Wake Up Wall Street (SPY) (QQQ): Equities slump in metaverse and real world

Here is what you need to know on Thursday, February 3:

Equity markets are down in both the metaverse and real world this morning as Facebook (aka Meta Platforms) pumped a lot of cash into building out its metaverse investment. The shares dropped an alarming 23% after missing earnings on Wednesday evening. We had warned on this in our preview note yesterday, and equity markets will now resume the bearish theme from earlier this year. A bounce spurred on by Apple and Google is now distant, and only Amazon (AMZN) can save us now.

Even then it is a big ask that would require a huge beat to put this bear back into hibernation. High growth names will get hammered again, and risk barometers are flashing again this morning. The combination of higher yields, Vix and dollar combined with FB will make for a tough end to the week.

The Bank of England did what was expected and hiked rates 25bps this morning. Sterling strengthened on the back of a surprising 5-4 vote with the four members looking for a 50bps tightening. This has seen yields pop again as other central banks will be watched for increasing hawkishness. The ECB as expected kept rates unchanged.

The dollar is higher after the ECB decision, while it is flat versus sterling after the BOE raises rates. Bitcoin is lower at $36,700, and gold is at $1,802. Oil is lower at $87.04.

European markets are lower: Eurostoxx -0.45, FTSE -0.1% and Dax -0.3%.

US futures are lower: S&P -1%, Dow -0.2% and NASDAQ -2%.

Wall Street (SPY) (QQQ) News

Bank of England raises rates by 25bps. 5-4 vote, four voters wanted a 50bps rise. Sterling strengthens.

ECB leaves rates unchanged.

Meta Platforms, aka Facebook, (FB) misses earnings, shares collapse over 20%.

Nokia (NOK) misses earnings.

Eli Lilly (LLY) beats on top and bottom lines.

Honeywell (HON): EPS beats, but revenue misses.

Merck (MRK) beats on top and bottom lines.

Novavax (NVAX) gets conditional all clear from UK for its covid vaccine.

Ralph Lauren (RL) beats on EPS and revenue.

Overstock.com (OSTK) makes Wedbush best ideas list.

Shell (SHEL) announces an increase in dividend and $8.5 billion buyback.

Spotify (SPOT) issues weak forecast, shares fall.

SNAP down 16% on Facebook read-across.

PINS also down 9%.

Humana (HUM) up on medicare rates proposal.

Amazon (AMZN) and Ford (F) report after the close.

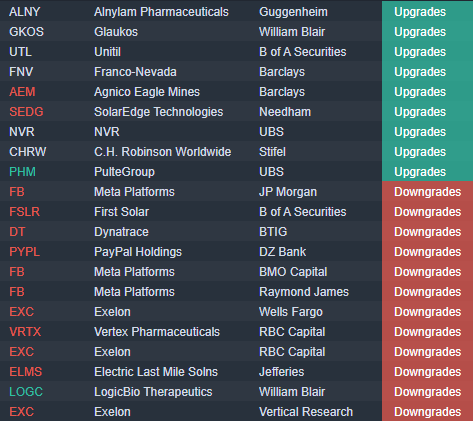

Upgrades and Downgrades

Source: Benzinga Pro

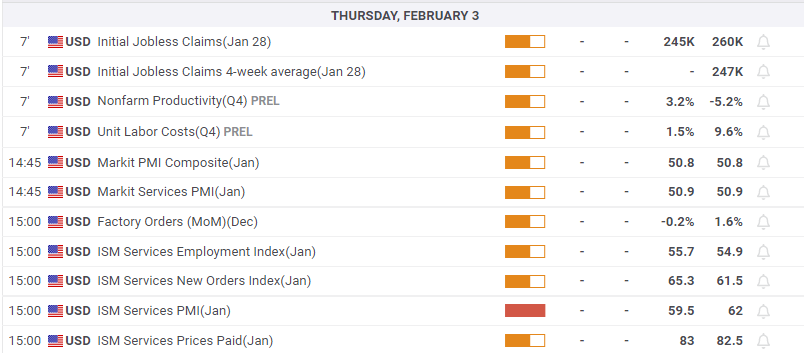

Economic releases

Like this article? Help us with some feedback by answering this survey:

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.