reset higher. The CNN Fear & Greed Index shifted back toward fear — a sign that the short-term risk appetite built over the prior nine weeks has been at least partially unwound.

Fed repricing: from cuts to hikes

The most consequential shift was in rate expectations. Before the report, CME FedWatch assigned a 96.4% probability to the Fed holding rates unchanged at the June 17 meeting. What changed was the back half of 2026.

Within minutes of the NFP release, the implied probability of at least one rate hike before year-end climbed from roughly 50% to above 57%. Some pricing now reflects a minority chance of a December 2026 hike — the first non-zero hike odds on FedWatch since 2023. The earliest rate cut carrying majority market odds has been pushed out toward September, at the earliest.

The June 16–17 FOMC meeting will be Kevin Warsh's first as Fed chair. Markets are not pricing an immediate hike at that meeting, but the NFP data strengthens the case for hawkish patience in the statement.

News in focus this week

● Tuesday, June 9: China PPI (May) — input-cost signal for global manufacturing. ● Wednesday, June 10: US CPI (May) — critical follow-up to NFP. Consensus expects headline CPI around +0.5% MoM, lifting the annual rate toward 4.2%.

● Wednesday, June 10: Bank of Canada rate decision.

● Thursday, June 11: US PPI (May); Euro area ECB rate decision.

● Friday, June 12: UK GDP (monthly).

Now let's shift to potential scenarios and trading ideas for the week ahead, covering the post-NFP repricing and the possible short-term swings that may develop around the CPI release and the FOMC meeting.

XAUUSD

Gold is under pressure after Friday's flush. The metal had been in a downswing before the NFP release, and the publication had amplified the decline. The data-driven spike in the US dollar and yields triggered a sharp intraday reversal, with XAU/USD sliding from the $4470 area toward $4,300.

From a swing perspective, the short-term structure now favours a bearish continuation rather than an immediate recovery. A possible scenario involves a short-term swing short on gold, targeting a move toward the $4,200–$4,250 area as the market digests higher yields and a stronger dollar. A softer-than-expected CPI on Wednesday would likely challenge this setup.

NAS100 (Nasdaq)

The Nasdaq recorded the most visible damage on Friday, but sharp selloffs for techs create short-term mean-reversion opportunities, especially in the context of a strong uptrend.

A possible scenario for the week ahead is a pullback buy on Tuesday–Wednesday, assuming Wednesday does not bring a follow-through CPI surprise. The 29000 area on the USTEC may act as an initial support zone where responsive buying could emerge. The stabilisation in bond yields and a pause in the dollar rally would help it to recover.

The risk to this scenario is a hotter CPI reading that pushes Fed hike odds above 60% and triggers a second leg lower in tech. The FOMC meeting on June 16–17 remains the larger catalyst; the Tue–Wed window is best framed as a short-term swing rather than a structural trend reversal.

Author

Stanislav Bernuhov

Common Sense Trading

I'm an individual trader since 2004 and a trading coach since 2010.