2.25% rates and a wide discount: Why the Loonie isn't an Oil trade

The Loonie is trading at a 12-month low against the Greenback, and Oil is the only story the desk wants to tell about it. That story is wrong, or at least it answers the wrong question. Crude has unwound its war premium, the Canadian Dollar has slid, and the tidy read is that one dragged the other. The Loonie stopped trading the barrel months ago.

What has pulled it to the lows is the rate gap and a US Dollar pinned near 13-month highs, and the one corner of the Oil complex traders keep reaching for, the crack spread, is the worst tell of all for Canada.

The rally the Loonie sat out

Measure the relationship over June alone, and it looks textbook. West Texas Intermediate (WTI) has slid to a three-month low near $73 as the US-Iran ceasefire roadmap reopened the Strait of Hormuz and let blocked barrels back onto the water, and the Loonie softened in step. Pull the lens back to the turn of the year and the textbook tears. The Canadian Dollar was at its strongest of 2026 in late January, near 1.3500, with crude still cheap in the low $60s. Then the war premium did its work.

WTI tore from the low $70s into the $90s through February and March, Brent ran past $110, and the Loonie did not rally with it. The pair spent the entire spike rangebound and was sitting near a local high around 1.4000 in April, with crude close to its peak. A currency that firms on cheap Oil and sags on dear Oil is not trading Oil. The June leg lower is a coincidence, the Dollar and crude happening to point the same way. The months the Loonie sat out the rally are the signal.

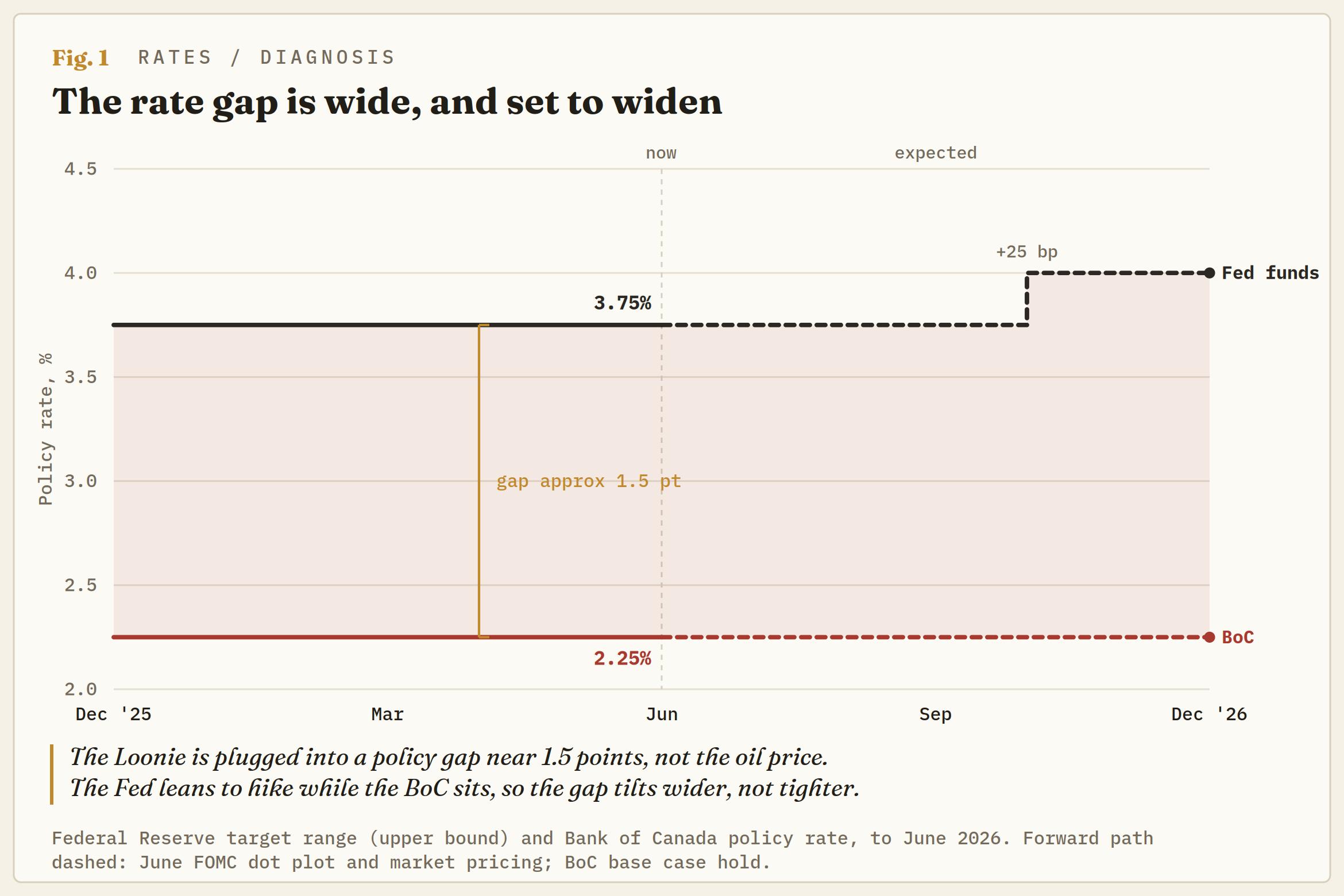

It's the rate gap, not the barrel

What the Loonie has actually been plugged into is the policy spread, and it has run the wrong way for Canada. The Federal Reserve (Fed) left its target range unchanged at its June meeting, but the projections leaned hawkish, with roughly half of the Federal Open Market Committee (FOMC) now pencilling in at least one more hike this year, and the US Dollar index has climbed to a 13-month high behind it. The Bank of Canada (BoC) has sat at 2.25%. The market leans towards a 25bp BoC hike in December, but that is the tell, not the rescue.

It would be a hike forced by energy leaking into inflation rather than earned by an economy that can carry it, delivered into soft growth and a wobbling labour market. A reluctant hike to defend the currency against imported inflation is a different animal from a confident one, and the tape knows it. The Fed leans hawkish from a higher level, the BoC inches from a lower one, the gap is wide, and the Loonie is wearing it.

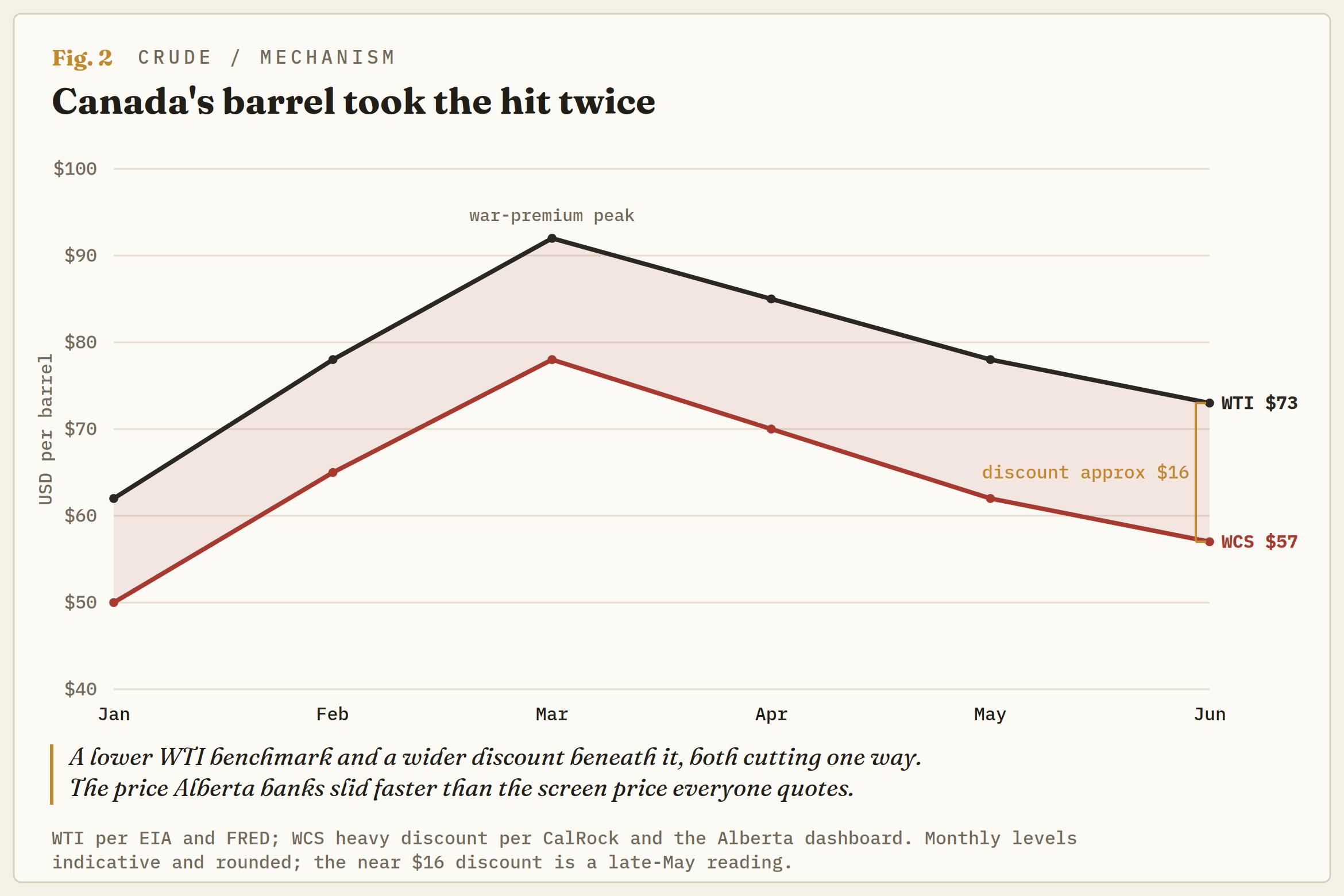

Canada sells the wrong cut of the barrel

Here is where Oil actually bites, and not the way the bulls hope. Canada does not sell the barrel; it sells the cheapest, heaviest cut of it. Western Canadian Select (WCS), the oil-sands benchmark, prices at a discount to WTI for quality and pipeline distance, and that discount widened back out to around $16 a barrel through the conflict, wider than its post-pipeline norm.

So Canadian crude took the hit twice over, from a lower WTI benchmark and a wider discount sitting beneath it. The price an Alberta producer actually banks fell by more than the screen price everyone quotes. Traders who watch WTI and infer the Loonie are already watching the wrong barrel; the one Canada ships has done worse.

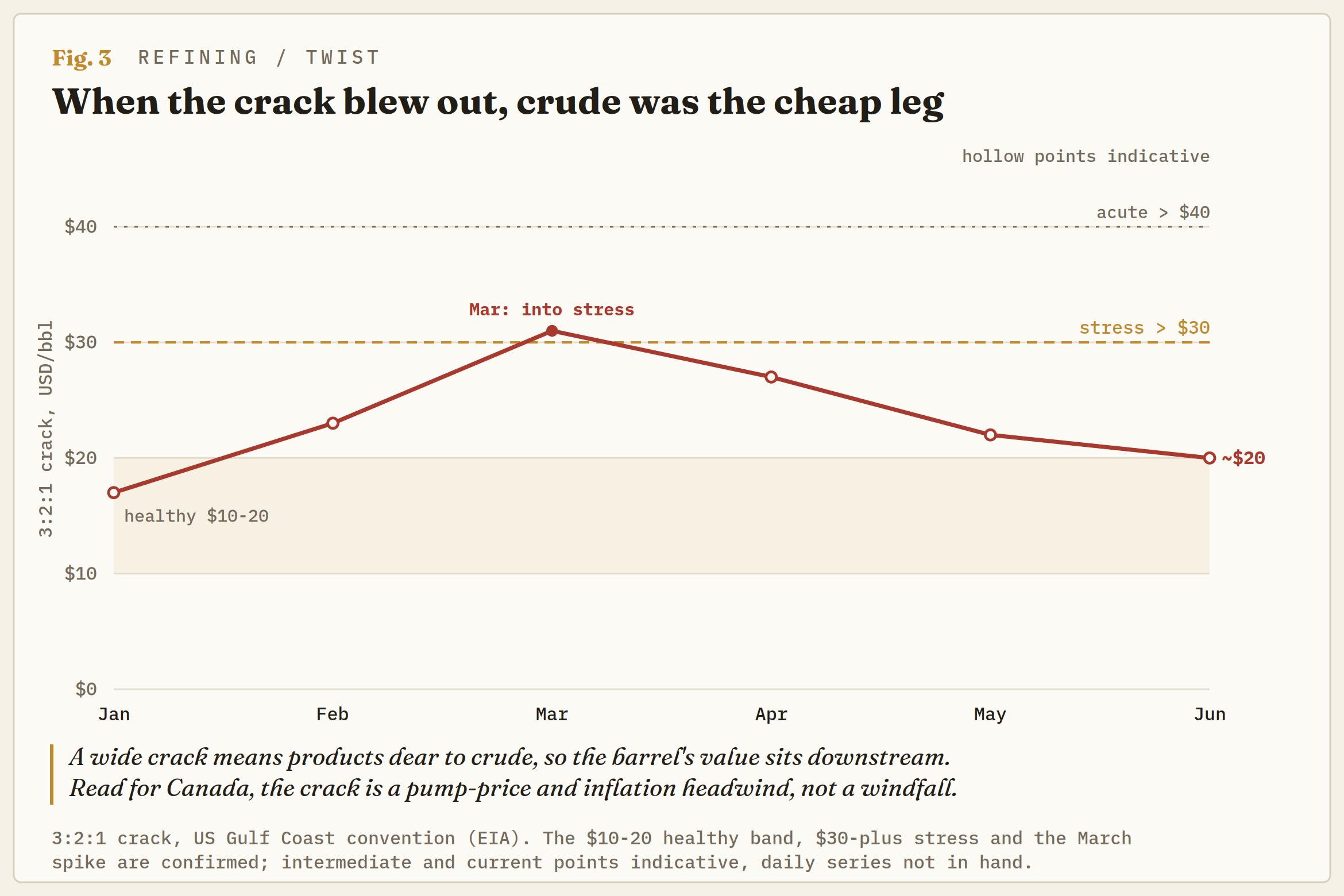

The crack spread is the wrong tell

Which brings us to the crack spread, the metric the question keeps circling. The crack is the refiner's cut, the gap between the products, gasoline and distillate, and the crude fed in to make them. A wide crack is, by definition, products dear relative to crude, which means the value of the barrel is sitting downstream with the refineries, not upstream with the crude Canada sells. That is the opposite of a Canadian boon.

It is also exactly what happened in March, when the 3:2:1 crack tore out past $30, a reading that flags refinery stress, even as the war raged, because Hormuz tightened refined products as hard as crude.

The Oil headline screamed bullish; the crack was quietly flagging crude, Canada's leg, as the cheaper end of the barrel. The spread has since cooled as crude round-tripped lower and US pump prices slipped back below $4. The only channel by which the crack reliably reaches Canada runs through cost, not revenue.

Fatter margins mean firmer pump prices, which feed Canadian inflation, which lands back on that same reluctant BoC. Read properly, the crack is a Loonie headwind dressed as Oil-complex strength, a stagflation tax, not a terms-of-trade gift.

The lean, and what would change it

On the chart, the Loonie sits with the bears. USD/CAD has broken to a fresh 12-month high, clearing the November peak around 1.4150 and turning it into the first shelf of support, with the uptrend off the May low near 1.3550 intact. The lean is for more, but not at any price. The Stochastic RSI is pinned near the top of its range, so chasing 1.4200 is poor risk-reward; better entries are on dips into support.

Overhead, 1.4250 is the immediate marker, then 1.4300. Below, 1.4150 is the line the bulls want to hold; 1.4000 is the bigger one, the breakout shelf and the round number, and a daily close back beneath it neutralises the move. Lose 1.3900, and the breakout has failed.

The trigger that flips the lean is not the Oil price. A crude bounce on its own, with the rate gap still wide and the Dollar still bid, is a fade for anyone long the Loonie. What would actually turn it is the policy spread closing, a dovish Fed pivot or a BoC hawkish enough to convince the tape that December is conviction rather than damage control. Until one of those lands, the Loonie is a rates-and-Dollar story, and the barrel is just the costume.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.