US: New home sales, a short-lived rebound?

The significant rise in American households’ mortgage rates - as illustrated by a 30-year fixed rate of 7.9% according to the Mortgage Bankers Associations (MBA, week of October 29th), a 23-year high, prompted a depletion of housing inventories on the existing real estate market. In 2023, the inventory is estimated at 1.05 million in average by the National Association of Realtors (NAR), against 2.2 million between 2010 and 2019, as households are reluctant to sell their home in order not to have to buy a new one and shift towards a higher debt service regime.

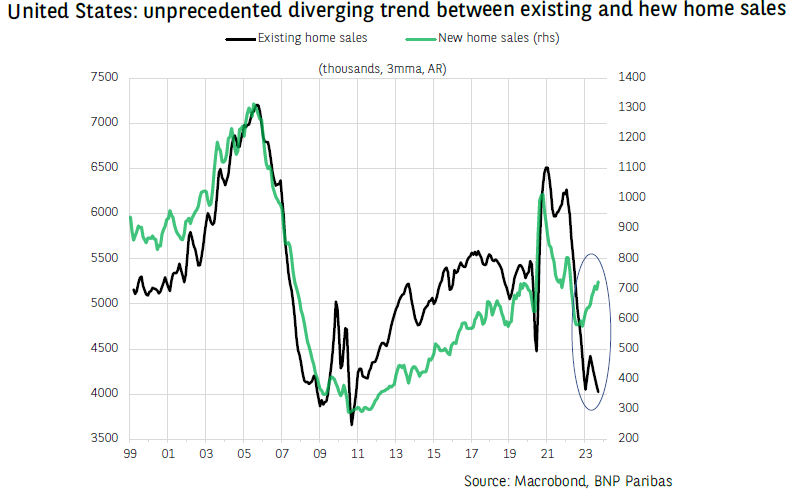

This “freezing” situation on the existing home segment enabled some demand redirection towards newly built houses, inducing previously unseen diverging trajectories between the two indicators since late 2022. In September 2023, new home sales (3-month moving average) increased by +24% y/y, whereas existing home sales are down by nearly 16%. So far, in average, in 2023, 1 newly built home had been sold for 6.2 existing homes, against a 1/10.9 average between 2010 and 2019.

The strength of newly built share of the market translated into the quarterly national accounts’ residential investment data, with a +1% q/q increase in Q3 2023, putting an end to a 9-quarter streak of contraction. However, this rebound is unlikely to prove sustainable, as the impact of higher rates on real estate demand is tangible. Indeed, the MBA index of mortgage applications has reached a 27-year low in September, which is explained by a nearly uninterrupted deterioration of affordability appearing in the related NAR index since the first Fed rate hike in March 2022. Supply-side indicators are also pointing to weakness, as homebuilder sentiment is sluggish (NAHB index standing at 64.5 in September), while housing starts and building permits remain on a downward trend.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.