Weaker job growth could also invite increased rate-cut expectations for March’s policy meeting

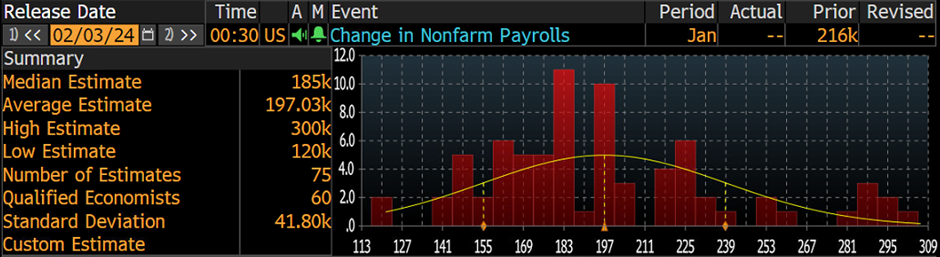

According to Bloomberg, the median estimate for today’s non-farm payrolls for January is 185,000, with the estimate range between 300,000 and 120,000.

A softer-than-expected release—around the 130k-140k neighbourhood that is nearer the estimate range low—may attract USD shorts. Weaker job growth could also invite increased rate-cut expectations for March’s policy meeting. Regarding an upside surprise, markets would likely want to see upwards of 240,000. This could trigger a short-term dollar spike and would likely help seal the deal for a no-change in March, as strong jobs growth could eventually underpin inflationary pressures.

Expectations for the unemployment rate are for a slight uptick to 3.8% from 3.7% the month prior, which would pull the rate nearer the top of the recent two-year range (the highest we’ve been in this time is 4.0%). To surprise markets, a move to 4.0% or greater would need to occur (USD bearish) and a push south of 3.6% (the two-year range low is 3.4%) may trigger USD bulls.

For average earnings, the year-on-year measure is expected to come in at 4.1% for January, matching December’s reading. The estimate range, however, falls between 4.2% and 4.0%, therefore a print below (above) 4.0% (4.2%) would see elevated volatility.

This week’s data

US Job Openings surprised to the upside on Tuesday. According to the Bureau of Labor Statistics, the number of job openings in the US increased to a little more than 9.0 million in December 2023. This moderately surpassed the upper estimate range limit of 9.0 million and came in comfortably north of the median estimate of 8.75 million. However, with the upward revision of the previous number to 8.93 million, this is little changed from November. Wednesday followed up with a meaningful decrease in job growth, as per the monthly ADP employment report, and yesterday saw the ISM Manufacturing PMI employment component drop to 47.1 in January from 47.5 in December.

Fed rate pricing forecasts six rate cuts

You will recall that the Fed were live and kicking earlier this week and essentially acknowledged rate cuts are on the horizon, though pushed back against the number of rate cuts and also against a March cut. Fed Chair Powell himself came out and said this: ‘Based on the meeting today, I don’t think it’s likely that the Committee will reach a level of confidence by the time of the March meeting’.

However, while the Fed continue to project only three cuts this year, the markets now project nearly six cuts by the year-end. Remember, just a week ago, markets were pricing in fewer cuts.

So, what the market is perhaps communicating here is that while the Fed is saying they’re unlikely to cut in March (Fed funds futures data also shows around a 37% chance of a cut at the upcoming meeting), additional cuts will be seen later on in the year.

Market snapshot ahead of the event

The S&P 500 fell sharply on Wednesday, dropping -1.6%, but Thursday, leaving nearby daily support unchallenged at 4,818, saw price reclaim all recently lost ground and end the session testing the previous day’s high. As of writing, we continue to trade near all-time highs.

Although the US Dollar Index navigated southbound on Thursday, it changed little in terms of the multi-week range held between daily support and resistance at 102.92 and 103.62, respectively (note also that the support and resistance is accompanied by a 50-day SMA and a 200-day SMA, respectively). You can also see that the Relative Strength Index (RSI) recently formed a hidden negative divergence (a cross sub-50.00 would help reaffirm negative momentum). Ultimately, then, heading into the event, the daily chart’s range limits will be watched, and a breakout on either side could see follow-through momentum, targeting either the lows of 102.10 (in the event of a downside push) or resistance at 104.15 should a breakout higher emerge.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,