Rotation or illusion? China rebounds while US leadership gets crowded

There is a question sitting under the current CHA50 vs. US500 setup: is China finally drawing capital on its own merits, or is this simply what happens when the U.S. trade becomes too full? The China vs. US stock market debate has sharpened because both sides now carry very different risks. China is no longer priced only as a disappointment story. The U.S. is no longer priced with much room for disappointment at all.

China’s rebound has real inputs

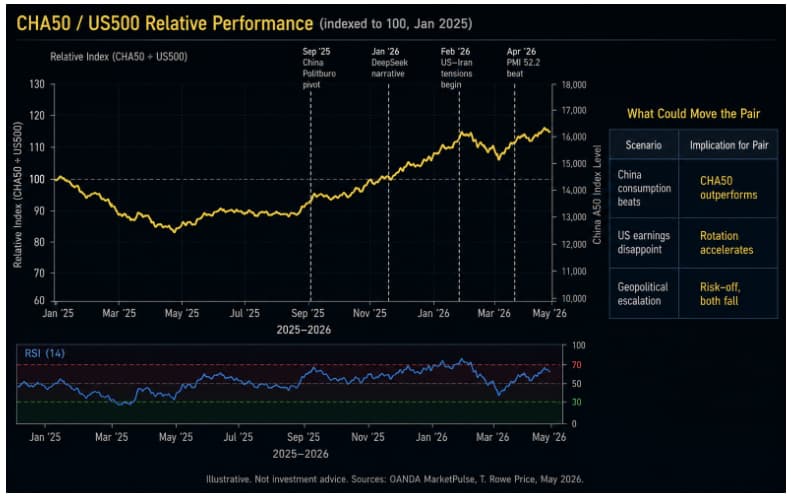

The China stock market rebound is not built on one headline. From late February to early May 2026, the China A50 gained about 7%, while MarketPulse noted a bullish breakout above a six-month range and targets near 16,100 to 16,340 if momentum holds. April data also helped. The private RatingDog manufacturing PMI rose to 52.2, the strongest reading since late 2020, helped by firmer production and new orders.

That gives the China A50 vs S&P 500 trade a clearer base than it had last year. Beijing has kept monetary policy “moderately loose” for 2026 and continued to push domestic demand as a central policy theme. Invesco’s China equities outlook also points to a more supportive rate environment and better earnings visibility as possible reasons global investors may take another look at Chinese shares.

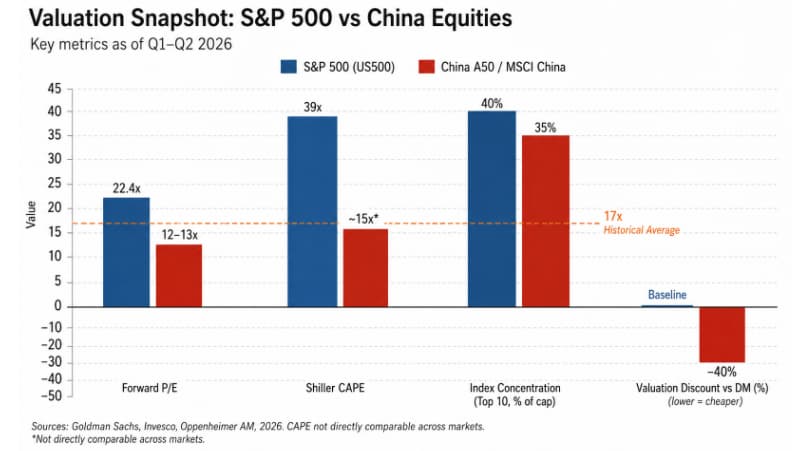

The US side looks expensive, not broken

The case against U.S. leadership is not that the S&P 500 is weak. It is that the bar has moved higher. The US market's overcrowded trade is visible in valuations, index concentration, and the dependence on a narrow group of mega-cap growth names. That does not automatically mean a crash. It does mean the market needs earnings to keep justifying the multiple.

This is where US equity valuations risk matters. When a market is priced for strong margins, AI-led productivity, and steady growth at the same time, small disappointments can travel quickly through the index. For investors using a CHA50/US500 comparison, the question is less about absolute quality and more about relative expectations. China still has problems. The U.S. has less tolerance for bad news.

Rotation, or just a cheaper place to hide?

The global capital rotation story is tempting because positioning has been so uneven. U.S. equities still dominate global benchmarks, while emerging markets remain lightly owned by comparison. T. Rowe Price has argued that emerging markets may be near an inflection point in global capital flows, especially after years of U.S. dominance.

That supports the emerging markets vs. US stocks argument, but it does not settle it. A cheaper market can rally because fundamentals are improving or because investors are tired of paying too much elsewhere. Those are not the same thing. The current global capital rotation trends look plausible, yet still fragile.

China’s policy bet

The strongest argument for the China side is policy. The China stimulus impact markets thesis rests on targeted support rather than a single dramatic rescue package. Beijing is trying to steady demand, defend industrial strength, and keep liquidity conditions loose enough to prevent another confidence slide.

The macro outlook of China's economy is still mixed. Manufacturing looks better, services improved in April, and EV leadership remains a real structural advantage. But the property drag has not disappeared, household confidence is still uneven, and exporters remain exposed to trade shocks. That is why investor sentiment for China stocks has improved without turning euphoric.

How traders should read the pair

For anyone looking to trade China vs. US equities, this is not a clean “China good, U.S. bad” setup. It is a relative trade between a crowded leader and a recovering laggard. The Versus Trade CHA50 US500 works best as a test of mean reversion: can Chinese equities keep closing the gap while U.S. equities pause, consolidate, or reprice?

A proper regional equity performance comparison also needs to separate technical strength from structural change. The China A50 breakout is constructive, but charts cannot prove that long-term capital has truly changed direction. They only show that buyers have started to act.

The risk still cuts both ways

The China rebound vs. US leadership trade carries obvious tail risks. U.S.-China friction can return quickly. The planned Trump – Xi meeting in Beijing on May 14–15 is a live catalyst, not a guaranteed relief event. A weak consumption print or renewed property stress could cool the China trade fast.

On the other side, the U.S. could keep winning if AI earnings broaden beyond the largest names and the Fed avoids a policy mistake. That would delay any serious rotation from the US to emerging markets.

For global diversification strategies, the balanced answer is simple: China now deserves attention again, but not blind trust. The emerging markets recovery outlook has improved because valuations, policy, and positioning have lined up better than they have in years. Whether that becomes a lasting rotation is still unproven.

For now, the pair sits between signal and illusion. That is exactly why it matters.

Author

Amir Razak

Versus Trade

Malaysian-born market analyst Amir Razak cuts through the noise every week, breaking down Versus Pairs and explaining what is really driving one asset ahead of another.