Will Dollar strength hold in Q3? FX outlook 2026

The Dollar enters Q3 as the market’s first line of defence against sticky inflation, geopolitical stress and a Federal Reserve that can afford to wait.

That support is fundamental, not merely technical. The immediate uncertainty is whether DXY can clear weekly resistance and whether higher yields begin to destabilise risk-sensitive assets.

That is why AUDJPY and GBPJPY matter later in this outlook: a synchronised breakdown would show that pressure is spreading from cyclical currencies into the yen-funded carry trade.

The dollar starts Q3 with an advantage.

The dollar’s early-Q3 edge comes from a Federal Reserve that can remain restrictive while several peers face weaker growth or greater energy exposure. That gives USD a genuine fundamental advantage.

At the 26 June 2026 chart snapshot, DXY was testing 101.229 and its weekly 200W-EMA band. A break opens 103.842-104.683, while rejection could simply be a delay of the broader bullish case in Q3.

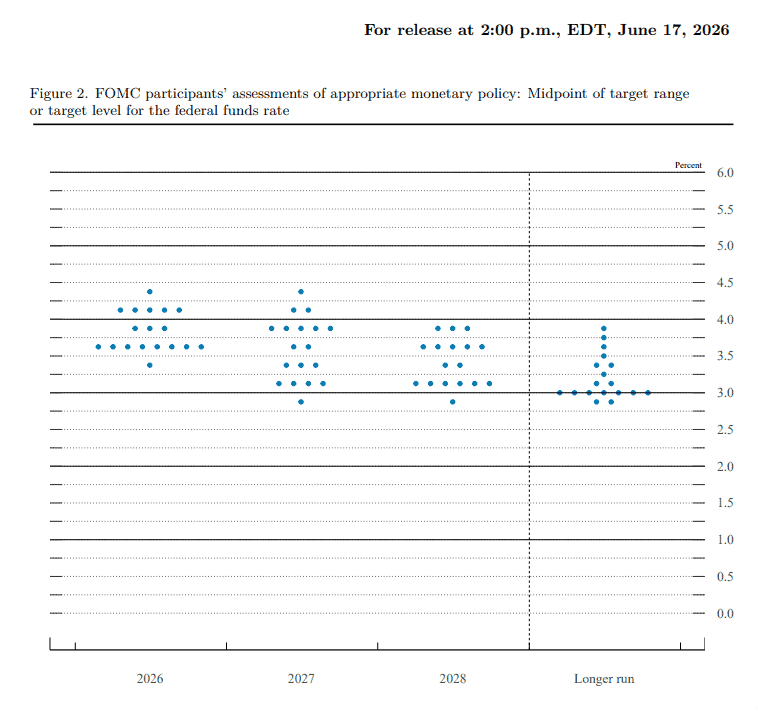

What the June dot plot actually says

The 17 June projections showed a difficult mix: 2026 growth was trimmed to 2.2%, while PCE inflation rose to 3.6% and core PCE to 3.3%. The Fed saw slower growth, but not enough weakness to justify a rescue.

The median year-end rate projection rose to 3.8%, yet the dots were split between hikes and no change. The Q3 message is not that a hike is certain, but that cuts have lost credibility.

i. Base case: The Fed holds while inflation remains uncomfortable and employment stays positive.

ii. Hawkish risk: Core inflation broadens, oil rises and the US 2-year yield moves higher.

iii. Dovish risk: Payrolls, hours, claims and credit conditions weaken together.

This keeps USD fundamentally supported through Q3. A more durable reversal would require front-end yields to fall alongside softer labour, normalising oil or a clear change in Fed expectations.

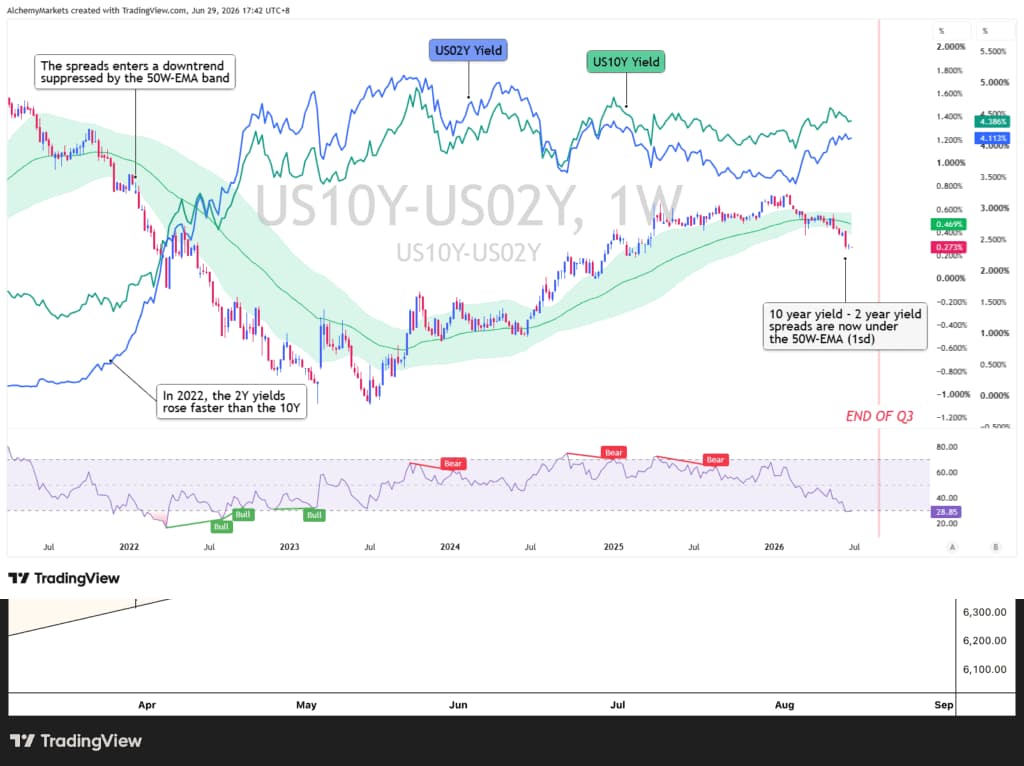

Yield spread shows why Dollar is gaining strength

The US 10-year minus 2-year spread helps distinguish between policy-led dollar strength and pressure coming from longer-term inflation, Treasury supply or fiscal concerns. A narrowing spread is most supportive for USD when the 2-year yield rises faster than the 10-year, as this points to a more restrictive Federal Reserve path.

i. Spread narrows as the 2-year rises: Hawkish Fed repricing and the cleanest USD-positive setup.

ii. Spread widens as the 2-year falls: Softer Fed expectations and a more USD-negative signal.

iii. Spread widens as the 10-year rises: Inflation, Treasury supply or term-premium pressure; USD support depends on credit and risk assets remaining stable.

iv. Both yields fall sharply: Growth or disinflation concerns are taking over; the dollar response depends on whether markets price orderly easing or wider financial stress.

At our 29 June snapshot, the 10Y-2Y spread had moved below its weekly 50-EMA band as the 2-year yield moved closer to the 10-year.

In 2022, aggressive Fed tightening pushed short-term yields above long-term yields, while the same front-end repricing supported DXY. The inversion did not cause dollar strength; both came from the same policy shock.

US 10-year minus 2-year spread: The spread has moved below its weekly 50-EMA band as the 2-year yield catches up with the 10-year. Alchemy Markets / TradingView, 29 June 2026.

Oil remains the bridge between geopolitics and rates

Oil and the US-Iran conflict remain central to the Q3 FX outlook. Continued de-escalation and peace talks have so far helped contain inflation expectations, limiting the pressure on central banks to become even more hawkish.

However, the attacks on vessels passing through the Strait of Hormuz on 27-28 June exposed how fragile the 17 June memorandum remains.

FX traders should therefore continue monitoring geopolitical tensions throughout Q3. Although markets appear increasingly desensitised to the repeated cycle of threats, retaliation and temporary stand-downs, another serious escalation could still threaten the agreement.

If either side formally declares the deal over, we expect the initial market reaction to be bullish for both oil and the dollar as inflation expectations rise and the case for Fed easing weakens.

The Q3 base case is managed instability. Talks may continue, but further disputes over Hormuz transit rules or attacks on vessels could force markets to reprice oil, inflation and the dollar before the mid-August negotiation deadline.

Author

Zorrays Junaid

Alchemy Markets

Zorrays Junaid has extensive combined experience in the financial markets as a portfolio manager and trading coach. More recently, he is an Analyst with Alchemy Markets, and has contributed to DailyFX and Elliott Wave Forecast in the past.