Tech supply chain daily: Beijing may put a firewall around its best AI models

- Beijing may be preparing to restrict access to its most advanced AI models, turning China’s low-cost model advantage from a commercial export weapon into a protected national asset.

- Near-term, that could ease fears that US enterprises will rapidly migrate toward cheaper Chinese LLMs, offering some breathing room to pressured frontier-AI valuations.

- The move would not solve the broader token-pricing problem. Capability convergence and falling costs still threaten to compress returns across the AI stack.

- The AI trade is becoming less about software alone and more about strategic control: chips, capital, data, energy, users and increasingly, national borders.

China’s AI firewall

The AI race is starting to look less like a software land grab and more like an arms market where both sides have suddenly realised they may be exporting too much of the ammunition.

For much of the past year, the anxiety ran one way. US frontier-model providers warned that Chinese developers were distilling, reverse-engineering or otherwise catching up too quickly. Whatever the exact mechanics, the commercial result was clear enough: Chinese models were improving rapidly, while their costs remained far below those of their US rivals.

That mattered because the real threat to US frontier AI was never that Chinese models had to be better. They only had to be good enough.

For coding, customer support, workflow automation and internal enterprise tasks, a cheaper model with roughly comparable capability could put serious pressure on token pricing and revenue expectations. That was the unpleasant arithmetic behind the recent wobble in parts of the AI supplier complex: intelligence was beginning to look less scarce, and scarcity is where the premium multiples live.

Reuters now reports that Beijing may be considering restrictions on overseas access to China’s most advanced AI models, including future releases. Alibaba, ByteDance and Z.ai were reportedly among companies involved in recent discussions with Chinese authorities. EXCLUSIVE Beijing is looking at curbing overseas access to China’s top AI models, sources say.

The details remain unsettled, but the direction is important. China may be moving toward its own version of AI export controls, treating frontier models less like commercial software and more like strategic infrastructure.

That would be a meaningful shift. China’s open-model ecosystem has been one of its strongest competitive tools. Alibaba’s Qwen, ByteDance’s Doubao and Z.ai’s GLM models have gained global traction because they combine increasingly credible capability with much lower costs. They were not just competing with US labs on technology. They were competing on the one thing every enterprise buyer understands immediately: price.

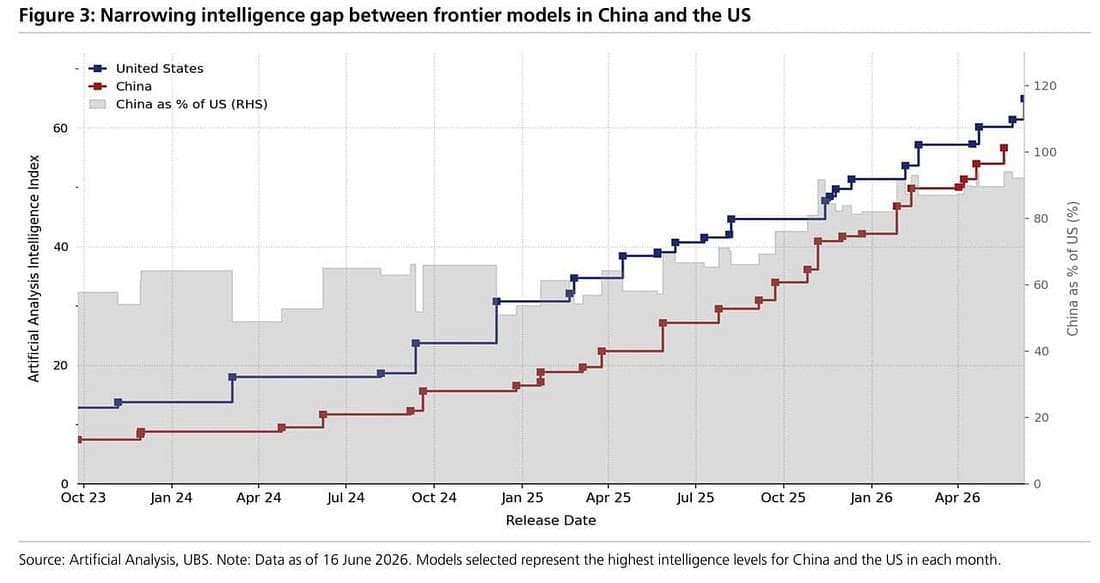

China’s frontier-model capability gap with the US has narrowed rapidly, turning low-cost Chinese AI into a more credible enterprise alternative. Source: Artificial Analysis, UBS; data as of 16 June 2026.

If Beijing restricts overseas access to its best models, that price-disruption threat becomes less immediate for US frontier-model providers.

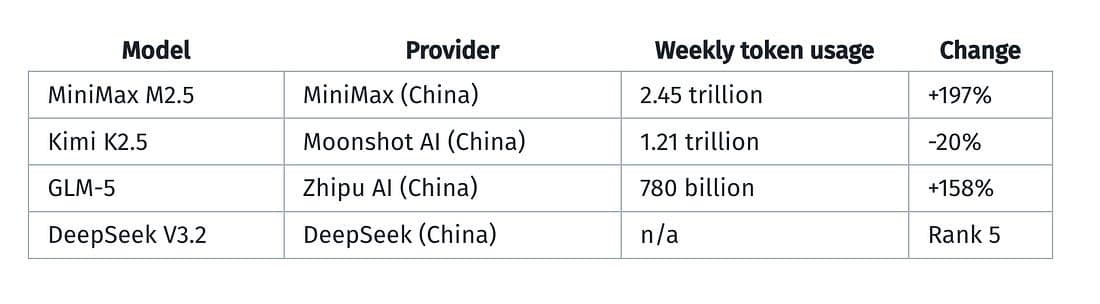

Chinese AI models have rapidly gained usage share on OpenRouter in 2026, underlining that lower-cost alternatives are already gaining real global traction.

For now, that could be a modest reprieve for the US AI complex. The market has been worrying that falling token costs and cheaper Chinese alternatives would compress the economics of US model providers, forcing them into a race to the bottom before they had fully monetised the enormous capital investment behind their infrastructure.

A Chinese firewall around its best models would not eliminate that risk. Token pricing is still falling, model capability is still converging, and open-source competition is not disappearing. But it could slow one of the most obvious channels through which US enterprise customers were beginning to test cheaper alternatives.

There is a trade-off for Beijing, however.

China’s AI firms are trying to build global relevance, developer ecosystems and commercial scale. Restricting foreign access may protect strategic capability, but it also risks limiting revenue, user feedback, developer adoption and the sort of global distribution that turns a strong model into a durable platform.

That is the paradox. China may protect its laboratory while narrowing the commercial runway outside it.

The larger message is that AI is becoming less of a pure software story and more of a strategic asset class. The next phase of the boom may not be decided only by who has the best model, the cheapest token or the largest cluster.

It may increasingly be decided by who gets access.

SK Hynix shows the AI memory trade still has a bid

The AI trade has taken a few punches, but SK Hynix just showed there is still a long line outside the right door. The company’s planned $28 billion US listing is already multiple times oversubscribed ahead of Thursday pricing, with demand coming from global long-only funds and technology-focused investors.

That is the important signal. This is not just another foreign listing. It is a real-time auction for one of the key bottlenecks in the AI supply chain: high-bandwidth memory. Investors may be arguing about falling token prices, cheaper Chinese models and whether frontier AI margins can hold, but they are still willing to pay up for the hardware layer that keeps the whole machine running.

SK Hynix is marketing 177.9 million ADRs, with each ADR equal to one-tenth of a common share. Based on the Seoul closing price, the deal is worth about $28 billion, putting it on track to become the largest-ever US listing by a foreign company. Around 1,000 institutional investors reportedly joined the management call, which tells you this is not a sleepy cross-listing. It is a crowd trying to get closer to the memory engine of the AI boom.

The attraction is easy to understand. AI may be a software story on the surface, but underneath it is still a physical buildout. Data centres need accelerators. Accelerators need high-bandwidth memory. And SK Hynix sits in one of the narrowest lanes of that road. When everyone wants to move through the same bottleneck, the toll collector tends to get paid.

That does not make the trade risk-free. SK Hynix’s market value has more than tripled this year to more than $1 trillion, and the stock has already seen sharp swings. Memory remains cyclical, and crowded enthusiasm in a cyclical sector can turn quickly when pricing, inventories or capex assumptions shift.

There is also a technical twist. Limits on converting the Korea-listed shares into ADRs may restrict arbitrage, which could allow the US-listed ADRs to trade at a premium. That can create early scarcity value, but it can also turn the deal into a positioning magnet, where the price reflects not only fundamentals but who managed to get stock and who still needs to chase it.

The broader message is simple. The market may be questioning parts of the AI story, especially model pricing and software monetisation, but it is not yet walking away from the supply chain. In fact, the more investors worry about model margins, the more they seem to prefer the companies selling the picks, shovels and memory bandwidth.

SK Hynix is therefore less a clean victory lap for the AI trade than a useful distinction. Not every part of the boom deserves the same multiple.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.