USD/CAD: Will March 1 matter?

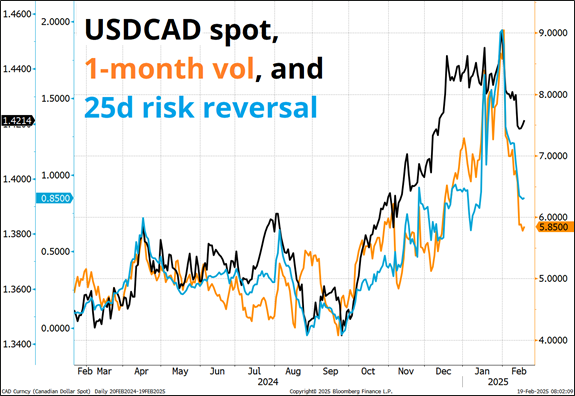

USDCAD is on the cusp of becoming interesting again as vol, skew, and spot have all moved significantly lower and we are now 10 days away from the March 1 deadline for 25% tariffs on Canada and Mexico. While these are viewed as somewhat of a farce by most people in the market, they are still lingering! On February 3, Trump Truthed the following:

“I am very pleased with this initial outcome, and the Tariffs announced on Saturday will be paused for a 30-day period to see whether or not a final Economic deal with Canada can be structured. FAIRNESS FOR ALL!”

Has a final economic deal with Canada been structured? Not yet. Unless you consider the deal that Trump negotiated and signed (USMCA), of course, but that deal is no longer relevant for whatever reason. The interesting question now is whether the market will even bother to rally USDCAD into March 1, or the credibility of the threat is now so low as to be irrelevant to traders. With nothing priced, it’s probably worth considering the possibility of a last-second runup in USDCAD as March 1 nears. Even if nobody believes the threat, it will be the path of least regret to have something on just in case.

You can see in this chart that 1-month CAD vol and skew (orange and blue lines) are both back to pre-election levels. If you think there is a greater than 20% chance that Trump puts the 25% tariff on Canada, plug your nose and buy some 1-month USDCAD calls.

Purgatory

The collapse in FX vol and general market malaise right now is a function of a narrative vacuum. Tariffs are not a tradable theme, the Fed is not in play, Russia/Ukraine is not evolving fast enough to deliver profits to EURCHF longs or EURPLN shorts, and the potentially negative impacts of DOGE and tariff uncertainty are not appearing in the economic data yet because of strong JAN/FEB seasonality. There is not a great argument for higher US yields here, but the good arguments for lower yields rely on weakening economic data that we won’t see for at least a few more weeks.

This leaves us in the nothingburger zone where economic data doesn’t mean much, headlines are falling on deaf or desensitized ears, and strong trends like JGBs and gold are crowded but still working on pure momentum.

I suppose the theme is the disappearance of TINA, but that has played out strongly in equities, with only a marginal impact on FX. The rebirth of foreign equities and carry feels like it could dissolve at any moment as tariffs loom March 1 and/or April 2.

I suppose it’s logical to just stick with what’s working (PLTR, BABA, GLD, short JGBs) etc. but I am just going to sit here doing nothing in FX until something attractive appears. I don’t think there is a short USD trade to be done on the back of RoW exceptionalism because it’s long in the tooth and crowded in many cases (Europe, especially) and the FX response to European exceptionalism has been woefully unimpressive on the currency side.

At the start of 2025, EURUSD was as crowded as it has ever been. Since then, European equities have skyrocketed, US equities have come into question, and EURUSD is up only 85 pips. So, we have unwound a massive short EUR position with very little impact and now the risk/reward looks better long USD than short. But long USD has no real solid thesis behind it, so my base case is we consolidate for a bit and then see what happens March 1.

Final thoughts

BABA and WMT earnings coming up. I am fascinated by WMT stock, which looks like a constant VWAP over the past 12 months. Their new AI model and data center GPU products must be doing very well.

The P/E ratio chart is intriguing.

Author

Brent Donnelly

Spectra Markets

Brent Donnelly is the President of Spectra Markets. He has been trading currencies since 1995 and writing about macro since 2004. Brent is the author of “Alpha Trader” (2021) and “The Art of Currency Trading” (Wiley, 2019).