A bit of a gloomy start to April – Coronavirus economic damage lays bare

Global stocks got off to a soggy start in April as economic damage wrought by the coronavirus was laid bare and investors felt there was not yet enough to show the virus was at or near its peak in Europe or the US. Donald Trump reflected the mood as he warned of weeks of pain still ahead, a stark change from his rather casual approach thus far. He also called for another $2tn for infrastructure spending. A bit of a gloomy start to April, like a sharp frost killing off the buds that appeared too soon.

Economic surveys are not surprisingly pointing to sharp contraction in activity because of the coronavirus. The Bank of Japan’s Tankan survey showed sentiment among the country’s large manufacturers soured in the Jan-Mar quarter, plunging from zero to –8, a 7-year low. South Korean factory activity declined at its fastest pace in 11 years in March.

European final PMI readings highlight declining activity, but the real damage will be done in April. Italy’s March manufacturing PMI fell to 40.3 vs 40.5 expected, the lowest level since 2009. It’s bad, a substantial drop. The output index in particular highlights the damage being done – down to 27.8 from 46.9 in Feb. To be honest it could be even worse. Spain’s final PMI reading for manufacturing slipped to 45.7, vs 44.0 expected. France printed 43.2 vs 42.9 expected, while Germany came in on the nose at 45.4.

Asian equities lead the way lower overnight. Tokyo finished –4.5%, while Hong Kong was more than 2.5% lower. US stocks yesterday finished on a weak footing with a decline into the close leaving the Dow nursing its worst quarterly loss since – no surprise – 1987. Only Microsoft finished the quarter higher, and only by a whisker.

Today, European equity markets opened weaker with declines of more than 3% registered in London and Frankfurt. HSBC, AstraZeneca, Diageo and BP were the biggest drags on the FTSE 100 this morning. The 5400 is looking like the defensive line near term and bulls will need to defend this. If this goes we have a 5330 as the last line. 5700 offers the near-term resistance, breakout potentially north of 5800.

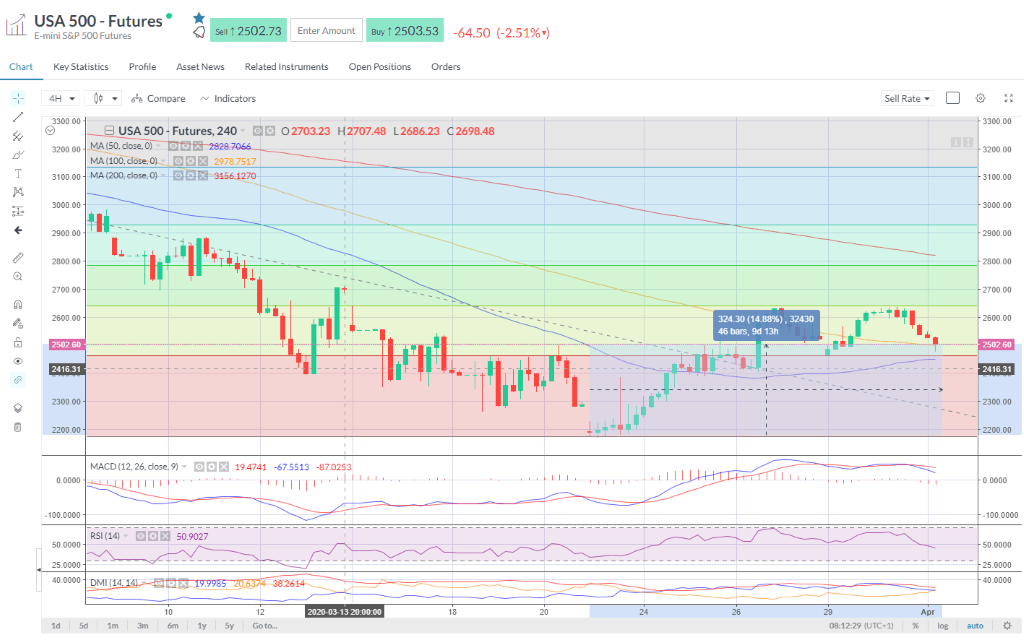

US futures are pointing to a soft start on Wall Street. E-minis didn’t retest the Sunday night lows with the 2480 holding. Near term resistance at 2640, the 38.2% retracement. Despite the pullback, we’re still 15% off the lows. Today’s ADP report in the US will be watched closely after that weekly jobless number last week hit 3.3m. The –150k expected looks a touch light.

Oil remains on its knees despite Trump calling Putin to try to stop the price rout. WTI has faded back to $20. WTI fell 67% in the first three months of 2020, its worst quarter on record. Trump’s efforts to sweet talk Putin may offer some hope of a way out of the supply war raging with OPEC, but it won’t do anything to boost demand, which could fall by around 20% over the next few weeks. Oil inventories later today expected to show a build of around 4m barrels.

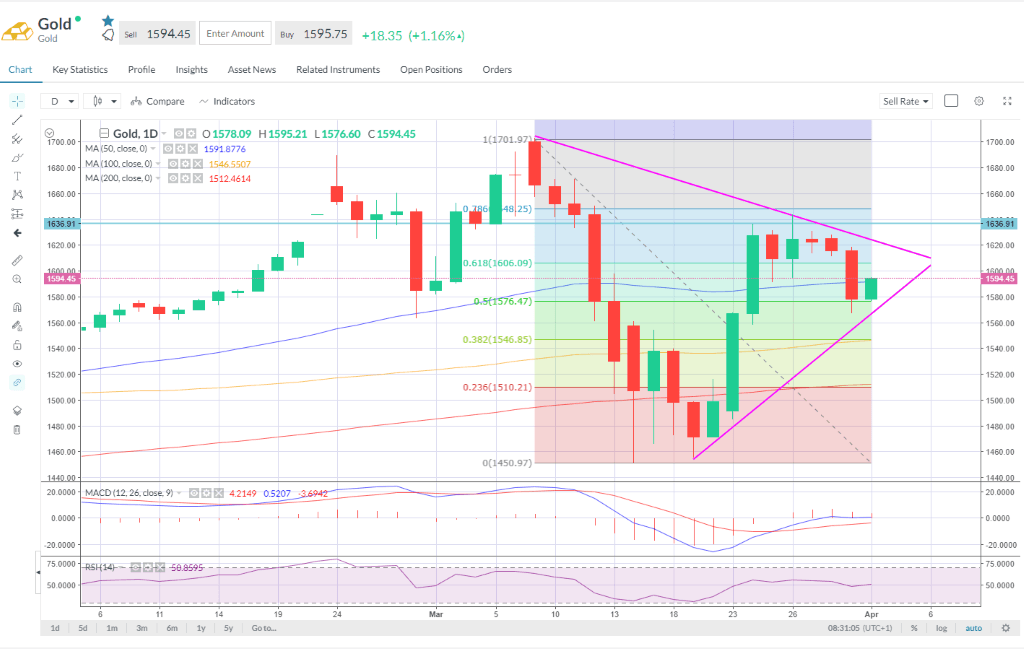

Gold has come back after weak session yesterday to trade around the 50-day SMA after the 50% retracement offered support.

Equities

UK banks were down after they acquiesced to the Bank of England’s arm-twisting to scrap dividends and buybacks. Lloyds, Barclays, HSBC, RBS, Standard Chartered and Santander all announced last night that they would cancel last year’s planned pay outs and not pay any dividends this year. Shares were lower on the open but ultimately shareholder returns are not the main priority right now. Barclays says today that Stoxx 600 dividends will decline by 40% this year. Shareholders are at the back of the queue.

Author

Neil Wilson

Markets.com

Neil is the chief market analyst for Markets.com, covering a broad range of topics across FX, equities and commodities. He joined in 2018 after two years working as senior market analyst for ETX Capital.