Wall Street shakes off tariff blues, dances to the disinflation beat

Wall Street is back in full swagger mode, shaking off April’s tariff tantrums and marching higher as the market sniffs out a lasting trade war détente and a not so hyper inflation pulse. The S&P 500 recorded its fourth consecutive gain, closing at 5,916.93, while the Dow climbed 272 points higher to settle above 42,300. The Nasdaq, meanwhile, hit the pause button after a sizzling week, slightly dragged down by late-day META drama over AI rollout delays—but still resting on a 6% weekly gain, with Nvidia and Tesla leading the charge like caffeinated greyhounds, both up 15%+ week-to-date.

This rally isn’t just about rosy headlines—it’s about bond yields finally cracking under the weight of disinflationary signals and a growing sense that maybe, just maybe, the tariff-induced inflation firestorm might be tamer than feared. The market is back flirting with the idea that Fed Governor Waller might be right—that the tariff bump could prove transitory rather than systemic. The Producer Price Index print of -0.5% for April—versus a +0.3% expectation—echoed the tame CPI read earlier in the week. Bond traders took that as their cue to hit the “buy” button, sending the 10-year yield down nine basis points on the day to 4.44%, even though it’s still 7 to 8 basis points higher on the week. The dollar softened in turn, while Fed cut bets were gently nudged back onto the table.

The long-running divergence between soft data (survey-based sentiment) and hard data (real economic output) is finally starting to close—but not in the direction the establishment PhD crowd promised. Instead of real activity rolling over to meet downbeat sentiment, it’s the surveys that are playing catch-up. The mood music is shifting. Business sentiment is perking up just as the actual economic data holds firm.

Thursday’s macro smorgasbord said it all: jobless claims came in strong, factory output surprised to the upside, retail sales managed a modest beat( or in line, subject to whose data you use), and the Philly Fed index staged a monster bounce. The only real blemish was a drop in homebuilder confidence—but that’s a rate-sensitive corner that’s been wobbling all year. The rest of the tape suggests momentum is quietly re-accelerating beneath the surface. Those hedging for stagflation are watching their thesis get chipped away, one data point at a time. The question now isn't whether the economy is slowing—it’s whether the market has been underestimating its resilience all along. Hence, the bears are finding fewer cracks to wedge into.

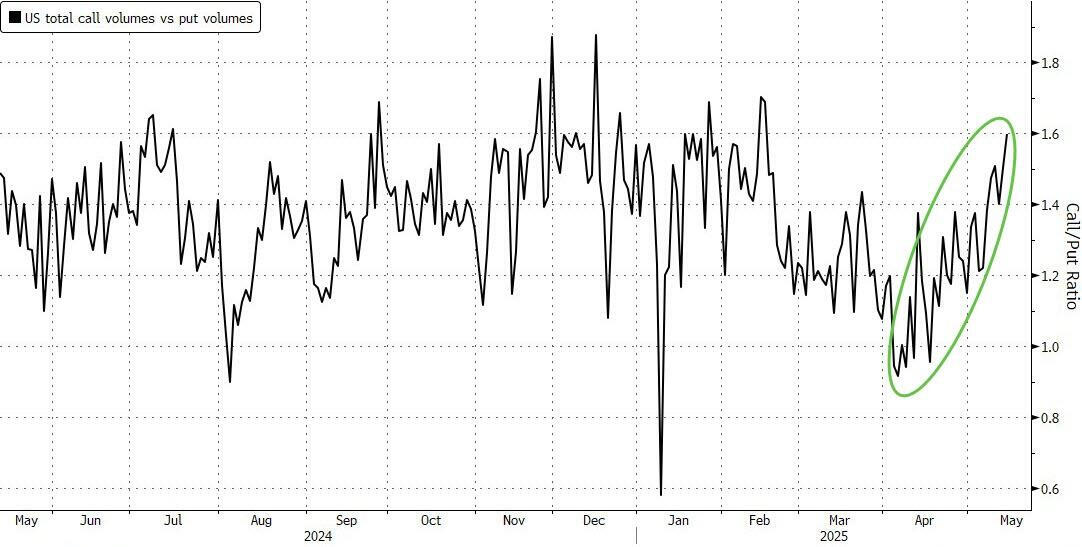

Beneath the surface, the tape is flashing more green than red. Cyclicals and defensives both found buyers, while the S&P 493 quietly outperformed the Mag7, suggesting the rally is broadening—not narrowing. Market breadth is improving, not deteriorating—a subtle but bullish tell. Greed, not fear, is back in charge, with the call/put ratio hovering at euphoric levels last seen before the S&P’s February record. Traders are no longer hedging for stagflation—they're hedging against being left behind.

That said, this isn’t a one-way rocket ship. The late-session tech wobble that clipped the Nasdaq serves as a reminder: this market is hypersensitive to headlines, especially those tied to AI rollout timelines and sector leadership fragility. And while the trade truce chatter has soothed nerves for now, tariffs aren’t going away—they’re baked into the administration’s policy playbook. The question is no longer if tariffs persist, but where the effective rate settles. Will it stabilize above 15%, or drift lower as deal-making and carve-outs unfold?

The real market calculus lies in the pass-through math. How much of the tariff burden do corporates choose to swallow, and how much do they shove down the value chain to consumers? That balancing act will take months to surface—and it’ll show up not in press conferences, but in the gritty details of import prices, CPI, retail sales trends, and margin guidance tucked into earnings calls. That’s where traders will eventually find the truth: in the tug-of-war between pricing power and consumer resilience. Until then, the market will keep trading the smoke signals.

At the end of today, we’re in a “buy everything” regime where economic data trumps headline disruption, and a high-stakes poker game of tariff chicken is being re-priced as not pure negative. The S&P is trading like last month’s rout was just a bad dream. Call it what it is: a stampede driven less by fundamentals than by FOMO, momentum, and the visceral fear of missing the next leg higher. The question now is simple—who’s still sidelined, and how fast are they about to chase?

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.