Fed Minutes to offer clues on Warsh's Fed debut

- The FOMC Minutes are expected to show further insight about the first Federal Reserve meeting with Kevin Warsh as chairman.

- The Fed is likely to provide a reduced version of the minutes amid Warsh’s reluctance to provide forward guidance.

- Investors will be attentive to growth and inflation expectations to assess the bank’s policy plans.

The United States (US) Federal Reserve (Fed) will release the Minutes of the June 16-17 Federal Open Market Committee (FOMC) meeting on Wednesday at 18:00 GMT. The Minutes should shed more light on the Fed’s hawkish hold delivered at Kevin Warsh’s first meeting as Fed Chair. Even so, doubts remain about how much the minutes will reveal, given Warsh's refusal to provide forward guidance.

The US central bank left the Fed Funds rate unchanged in the 3.50%-3.75% range, as widely expected, although the statement’s language showed a hawkish tilt that surprised markets and provided some support to the US Dollar (USD).

The committee approved the decision unanimously, putting an end to market speculation about the divergences within the governing council. Beyond that, the statement highlighted resilient activity and above-target inflation, adding to the case for interest rate hikes in the near term.

Kevin Warsh and his unexpected hawkish edge

The Fed met expectations in June and left its benchmark interest rate on hold for the sixth consecutive time, with the new chairman’s hand evident in the reduced monetary policy statement. The main takeaway of June’s meeting, however, was Kevin Warsh’s willingness to remove forward guidance, in clear contrast to his predecessor, Jerome Powell’s style, to allow the central bank further flexibility in setting monetary policy.

Warsh, however, was swift to tackle investors’ concerns about the central bank’s independence, showing an “unambiguous” commitment to deliver price stability, which the market took as a hawkish signal.

The bank’s statement also confirmed Warsh’s plans to implement radical changes in key areas of the central bank, including communication, data sources, and the framework of the central bank's inflation studies, which might also alter the bank’s monetary policy stance in the medium term.

As an immediate consequence of the new house style, the bank is expected to deliver a slimmer, less informative version of the Minutes with no clear hints about the bank’s rate path beyond the economic and inflation outlook.

With this in mind, investors will cautiously analyse the Minutes against the framework of last week’s disappointing Nonfarm Payrolls (NFP) report. June’s Payrolls showed a sharp slowdown in net employment creation, at 57K against expectations of a 110K increase, following three months of strong data, which prompted investors to push back hopes of Fed rate hikes.

Beyond that, concerns about inflation have eased since last month’s meeting. The latest US inflation figures remain well above the 2% target, but the easing tensions in the Middle East have brought Crude Oil prices back to pre-war levels. This is likely to cool price pressures over the coming months, and might grant Warsh with valuable leeway to postpone rate hikes.

When will FOMC Minutes be released and how could they affect the US Dollar?

The FOMC will release the Minutes of the June 16-17 policy meeting at 18:00 GMT on Wednesday.

Investors’ bets on Fed rate hikes have receded from the highs witnessed before last week’s NFP report, but money markets are still pricing at least a 25-basis-point rate hike over the next six months, which keeps the US Dollar buoyed.

The CME Group’s FedWatch tool still shows a 58% chance of a rate hike in September and nearly an 80% chance that the bank will tighten its monetary policy before the year-end. In this context, a clear message from the bank to contain inflationary pressures might reassure Fed tightening bets and provide a fresh boost to the US Dollar.

Downside risks from the US Dollar, in this case, would come from comments that play down the risk of second-round effects on inflation and link current higher prices to the energy shock.

USD moves, in any case, are likely to be limited, as recent developments in the Middle East and last week’s labour figures have altered the scenario, and investors are likely to await further US economic releases to better assess the Fed’s rate hike calendar.

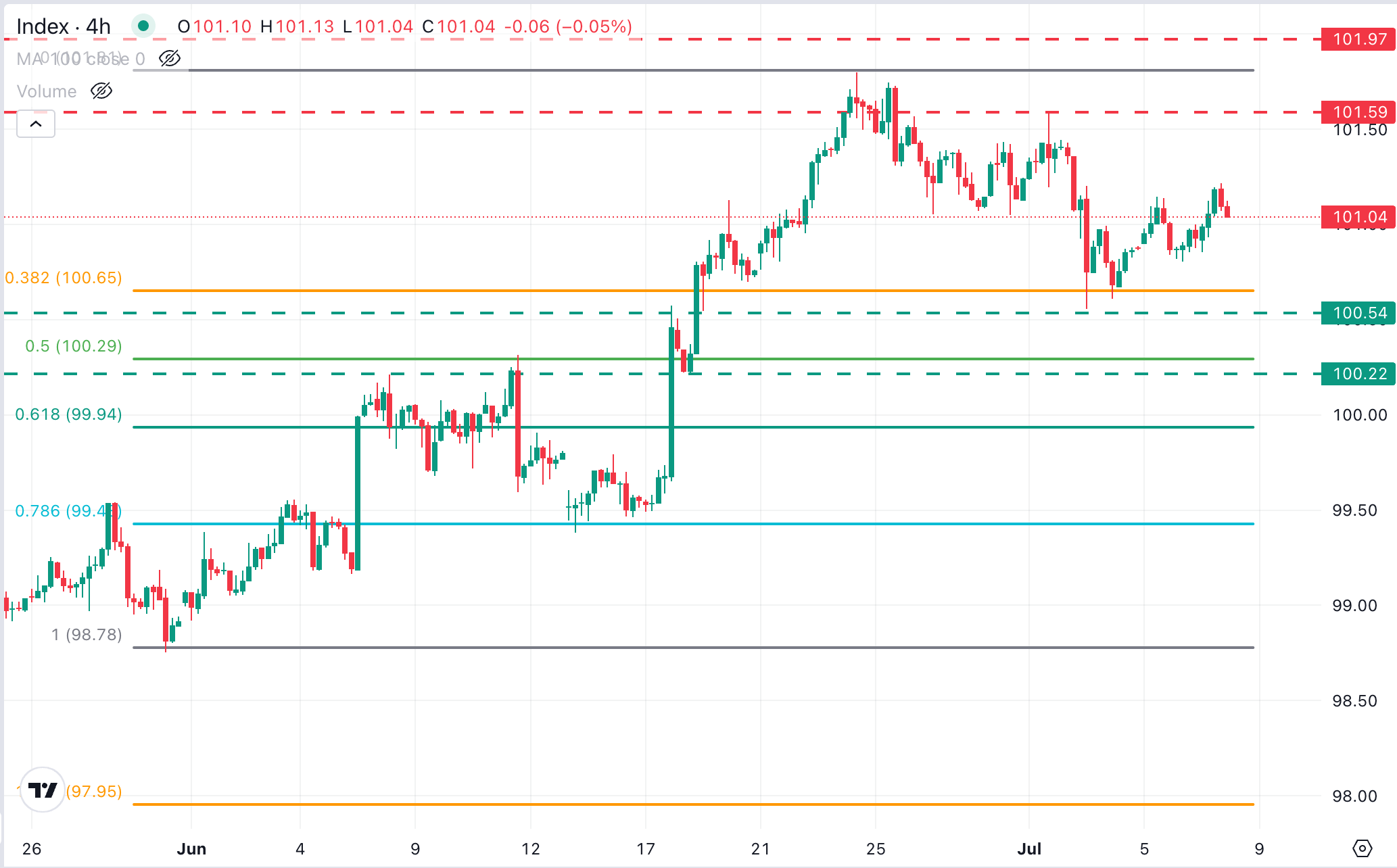

The US Dollar Index (DXY) has been wavering on both sides of the 101.00 level so far this week, trading within a corrective channel from last week’s highs at the 101.80 area. Momentum indicators highlight a mixed bias, with the Relative Strength Index (14) just below 50 and the Moving Average Convergence Divergence (MACD) near zero hinting at a lack of clear bias, although the broader trend remains bullish.

Immediate resistance emerges at the mid-range of the 101.00s, which held bulls in early July, closing their path towards the 2026 peak of 101.80. On the downside, bears would have to breach the area between the 38.2% Fibonacci retracement of June’s rally and the July 2 low, in the 100.50-100-60 area, to confirm a deeper correction, aiming for the June 11 high around 100.30. Further down, the 78.6% Fibonacci retracement meets the June 15 low, just below 99.40.

(The technical analysis of this story was written with the help of an AI tool.)

US Dollar FAQs

The US Dollar (USD) is the official currency of the United States of America, and the ‘de facto’ currency of a significant number of other countries where it is found in circulation alongside local notes. It is the most heavily traded currency in the world, accounting for over 88% of all global foreign exchange turnover, or an average of $6.6 trillion in transactions per day, according to data from 2022. Following the second world war, the USD took over from the British Pound as the world’s reserve currency. For most of its history, the US Dollar was backed by Gold, until the Bretton Woods Agreement in 1971 when the Gold Standard went away.

The most important single factor impacting on the value of the US Dollar is monetary policy, which is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability (control inflation) and foster full employment. Its primary tool to achieve these two goals is by adjusting interest rates. When prices are rising too quickly and inflation is above the Fed’s 2% target, the Fed will raise rates, which helps the USD value. When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates, which weighs on the Greenback.

In extreme situations, the Federal Reserve can also print more Dollars and enact quantitative easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system. It is a non-standard policy measure used when credit has dried up because banks will not lend to each other (out of the fear of counterparty default). It is a last resort when simply lowering interest rates is unlikely to achieve the necessary result. It was the Fed’s weapon of choice to combat the credit crunch that occurred during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy US government bonds predominantly from financial institutions. QE usually leads to a weaker US Dollar.

Quantitative tightening (QT) is the reverse process whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing in new purchases. It is usually positive for the US Dollar.

Economic Indicator

Nonfarm Payrolls

The Nonfarm Payrolls release presents the number of new jobs created in the US during the previous month in all non-agricultural businesses; it is released by the US Bureau of Labor Statistics (BLS). The monthly changes in payrolls can be extremely volatile. The number is also subject to strong reviews, which can also trigger volatility in the Forex board. Generally speaking, a high reading is seen as bullish for the US Dollar (USD), while a low reading is seen as bearish, although previous months' reviews and the Unemployment Rate are as relevant as the headline figure. The market's reaction, therefore, depends on how the market assesses all the data contained in the BLS report as a whole.

Read more.Last release: Thu Jul 02, 2026 12:30

Frequency: Monthly

Actual: 57K

Consensus: 110K

Previous: 172K

Source: US Bureau of Labor Statistics

America’s monthly jobs report is considered the most important economic indicator for forex traders. Released on the first Friday following the reported month, the change in the number of positions is closely correlated with the overall performance of the economy and is monitored by policymakers. Full employment is one of the Federal Reserve’s mandates and it considers developments in the labor market when setting its policies, thus impacting currencies. Despite several leading indicators shaping estimates, Nonfarm Payrolls tend to surprise markets and trigger substantial volatility. Actual figures beating the consensus tend to be USD bullish.

Author

FXStreet Team

FXStreet

Composed of a group of economic journalists and FX experts, the FXStreet content team produces and oversees all content published on FXStreet. It provides a purely journalistic approach to the Forex market.