SK Hynix's US IPO puts focus on memory stocks

- SK Hynix begins trading on the NASDAQ on Friday.

- SK Hynix reaps $26.5 billion after selling nearly 178 million shares at $149.

- Analysts expect a rally as the secondary listing was oversubscribed at least seven times.

- Competitors Micron and Sandisk opened lower on Friday.

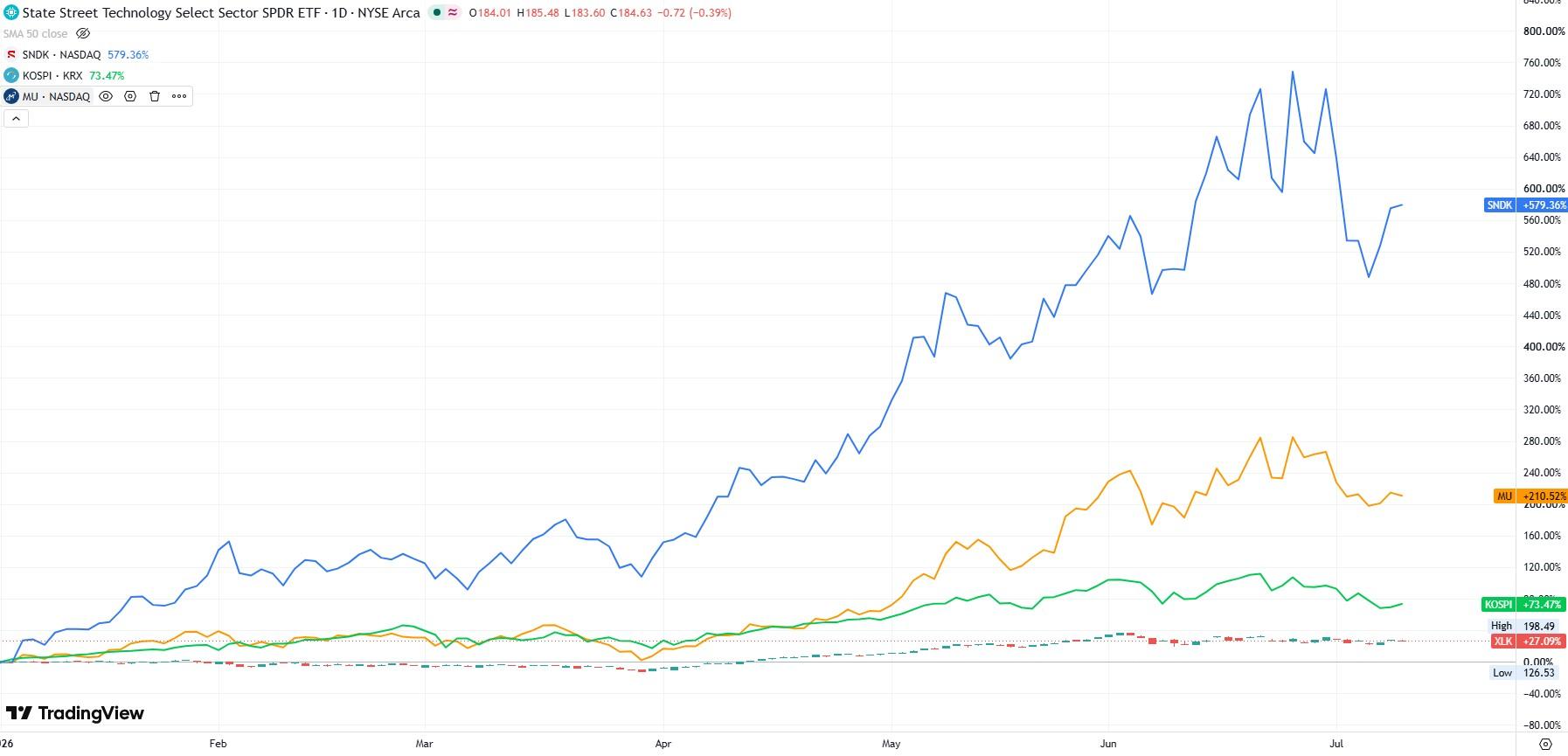

There have been two competing theories on how Friday's SK Hynix US debut will affect the two leading US memory chip stocks, Sandisk (SNDK) and Micron (MU).

The first posits that investors will sell some of their holdings in the US companies in order to include the South Korean competitor. The second views the three as similar horses that should all benefit from the ongoing global memory shortage that has provided the sub-sector of the semiconductor industry with exploding margins and profits.

The first theory seems to be the leading contender on Friday as SK Hynix is set to begin trading under the ticker SKHY sometime during the regular session. Both Micron and Sandisk shed some weight in the early going on Friday.

The broader market is waxing and waning between positive and negative territory as the NASDAQ Composite and Dow Jones Industrial Average both search for direction.

SK Hynix prices US IPO

On Thursday, SK Hynix sold 177.9 million American Depositary Receipts (ADRs) for $149 apiece, raising $26.5 billion in the process. The secondary listing was oversubscribed by between seven and eight times over, depending on who you ask. And that is why leading market observers are expecting an immediate rally.

SK Hynix is a leading supplier of high-bandwidth memory (HBM) to Nvidia (NVDA) and other players in the AI data center buildout. SKHY holds approximately 32% of the dynamic random access memory (DRAM) market and around 57% of the HBM market.

"This could mean that the ADR trades at a premium to the local shares, but more importantly it could help re-rate the Korean-listed SK Hynix shares, which are currently trading at a PE discount to Micron (MU), whereas we think SK Hynix should trade at least on par with Micron’s valuation," Sam Konrad, investment manager for Asia equity income at Jupiter Asset Management in Singapore, told Reuters.

Much of the funding acquired from the US listing will be used to break ground on two new fabs in its home country.

Author

Clay Webster

FXStreet

Clay Webster grew up in the US outside Buffalo, New York and Lancaster, Pennsylvania. He began investing after college following the 2008 financial crisis.