A positive outlook as Q2 earnings season gets underway

Here are the key points

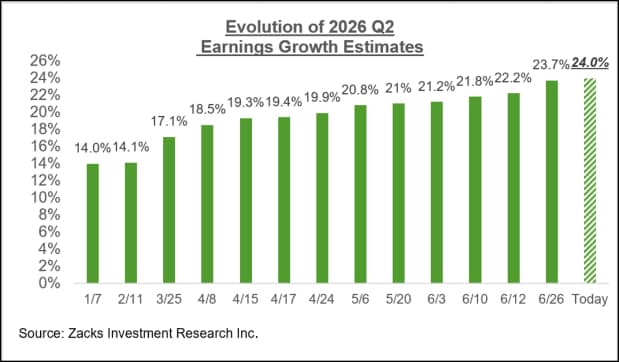

Total Q2 earnings for the S&P 500 index are currently expected to be up +24.0% from the same period last year on +11.3% higher revenues, with 11 of the 16 Zacks sectors expected to enjoy positive earnings growth.

Excluding the significant upward revisions to Energy sector estimates, aggregate Q2 earnings estimates for the remainder of the S&P 500 index would still be in positive territory since the start of April.

The Tech sector has been a critical growth pillar since 2023 Q3 and is expected to continue playing that role in 2026 Q2, with expected earnings growth of +48.5%. Excluding the Tech sector’s substantial contribution, Q2 earnings growth for the rest of the S&P 500 index would be +12.2% (vs. +24.0% otherwise).

Q2 earnings for the ‘Magnificent 7’ group of companies are expected to be up +28.5% from the same period last year on +24.4% higher revenues. Excluding the ‘Mag 7’ contribution, Q2 earnings for the rest of the index would be up +22.5% (vs. +24.0%).

Bank earnings in focus as Q2 earnings season takes the spotlight

JPMorgan (JPM), Bank of America (BAC), Citigroup (C Quick) and Wells Fargo (WFC) kick off the June-quarter reporting cycle for the Finance sector on July 14th. Bank stocks in general and these four stocks in particular have enjoyed a decent but otherwise unspectacular run this year, as some of the earlier geopolitical risk factors have eased lately. Banks are cyclical businesses, so any real or perceived reduction in economic risk is positive for their outlook.

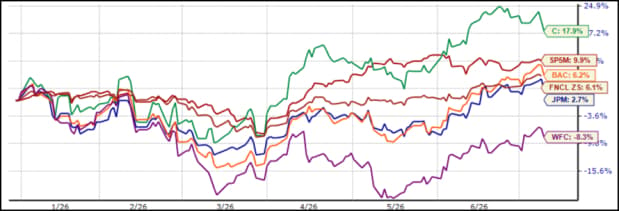

The chart below shows the year-to-date performance of JPMorgan, Bank of America, Citigroup and Wells Fargo shares relative to the S&P 500 index and the Zacks Finance sector.

The revisions trend is positive as a whole, with Q2 estimates for JPMorgan, Bank of America, and Citigroup modestly moving higher, while the same for Wells Fargo are going down a bit.

JPMorgan is expected to earn $5.49 per share on $48.7 billion in revenues in Q2, representing year-over-year changes of +10.7% and +8.5%, respectively. The Zacks Consensus EPS estimate for JPMorgan has increased +1.9% over the past month and +3% over the last three months. Q2 estimates for Bank of America and Citigroup have increased +2.8% and +4.7% over the last three months, while the same for Wells Fargo have decreased by -1.1%.

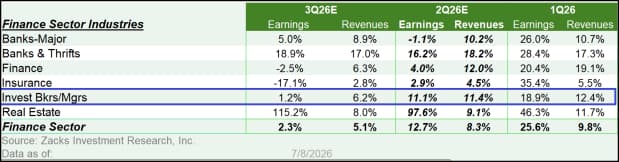

Total Q2 earnings for the Zacks Investment Banks/Managers industry, of which JPMorgan, Bank of America, Citigroup and Wells Fargo are a part, are expected to increase by +11.1% from the same period last year on +11.4% higher revenues, as the table below shows.

The growth in Q2 will come from the core banking and trading franchises, with investment banking activities largely stable. On the core banking side, loan growth is expected to accelerate further from the very strong numbers in the preceding quarter, with industry-wide data suggesting that Q2 loan growth will reach its highest level in three years. Growth is expected to expand into higher-margin categories such as commercial & industrial (C&I), autos, credit cards, and others.

For context, loan growth has trended below historical averages over the past three years, but the growth pace began improving in 2025, and the trend continued into 2026 Q1. The favorable outlook for loan portfolios bodes well for net interest income in Q2 and beyond, even though the yield curve lost some of its steepness in Q2. We remain skeptical of the consensus Fed view of a rate hike later this year, but renewed hostilities in the Persian Gulf will keep the inflation debate alive and kicking.

On the investment banking front, we should get solid numbers from the capital markets side of the business, particularly on the equity capital markets front. But M&A activities have been underwhelming, reflecting the effects of geopolitical uncertainties. Trading revenues remained robust in Q2, with mid-quarter updates indicating growth rates in the +10% to +15% range.

Aggregate trends on the credit quality front have been benign, as reflected in household and commercial delinquencies, bankruptcies, debt-service and other metrics. But the market’s focus will be private-credit exposure for banks, as the space has been in the spotlight lately for its exposure to the software and data-center industries.

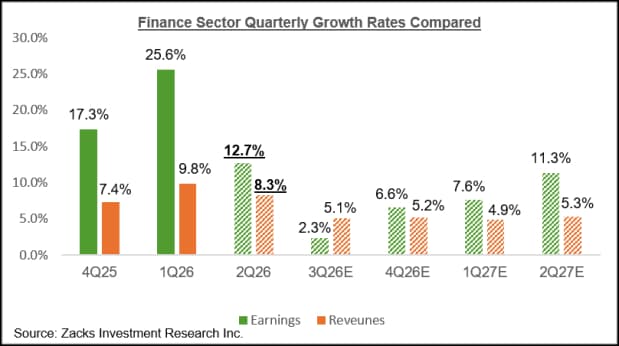

For the Finance sector as a whole, Q2 earnings are expected to increase by +12.7% on +8.3% higher revenues, following the sector’s +25.6% earnings growth on +9.8% higher revenues in the preceding period. The chart below shows the earnings and revenue growth picture for the Zacks Finance sector on a quarterly basis.

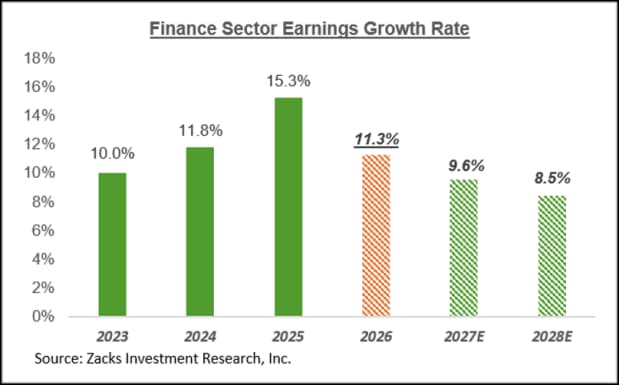

The chart below shows the sector’s earnings growth picture on an annual basis.

The Finance sector is the second largest earnings contributor to the S&P 500 index, behind only the Tech sector, accounting for 16.4% of the index’s expected forward 12-month earnings.

Keeping track of the revisions trend

The expected decline in Energy sector estimates notwithstanding, the overall revisions trend continues to be positive, with estimates for 2026 Q2 and full-year 2026 increasing. This favorable earnings backdrop is evident in the revisions trend, as seen in how expectations for 2026 Q2 have evolved in recent weeks.

The sectors enjoying positive estimate revisions since the start of April included Energy, Tech, Basic Materials, Utilities, and Business Services. Aggregate Q2 earnings estimates would still be positive since the start of the period, even without favorable revisions for the Energy sector, but aggregate estimates would be down if we exclude the increases in the Energy and Tech sector estimates.

The Tech sector has been enjoying positive estimate revisions for more than a year now, so the sector’s ongoing positive revisions trend is basically more of the same. We have discussed in this space the positive revisions that the Mag 7 group has been experiencing.

On the negative side, Q2 estimates were under pressure for the Transportation, Autos, Medical, Consumer Discretionary, Consumer Staples, and other sectors.

The chart below shows S&P 500 expectations for 2026 Q2 in terms of what was achieved in the preceding four periods and what is currently expected for the following three quarters.

The chart below shows the overall earnings picture for the S&P 500 index on an annual basis.

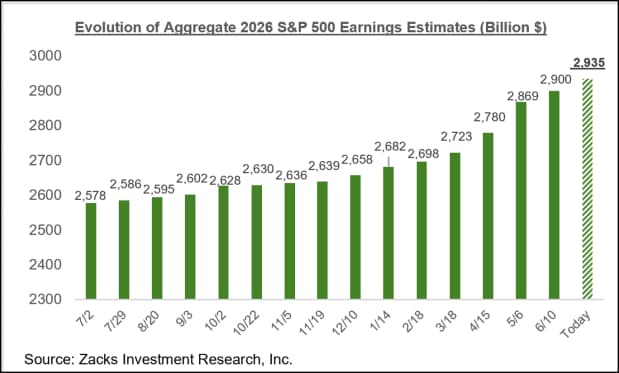

As with estimates for Q2, estimates for full-year 2026 have also been steadily going up, particularly since the start of March. The chart below shows the evolution of aggregate S&P 500 earnings estimates since last July.

Full-year 2026 earnings estimates have increased for 11 of the 16 Zacks sectors since the start of March, with the most pronounced gains at the Energy, Basic Materials, Tech, Industrials, Utilities, and Business Services sectors. On the negative side, estimates have been under pressure for the Transportation, Autos, Medical, and Consumer Discretionary sectors since the start of March. History suggests that these favorable revisions will get a boost from the Q2 earnings season and updated management guidance.

Want the latest recommendations from Zacks Investment Research? Download 7 Best Stocks for the Next 30 Days. Click to get this free report

Author

Zacks

Zacks Investment Research

Zacks Investment Research provides unbiased investment research and tools to help individuals and institutional investors make confident investing decisions.