The $270 billion speculation machine behind the AI wreck

- The trade: AI, SpaceX and crypto exposure increasingly sit inside the same leveraged speculation complex, even when the wrappers look different.

- The catalyst: A valuation-driven rotation out of mega-cap technology triggered mechanical deleveraging across products built to magnify daily moves.

- The risk: Daily-reset leveraged ETFs can turn volatility into forced buying on the way up and forced selling on the way down.

- What matters next: Watch rebalancing flows, single-stock ETF assets, options positioning and whether retail keeps buying the wrappers after the underlying story begins to wobble.

The $270 billion speculation machine

There has been an astonishing amount of forensic work going on behind last week’s tech wreck. Normally, I do not spend too much time analysing spilled milk. Markets break, people reach for the nearest explanation, and by the time the autopsy is complete the next trade is already walking through the door.

But this one is worth studying, because the damage was not simply a bad week for expensive AI stocks. It was a glimpse inside the machinery that has grown around every hot market narrative: more leverage, more wrappers, more ways for investors to own the same idea without necessarily owning more understanding of it.

As Bloomberg’s postmortem made clear, the AI selloff did not begin with leveraged ETFs, single-stock options, SpaceX trackers or crypto-adjacent products. Those vehicles did not cause the fire. They were the oxygen.

Once the market began rotating away from its largest AI winners on valuation concerns, the same products designed to turbocharge the upside became automatic amplifiers on the way down. The market had spent months building a taller and taller tower on the same narrow patch of ground. When the foundation shook, every additional floor became part of the problem.

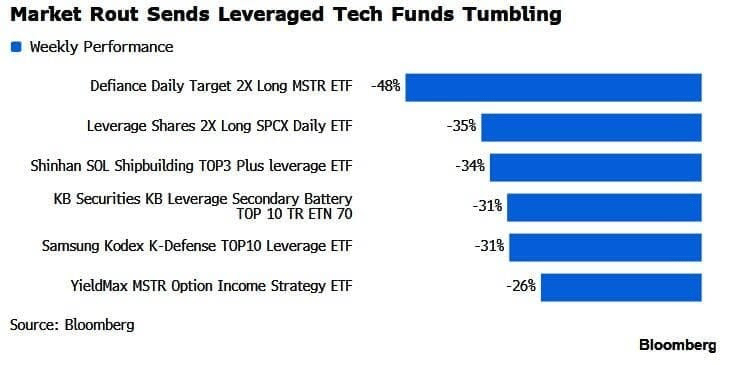

South Korea offered the clearest warning. Retail investors there have become some of the most aggressive users of two-times and three-times funds tied to AI chipmakers and other fashionable trades. Several of the country’s most prominent vehicles lost more than 20% during the week. That is the daily-reset leverage trap in plain sight: the product works beautifully while momentum runs in your favour, but it does not need a prolonged bear market to hurt. A few ugly sessions, some volatility drag and a crowded exit can do the job.

Then came SpaceX, Wall Street’s newest shiny object. Leveraged funds linked to the rocket company attracted almost $1 billion shortly after launch, even as the bullish products fell roughly 40% from their debut. That is the modern retail trade in miniature: buy the story late, add leverage because the underlying is already expensive, and discover that the price paid for easy access was far higher than it first appeared.

The scale of the ecosystem is no longer trivial. Leveraged ETFs now oversee more than $270 billion globally, with over $200 billion in the US and more than $45 billion in Asia, according to Bloomberg data. These funds use derivatives to deliver multiples of an asset’s daily move, and that daily reset is the important part. When markets swing hard, the funds must rebalance. Up markets can force them to buy more exposure into strength. Down markets can force them to sell more into weakness.

That does not mean every dip is caused by ETF mechanics. It does mean that once enough money sits inside these structures, they can turn an ordinary move into something with sharper edges. Barclays estimates that US leveraged-ETF rebalancing has recently run at several times its long-term average. In a market already dominated by a handful of mega-cap technology names, that is not background noise. It is an extra hand on the wheel.

The broader index damage still looked manageable on paper: the S&P 500 fell nearly 2% for the week, while the Nasdaq 100 lost more than 4%. But beneath the surface, the losses were concentrated in the kinds of assets that had become vehicles for maximum conviction. AI chips, single-stock technology funds, SpaceX exposure and crypto proxies were not really separate trades. They were different doors into the same casino.

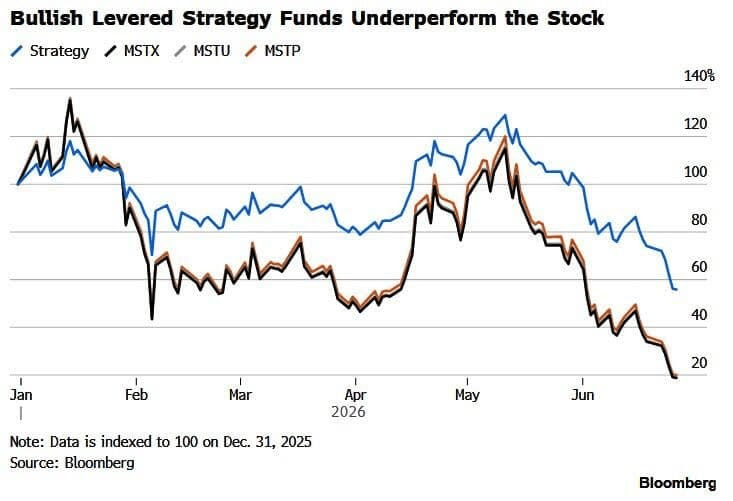

Strategy Inc. is another example. What began as a corporate Bitcoin exposure has steadily become a whole financial-engineering complex: common equity, preferred shares, ETFs and leveraged products, all allowing investors to express a view on Bitcoin through different wrappers. When sentiment turned, those wrappers came under pressure together. Bullish and bearish leveraged ETFs tied to Strategy, launched in 2024, have each lost more than 90% from inception despite attracting billions in assets. Preferred shares that were meant to provide a steadier income route into the same theme also slipped below par.

Different products. Same crowded room.

That is the real lesson from the AI rout. Every bull market creates demand for a faster horse. Wall Street is very good at supplying one. First comes the stock. Then comes the ETF. Then the two-times ETF, the three-times ETF, the options chain, the structured note, the preferred share, the token, the prediction contract and whatever else can be wrapped around the original narrative.

By the time the cycle matures, investors are no longer debating the company or the asset itself. They are debating the cleanest, quickest and most leveraged way to rent exposure to it for a day.

The danger is not leverage by itself. Professional markets have always used leverage. The danger is leverage combined with crowding, retail momentum, thin understanding and products that mechanically must buy and sell into already violent price action. That is how a healthy rally can begin to look less like investment and more like a high-speed conveyor belt carrying everybody toward the same narrow exit.

Last week was not necessarily the beginning of something darker. It may simply have been a warning shot. But the $270 billion leveraged-ETF complex, and the expanding ecosystem around AI and crypto, means the next reversal may not behave like old-fashioned profit-taking.

The market has built more accelerators than brakes...

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.