Early Q2 results reveal a highly robust earnings landscape

Here are the key points

The big banks have kicked off the Q2 earnings season with remarkable momentum. Both earnings and revenue growth rates—along with the percentage of companies beating expectations—are tracking significantly higher than in recent quarters. While we are still in the opening stages of the Q2 reporting cycle, these early results strongly reinforce the robust corporate earnings trend we've been seeing.

For the 34 S&P 500 companies that have reported Q2 results already, total earnings are up +55.3% from the same period last year on +18.8% higher revenues, with 91.2% beating EPS estimates and 82.4% beating revenue estimates.

The Q2 earnings and revenue growth rates have been boosted by Micron’s (MU) very strong quarterly results, but the earnings and revenue growth rates would still compare favorably with other recent periods when we exclude Micron from these results. Excluding Micron, Q2 earnings for the remaining 33 index members that have reported Q2 results would be up +21.5% (vs. +55.3% otherwise) on +12.5% higher revenues (vs. +18.8% otherwise).

For the Finance sector, we now have Q2 results from 36.6% of the sector’s market capitalization in the S&P 500 index. Total earnings for these Finance companies are up +30.2% from the same period last year on +20.4% higher revenues, with all the companies beating EPS estimates and 90.9% beating revenue estimates. This is a notably better performance from these Finance companies relative to what we have seen from the group in other recent periods.

Banks kick off the Q2 earnings season in style

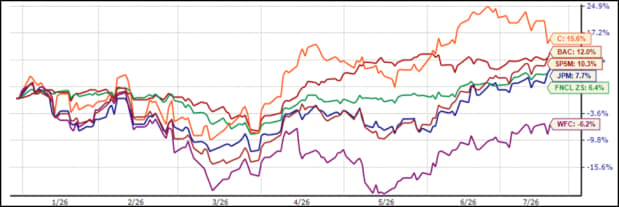

The big banks and brokers kicked off the Q2 reporting cycle in style, comfortably beating consensus EPS and revenue estimates and providing reassuring reads on underlying trends in their businesses. JPMorgan’s (JPM) Q2 earnings increased +21.7% from the same period last year on +27.7% higher revenues, while those for Bank of America (BAC), Citigroup (C), and Wells Fargo (WFC) increased +27.5%, +45.1%, and +18.4%, respectively.

Bank stocks in general and these four stocks in particular have enjoyed a decent but otherwise unspectacular run this year, as some of the earlier geopolitical risk factors have eased lately. Banks are cyclical businesses, so any real or perceived reduction in economic risk is positive for their outlook.

The chart below shows the year-to-date performance of JPMorgan, Bank of America, Citigroup and Wells Fargo shares relative to the S&P 500 index and the Zacks Finance sector.

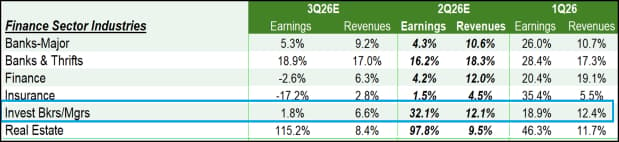

Boosted by the strong results from these banks, total Q2 earnings for the Zacks Investment Banks/Managers industry, of which JPMorgan, Bank of America, Citigroup and Wells Fargo are a part, are expected to increase by +32.1% from the same period last year on +12.1% higher revenues, as the table below shows.

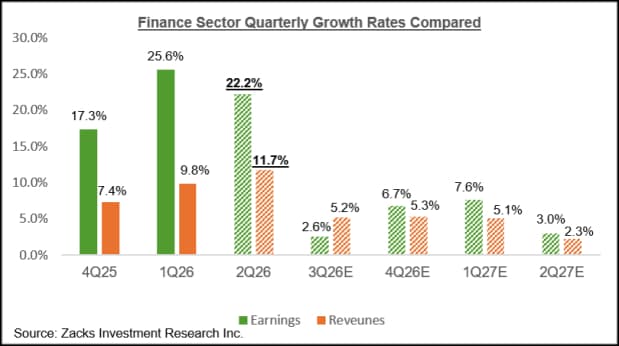

For the Finance sector as a whole, Q2 earnings are expected to increase by +22.2% on +11.7% higher revenues, following the sector’s +25.6% earnings growth on +9.8% higher revenues in the preceding period. The chart below shows the earnings and revenue growth picture for the Zacks Finance sector on a quarterly basis.

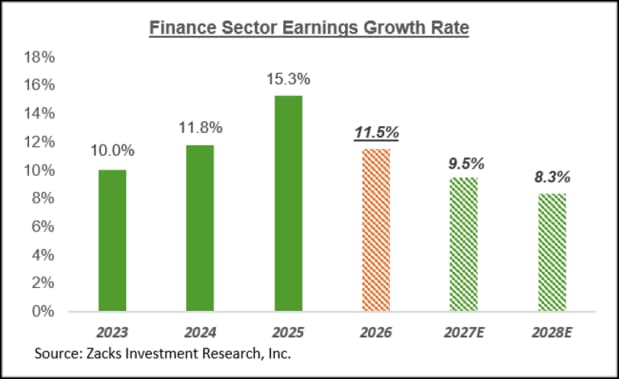

The chart below shows the sector’s earnings growth picture on an annual basis.

The Finance sector is the second largest earnings contributor to the S&P 500 index, behind only the Tech sector, accounting for 16.4% of the index’s expected forward 12-month earnings.

The earnings big picture

The chart below shows S&P 500 expectations for 2026 Q2 in terms of what was achieved in the preceding four periods and what is currently expected for the following three quarters.

The chart below shows the overall earnings picture for the S&P 500 index on an annual basis.

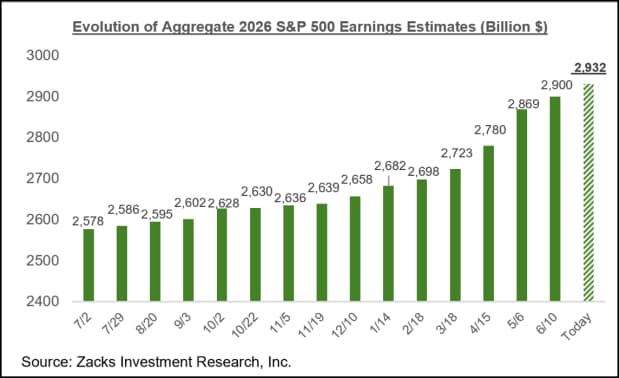

As with estimates for Q2, estimates for full-year 2026 have also been steadily going up, particularly since the start of March. The chart below shows the evolution of aggregate S&P 500 earnings estimates since last July.

Full-year 2026 earnings estimates have increased for 11 of the 16 Zacks sectors since the start of March, with the most pronounced gains at the Energy, Basic Materials, Tech, Industrials, Utilities, and Business Services sectors. On the negative side, estimates have been under pressure for the Transportation, Autos, Medical, and Consumer Discretionary sectors since the start of March. History suggests that these favorable revisions will get a boost from the Q2 earnings season and updated management guidance.

Want the latest recommendations from Zacks Investment Research? Download 7 Best Stocks for the Next 30 Days. Click to get this free report

Author

Zacks

Zacks Investment Research

Zacks Investment Research provides unbiased investment research and tools to help individuals and institutional investors make confident investing decisions.