Samsung was priced for perfection — Then came the reality check

- Samsung’s numbers were exceptional; the selloff shows the market wanted exceptional plus another upside surprise.

- The key shift is from strong AI demand to whether AI demand can keep accelerating fast enough to justify current valuations.

- Watch Samsung’s full results for HBM guidance, capex discipline and any softening in conventional memory pricing.

- The biggest risk is not an AI collapse, but a market discovering that even the best cycle eventually stops getting better.

Samsung was priced for perfection

The first proper AI stress test may not have arrived with weak demand, a capex warning, or some sudden crack in the data-centre story. It may have arrived with Samsung posting an extraordinary quarter and the stock falling anyway.

Samsung’s preliminary second-quarter numbers were, on their face, spectacular. Operating income surged nineteen-fold to ₩89.4tn, above expectations, while revenue more than doubled to ₩171tn. AI memory demand remains ferocious, supply remains tight, and the major memory makers are enjoying margins that would have looked implausible only a few years ago.

Yet Samsung fell as much as 5% in Seoul.

That is the problem with a market priced for perfection. Good is no longer good enough. Even exceptional is not enough. Investors are not judging the last quarter; they are judging whether the next several quarters can still exceed an earnings curve that has already been pulled almost vertically higher.

Memory has become one of the central toll booths of the AI boom. First the market paid for GPUs, then for high-bandwidth memory, packaging, networking, power and cooling. Every bottleneck became a profit pool, and Samsung, SK Hynix and Micron found themselves sitting in the middle of one of the most profitable cycles the sector has ever seen.

But the market is beginning to ask a more difficult question: not whether demand is strong, but whether it can keep accelerating at the rate investors have already assumed.

That is why Samsung’s reaction matters. The quarter did not undermine the AI story. It exposed how demanding the AI story has become.

The broader chip complex had already started to wobble in the United States. There was no single obvious catalyst, which is often how crowded trades begin to lose their footing. The marginal buyer simply starts asking whether the upside is still worth paying for when every good outcome is already embedded in the price.

Meta’s recent pushback against the idea of endless AI spending has added to that unease. One company does not end a capital-spending cycle, but it can change the market’s framing. Investors have spent the past year treating hyperscaler capex as a one-way escalator. The question now is whether spending is still accelerating, or merely staying very high.

For a sector priced beyond perfection, that difference is enormous.

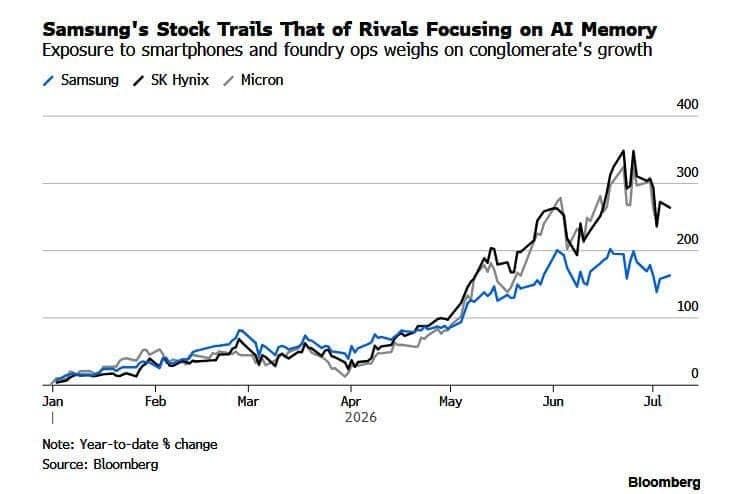

Samsung also has a more complicated equity story than SK Hynix. It is not a pure high-end memory trade. Its consumer electronics exposure and broader semiconductor base mean investors will want proof that the current memory boom can become a lasting increase in free cash flow rather than simply another powerful cyclical peak.

That puts the focus on the full results later this month: high-bandwidth memory progress, capex plans, conventional DRAM pricing, inventory trends and shareholder returns. The headline beat has already happened. The market now wants evidence that the profit machine can keep running at this speed.

The bull case remains clear. Memory shortages are still constraining AI expansion, suppliers are prioritising high-end products, and pricing power remains formidable. Counterpoint expects operating margins for the major memory names to run around 75% to 80% in the June quarter. South Korea is also treating the sector as a strategic national asset, with Samsung and SK Group planning huge capacity expansions.

But high margins do not just reward incumbents. They invite competition.

CXMT is still behind the Korean leaders in the most advanced memory products, but the pace of Chinese progress is becoming harder to ignore. It does not need to displace Samsung or SK Hynix in the highest-end AI products overnight. It only needs to make enough progress in conventional DRAM to loosen the supply discipline that has made this cycle so lucrative.

That is the longer-term shadow over the boom. Scarcity is profitable, but scarcity has a habit of financing the people trying to break it.

Samsung’s selloff does not mean the AI trade is over. It means the market has moved into its more dangerous phase. Earnings are still booming, margins are still exceptional, and demand is still real. But the price now demands that all of those things stay true, improve further, and continue for longer than investors have any right to expect.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.