What’s next for US Copper import tariffs

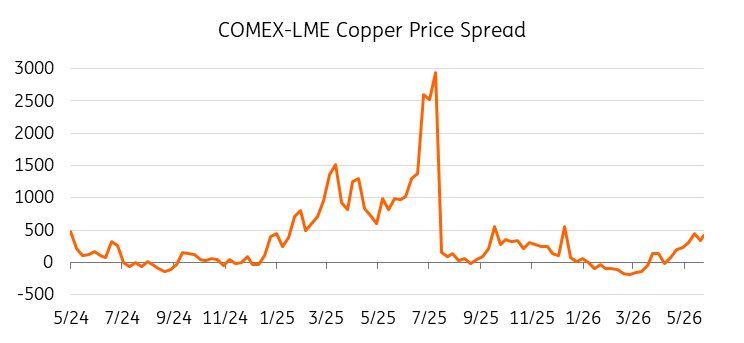

The US tariff decision on copper imports is weeks away, with the Commerce Secretary due to deliver a recommendation to President Donald Trump by 30 June. The market has already begun pricing the outcome. The COMEX-LME spread has widened to around $400/t, suggesting the market continues to price meaningful tariff risk into US-delivered refined copper.

Where we are now

LME copper is trading near record highs, with prices up around 10% year-to-date and holding up well against a difficult macro backdrop. Strong US jobs data has reinforced expectations that the Federal Reserve will keep policy restrictive for longer, while renewed tensions involving Iran have weighed on broader risk sentiment.

Supply tightness, US tariff-driven stockpiling and AI-linked power demand are keeping copper more resilient than the broader complex, with the tariff decision now only weeks away.

What the tariff decision looks like

When President Trump announced a 50% tariff on copper in July 2025, refined copper was carved out. That exemption is now under review. The Commerce Secretary has until 30 June to deliver an updated recommendation to Trump on whether and how to extend tariffs to refined copper. The original Commerce Department proposal called for a 15% tariff on refined copper imports effective January 2027, escalating to 30% in 2028.

Earlier this month, Trump signed a proclamation adjusting the broader metals tariff framework – maintaining the 50% tariff on semi-finished copper products, lowering the domestic content threshold from 95% to 85% to qualify for preferential treatment, and broadening the scope to include additional semi-fabricated products such as electrical conductors and cables. New rates took effect 8 June. These changes are widely seen as preparatory steps ahead of the refined copper review, making it easier for importers to qualify for preferential treatment tied to domestically produced metal.

How the market has already repositioned

Since February, US copper imports have spiked in anticipation of the tariff deadline, encouraging additional shipments into the US and tightening supply in other regions.

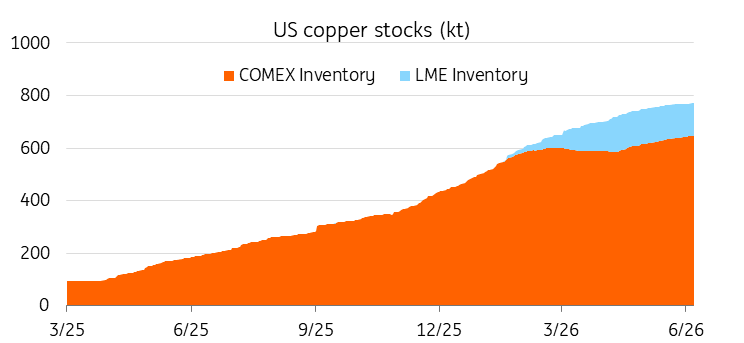

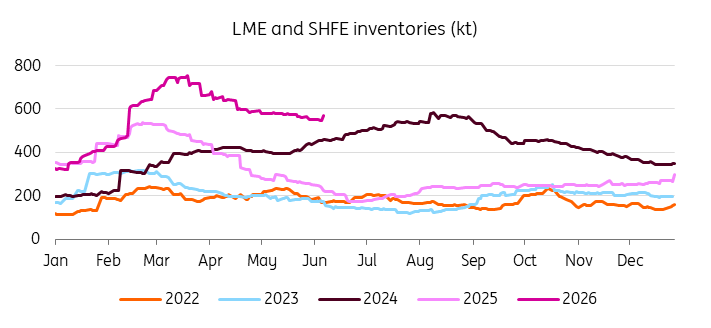

COMEX-registered inventories have risen to record highs. That build has come directly at the expense of LME and SHFE stocks, which have declined sharply over the same period.

COMEX stocks hit records, LME inventories also trend higher

Meanwhile ex-US inventories have declined sharply

This is not a demand-driven inventory build. It reflects a geographic redistribution of available metal driven by tariff arbitrage. A significant volume of copper cathode is now economically 'locked' into the US market. While some of this metal could eventually be released if tariff expectations fade, the prospect of further trade policy measures means inventories are increasingly being held as strategic rather than ‘arbitrageable’.

The COMEX-LME spread began re-widening from early 2026 as the 30 June deadline came into focus. It turned positive again in late March and has been climbing since, reaching around $400/t in early June. At current levels, the spread is well below the peak of around $2,937/t seen in late July 2025 when a 50% tariff on all copper was briefly feared. This suggests the market views a 15% phased tariff as a much more contained outcome.

COMEX-LME Copper spread rewidens

What happens after the announcement

A confirmed 15% phased tariff from 1 January 2027 would likely increase the premium of COMEX over LME copper. In practice, both benchmarks would move higher. COMEX would be supported by stronger US import demand, while LME would also benefit as metal diverted away from the US tightens supply availability elsewhere.

The overall impact would be supportive for copper prices globally, although the larger move would likely occur in COMEX.

If the proposed increase to 30% in 2028 is brought forward or confirmed as a near-term policy objective, the premium could expand further.

A delay represents the clearest near-term downside risk for the spread, although the impact would likely be more limited than an outright rejection of tariffs. The arb would compress and the pace of inflows into COMEX would slow – but material already stockpiled in the US is unlikely to leave the market quickly. As long as tariff risks remain, a significant portion of those stocks is likely to remain effectively locked within the US market. The spread would narrow, but would probably settle at a structurally wider level than pre-2025 norms rather than collapsing back to parity.

An outright rejection of tariffs remains the most bearish case. US import demand would drop sharply, and with the stockpiling incentive removed, both benchmarks would likely come under pressure. US-held metal could then potentially re-enter the global market or at least stop being 'locked' in the US.

Supply outlook remains tight

We forecast the global copper market to move into a deficit of around 35kt in 2026, reflecting mine supply losses across Indonesia, Chile, the DRC and Zambia, alongside disruptions to Middle Eastern sulphur flows and sustained end-use demand in electrification and grid infrastructure. The tariff outcome does not change that underlying market balance. However, it will determine how quickly the deficit becomes visible in exchange inventory data and how the price gap between COMEX and LME evolves.

We see LME copper broadly supported at current levels through 2Q, before easing modestly into 3Q and 4Q as the initial tariff stockpiling impulse fades and macro headwinds persist. The tariff announcement itself represents near-term upside risk to our near-term forecast. A front-loaded 30% tariff would put further upside in play. Conversely, a delay or outright rejection of tariffs represents the clearest downside risk to our view over the second half of the year.

The 30 June deadline and the COMEX-LME spread are the two indicators to watch most closely over the coming weeks.

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.