Week ahead – US CPI to test market nerves, RBNZ might cut rates [Video]

-

Market turmoil has eased, but will US CPI stir things up again?

-

Crucial week for sterling as UK CPI, GDP and retail sales on the way.

-

The RBNZ is edging closer to a rate cut, but will it be next week?

-

Japanese GDP, Australian jobs and Chinese data eyed too.

![Week ahead – US CPI to test market nerves, RBNZ might cut rates [Video]](https://editorial.fxstreet.com/images/Macroeconomics/EconomicIndicator/Prices/CPI/consumer-price-index-gm500080630-80587217_XtraLarge.jpg)

US economy worries take front and center

The panic about the US economy being on the verge of a recession has mostly eased but markets remain jittery. Investors see a real risk that the Fed’s delay in cutting rates has made a downturn inevitable. Sticky inflation is the main reason why the Fed has stayed this cautious. But inflationary pressures finally seem to be receding in a more sustainable manner.

Next week’s CPI report is expected to underscore this trend and in the absence of any surprises, the data may not do much in allaying the slowdown fears as the focus has shifted somewhat to the growth side of the story. But in the event that the inflation numbers shock either to the upside or downside, the ripple effects will certainly be more notable.

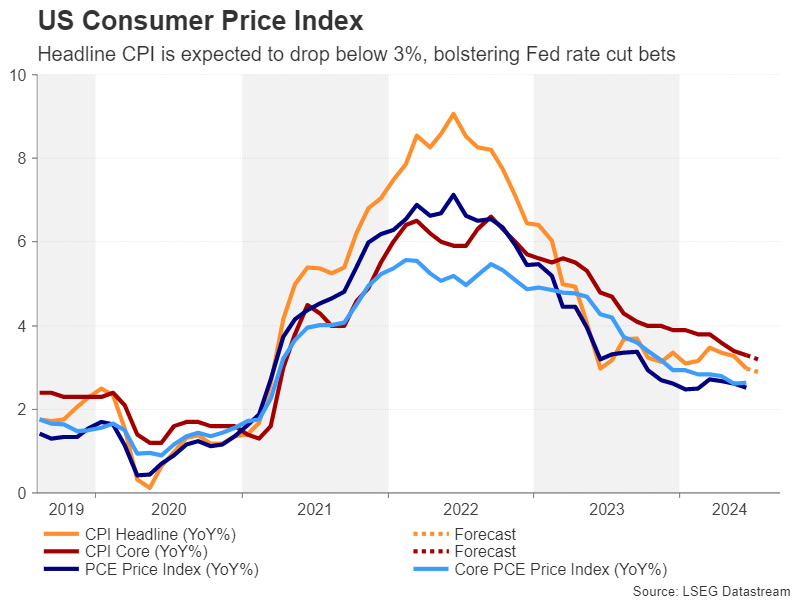

CPI to likely maintain downward trajectory

The headline rate of CPI is expected at 2.9% y/y in July, easing slightly from the prior 3.0%. The month-on-month figure is anticipated to have accelerated, however, from -0.1% to 0.2%. Core CPI is forecast to slow too on an annual basis from 3.3% to 3.2%, but inch up from 0.1% to 0.2% month-on-month.

A large upside surprise would be the worst outcome for the markets as it would mean the Fed won’t be able to slash rates very rapidly even as the economy is losing steam. On the other hand, a big miss would likely boost expectations that the Fed will cut rates by 50 basis points in September, cheering investors.

A busy US agenda

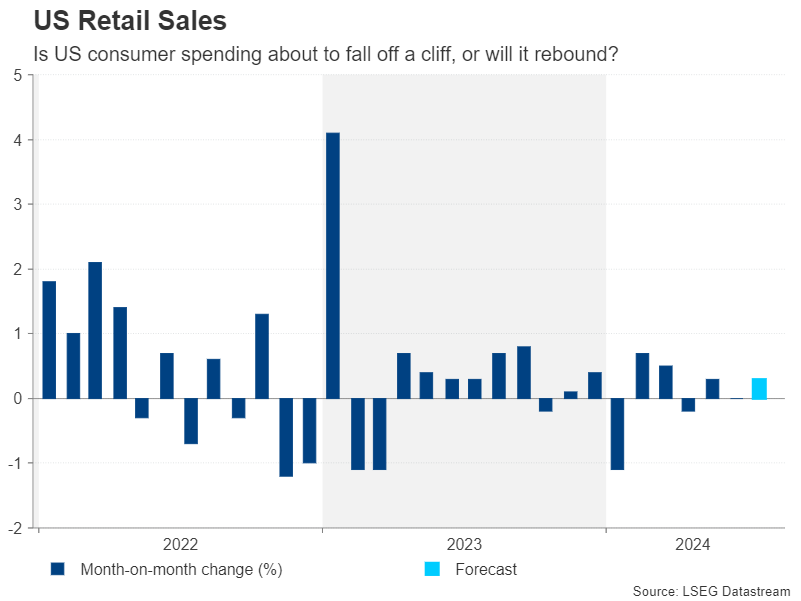

The CPI numbers are due on Wednesday and will be preceded by producer prices on Tuesday, while on Thursday, the spotlight will turn to retail sales. After flat growth in June, retail sales are forecast to have risen by 0.3% month-on-month in July, which may go some way in calming fears about a recession.

On Friday, the University of Michigan’s consumer sentiment survey will also be important, in particular, the inflation expectations for the next one and five years. Other releases will include the New York and Philly Fed’s manufacturing gauges, as well as industrial production for July, all out on Thursday, while on Friday, building permits and housing starts will attract some attention too.

If the upcoming data give a further green light to aggressive rate cuts, the US dollar could come under renewed pressure, having barely rebounded from the past week’s selloff.

Pound on the backfoot ahead of UK data flurry

The pound has retraced almost all its July gains, underperforming all other majors this month apart from the dollar. Although the Bank of England’s rate cut is to blame for some of this weakness, the riots across English cities have also been weighing on sterling as they’ve occurred just as investors had priced out political risks for the UK.

However, the focus over the next seven days will firmly be on the economy, starting with the labour market report on Tuesday. A somewhat cooler labour market has helped wage growth moderate to 5.7% y/y but ideally, BoE policymakers will need to see a further drop before being ready to lower rates again.

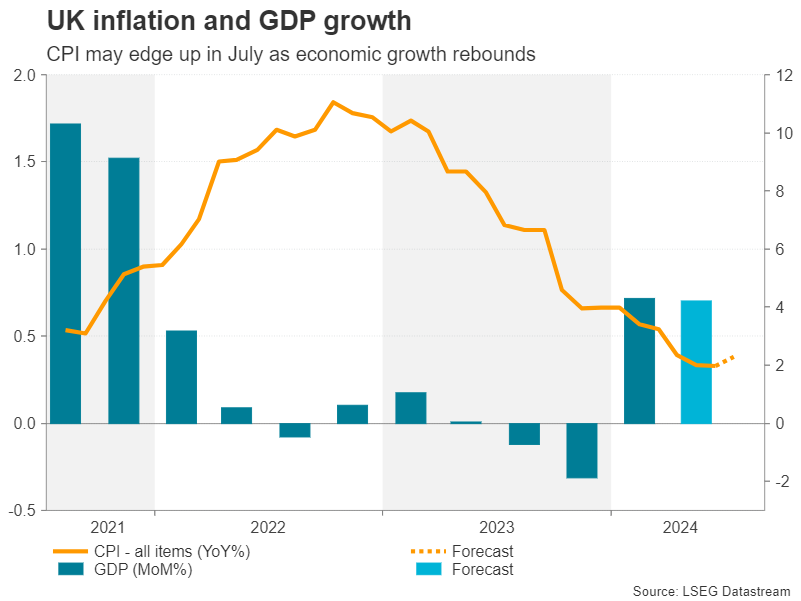

July CPI figures will follow on Wednesday and could be key to shaping rate cut expectations for the BoE’s September gathering as the odds for a second 25-bps reduction currently stand at around 30%. Headline inflation was unchanged at 2.0% in June – bang on the BoE’s target. But it probably edged up in July to 2.3% y/y, supporting the reasoning behind the hawkish cut at the August meeting.

Investors will also be keeping a close eye on services CPI, which like wages, remains elevated.

On Thursday, the UK will publish preliminary GDP readings for the second quarter. The economy is projected to have expanded by 0.7% q/q in Q2, maintaining the same pace as in Q1. Rounding up the weekly releases on Friday will be July retail sales.

Although the likelihood of a back-to-back rate cut in September is quite low, a broadly soft set of data could nevertheless push up market expectations, in a further setback for sterling.

Will the RBNZ join the rate-cut club?

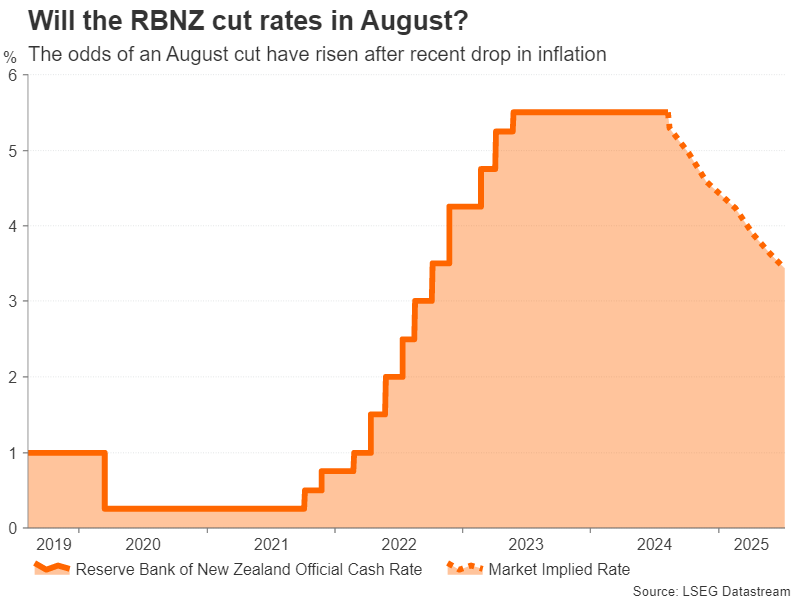

The Reserve Bank of New Zealand meets on Wednesday for its latest policy decision. Economists are not anticipating any change but there is growing consensus among traders that the RBNZ will announce a 25-bps reduction in the cash rate. Easing expectations started to gain traction after the previous meeting when policymakers sounded upbeat about the prospect of inflation returning to the 1-3% target range in the second half of this year, which was later backed by the Q3 CPI report that showed inflation falling to 3.3%.

Further building the case for looser policy was the RBNZ’s own survey on inflation expectations that pointed to the lowest expectations in more than three years.

Subsequently, investors have ramped up their bets for an August cut to about 80% so should the RBNZ decide to proceed with one, the New Zealand dollar will probably not suffer huge losses unless policymakers signal that more are on the way.

Can the aussie extend its recovery?

With the RBNZ looking certain to begin reducing rates later this year if not at the August meeting, the RBA is increasingly becoming the odd one out. Governor Michelle Bullock has pushed back on market bets of a cut anytime soon, but investors still see a reasonable chance of a move by December.

Nonetheless, the RBA’s hawkish stance is supporting the Australian dollar’s rebound attempt against the greenback, although next week’s releases may pose a downside risk. The wage price index for the second quarter is due on Tuesday and the employment report for July is coming up on Thursday.

In addition to domestic indicators, aussie traders will also be watching China’s latest monthly data dump. The July readings for industrial production, retail sales and fixed asset investment are out on Thursday. Any disappointment, especially with retail sales, would add to concerns that China’s economy is stuck in the slow lane, possibly hurting the aussie.

Yen bulls look to Q2 GDP

Finally in Japan, second quarter GDP numbers are due on Thursday. The data will be vital for the Bank of Japan where there’s an ongoing debate about whether the economy is strong enough to withstand higher interest rates. Other releases will include corporate goods prices on Tuesday and machinery orders on Friday.

The yen rally is currently taking a breather after the impressive gains over the past month. However, a print that’s stronger than the expected 0.5% q/q could revive the bulls.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics. Following graduation, he joined PricewaterhouseCoopers in the Business Recoveries team, where he was responsibl