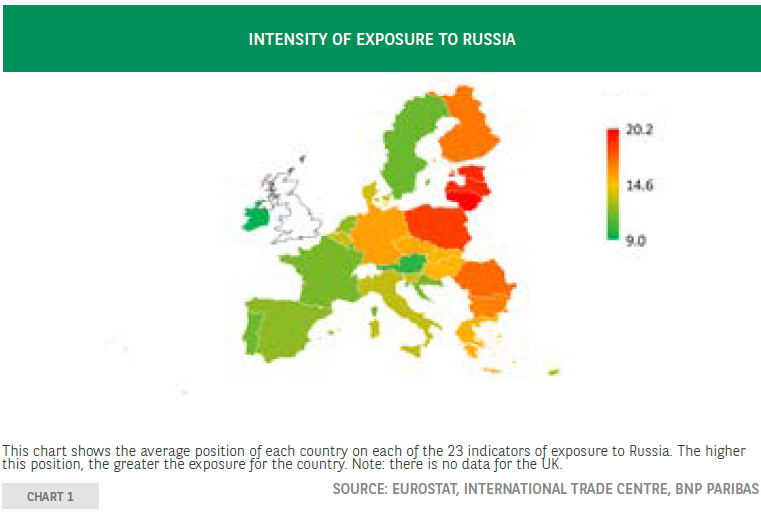

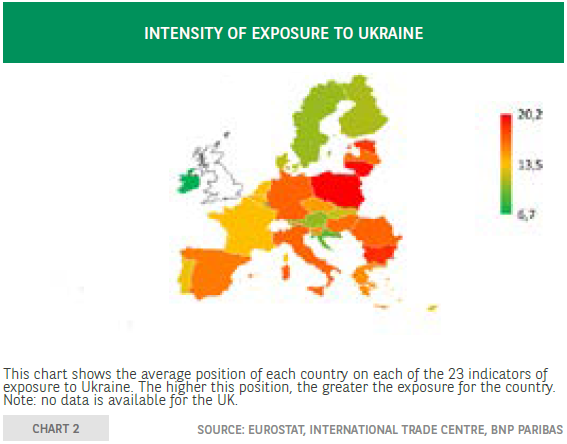

A heatmap of the dependence of European countries on Russian and Ukrainian imports

In this article, we will examine the links between Russia, Ukraine and various European countries in order to evaluate the latter’s exposure to the economic repercussions of Russia’s military offensive in Ukraine since 24 February. To do so, we look at imports of goods from Russia and Ukraine and the weight of energy and food components in the consumer price index1. The first series of indicators on imports gives us an assessment of the direct trade exposure of European countries, particularly when it comes to energy and food products, which are widely imported from Russia and Ukraine. The second series, examining the weight of energy and food in consumer spending, offers insight into the potential inflationary effects from the price shocks on the global commodities markets, which the war has amplified.

By presenting these indicators in the form of a heatmap, we can easily compare the level of exposure to Russia and Ukraine of all European countries. Where the data is available, we have also included the US, UK and China. Some indicators are broken down into sub-components to refine the comparison. For the six categories of trade in goods2, we distinguish between (i) the share of a given product in total imports from Russia or Ukraine and (ii) the share of a country’s total imports of a given product which comes from Russia or Ukraine. Linking these two variables allows us, for example, to analyse the weight of energy in trade between Russia and European countries: in 2019, 75% of EU imports from Russia were energy products, whilst 19% of total EU energy imports came from Russia.

Within the table we also break down the “energy products” line by identifying the energy mix: the share of gross domestic energy consumption contributed by each of the three main fossil fuel types–natural gas, oil and coal. We also show the share of each fuel type imported by a country and the share that comes from Russia. These two complementary measures allow us to compare the dependence on imports of a specific energy source and its significance for the energy mix of a given country. A country that is both a heavy gas user and a big customer of Russian gas will be significantly more exposed than others. This is the case for Latvia and Slovakia, where gas makes up more than a quarter of the energy mix and all of it is imported from Russia. Conversely, in some countries, including Austria, Denmark and Croatia, gas makes up a non-negligible share of the energy mix, but it is not imported from Russia3.

We carried out a similar analysis for Ukraine. Unlike Russia, which is a major supplier of energy products, Ukraine mainly supplies the EU with agricultural and food products, which represented nearly one third of the EU’s imports from Ukraine in 2019. We look at three major groups of agricultural products imported by the EU from Ukraine: cereals (corn, wheat, barley, oats, etc.), grains (soy, peanuts, rapeseed, sunflower, etc.), and animal and vegetable proteins. For these three product groups, we distinguish between (i) the share of a given product in total imports from Ukraine and (ii) the share of a country’s total imports of the product which comes from Ukraine.

With regards to the weight of energy and food in the consumer price index – indicative of the inflationary impact – Romanian, Latvian, Slovak, Bulgarian, Hungarian and Lithuanian households’ purchasing power is the most exposed (30% of consumption goes on these basic items).

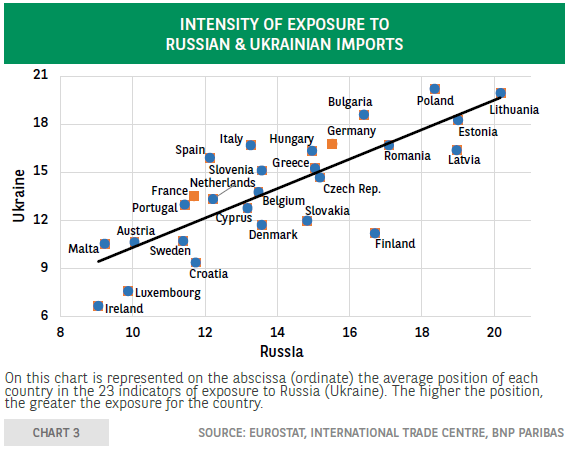

To establish a final ranking of the level of exposure of EU member states to Russia and Ukraine, we calculated an average of the positions for a given country for each of the 23 variables studied. The higher up the ranking a country is, the more dependent it is on Russia or Ukraine. This composite indicator confirms the significant exposure of countries close to Russia and Ukraine (Lithuania, Latvia, Estonia, Bulgaria, Finland, Poland [see charts 1 and 2]). It is also important to highlight the double exposure of the Baltic States to both Russia and Ukraine: a country heavily dependent on Russia is also dependent on Ukraine (see chart 3). Western European countries have less exposure, although there are significant differences, with Germany and Italy being more dependent on Russian gas than France, Spain or Portugal.

The exposure of European countries to Russia and Ukraine results primarily from their imports of Russian energy supplies and Ukrainian food and agricultural products. European countries’ dependence on Russian gas, coal and oil contributes significantly to the EU’s trade deficit with Russia (EUR49 billion in 2019). European countries are exposed and penalized, on the one hand, by the rise in prices of these products (caused by the conflict which is a source of additional inflation) and, on the other hand, by the slowdown in trade and the risk of supply disruption on primary products critical to domestic production. It remains to be seen how much growth will be affected by these issues.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.