A preview of NFP

NFP

I will be in Canada tomorrow, so I am previewing NFP today. The number is of much greater importance than usual as the Fed moves away from a forecasting framework and towards a current-data / rebuilding-credibility framework. While I have been pooh-poohing Warsh’s hawkish opener, I am also open to the idea that if he is serious about rebuilding credibility, he can find enough hawkish votes, and if June NFP (released tomorrow) is another hot one—July FOMC could be in play. Without the smoking gun of a hot payrolls report, the collapsing price of oil and plummeting inflation forwards should put an end to the July discussion pretty quickly.

What does a smoking gun look like? 4.2% UR and 150k or hotter. Maybe 4.3% UR and 175k or hotter. Anything cooler than that and I don’t believe they will consider a hike in July. The entire strip is somewhat conditional on the July meeting, in my opinion, because if you’re dovish and you survive July, you have time to wait for the disinflationary CPI and PCE prints that will inevitably land later in the summer.

Then, the Warsh Fed will have no reason to hike as progress on inflation will be satisfactory and the June FOMC will end up as the peak hawkish moment. At that point, the dots submitted for June FOMC will look like an out-of-date response to high oil prices and the new regime of oil and retail gasoline prices similar to pre-war levels will cause a swift recalibration of same said dots.

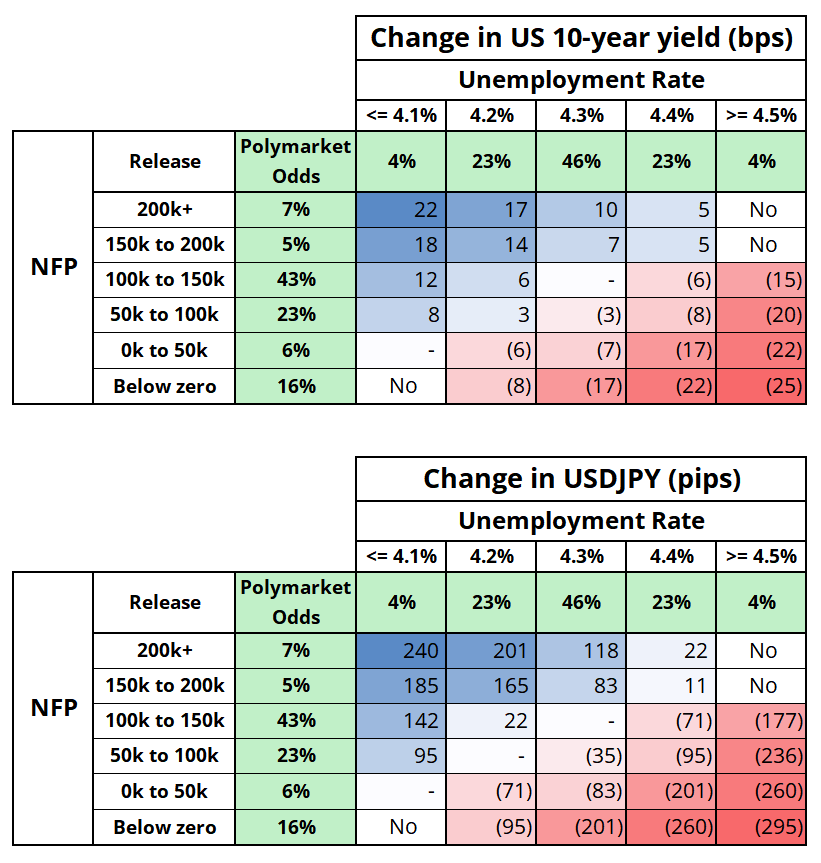

On the next page, I offer two grids showing how I expect 10s and USD/JPY to react to a variety of UR/NFP combos. In green are the Polymarket odds for each outcome, but note you cannot multiply the probabilities to get a combined probability because NFP and UR are not independent. You’re not getting 4.4% UR and +200k NFP, e.g.

One huge caveat with the USDJPY grid is that there is also the question of MOF intervention. The G7 mantra is that FX should reflect fundamentals and therefore it’s tricky and awkward for the MOF to intervene on a strong figure. On the other hand, it would make perfect sense for them to come in and smash USD/JPY on a soft outcome. So there is a big left tail there if we get a weak number and the MOF makes the tactical call that intervention on a semi-holiday after weak jobs is a winner. It would be an excellent tactical move.

Unilateral MOF interventions almost always yield a 3.0%-3.5% drop, so you are looking at 157.10/157.90 as the buy zone if they come in. In the very unlikely event of coordinated intervention, we might see 155.00. MOF intervention is a buy dips while coordinated intervention transforms USDJPY into sell rallies because it has a much better track record of marking major turns.

Here are the grids, as promised.

Gold

We are in a regime where G10 FX is trading like the good old days as interest rate differentials and gold are moving pretty much tick for tick with the majors. Tomorrow’s NFP will have a lot to say, therefore, about the direction of gold. On a short-term chart, it’s mildly interesting that gold is making a nice triple top after two solid holds and one splashy chop down/rip up. If the jobs report is stonking, this will not matter, but I suppose if you’re bullish gold and want to use a tight stop, you know where you are wrong.

Final thoughts

I don’t expect much from Warsh at Sintra today. In the old days, we might have hoped for a signal on the July meeting, but Mr. Warsh does not seem interested in dropping breadcrumbs.

I mentioned earlier that the G7 mantra is that FX should reflect fundamentals. Depending on their level of zoom, Bessent and Takaichi might be looking at this chart and thinking: USDJPY looks wrong.

MSTR moved a few deck chairs around. Let’s see if it makes a difference. The reality remains that it’s a leveraged, cash-flow-negative holder of a zero-cashflow asset that is falling in price. All they can do is buy time and pray for higher BTC prices. Tick tock.

Messi’s World Cup debut. Check out that lid!

Nobody Does It Better than Thom Yorke.

Author

Brent Donnelly

Spectra Markets

Brent Donnelly is the President of Spectra Markets. He has been trading currencies since 1995 and writing about macro since 2004. Brent is the author of “Alpha Trader” (2021) and “The Art of Currency Trading” (Wiley, 2019).